Chesapeake Energy Corporation (ticker: CHK) is the second-largest producer of natural gas and the 10th largest producer of oil and natural gas liquids in the U.S. The company is actively selling down sections of its business to centralize focus on the Eagle Ford and Utica plays. Approximately $4 billion in divestments were made in 2013 and CHK anticipates selling another $4 billion in 2014. The company is executing a spinoff of its oilfield services unit, as announced in February 2014, and expects the deal to be complete by June 30, 2014.

Divesture Overview

Chesapeake reviewed ongoing operations in an analyst day on May 16, 2014. The company has sold approximately $925 million in asset sales to date in 2014. Deals are in place to sell non-core assets in Texas and Oklahoma for approximately $310 million in cash proceeds. Additional divestures in southwest Pennsylvania and Wyoming are expected to return $290 million in cash to CHK. Despite the sales, CHK says it will lose only 2% of production and $250 million of operating cash flow.

At the analyst day, Doug Lawler, Chairman and Chief Executive Officer of Chesapeake Energy, said: “You see a lot of companies out there that are increasing CapEx and increasing production. You see some that are increasing CapEx and decreasing production. Chesapeake is increasing production and maintaining flat CapEx. As we look at the current outlook today, the work has taken place in the Company to continue to improve our balance sheet.”

The company is also selling CHK Cleveland Tonkawa, its subsidiary, to eliminate roughly $1 billion in equities paid to third parties. Upon its completion, CHK will receive a dividend of $400 million which will be used to pay down additional debt. The new company will be named Seventy Seven Energy and is expected to be completed by June 30, 2014.

Management said all sales and spinoffs will reduce CHK’s net leverage by nearly $3 billion. Additional benefits include $200 less in capital expenditures and $70 less in interest expenses. Total sales and divestures for 2014, once existing deals are closed, will surpass $4 billion.

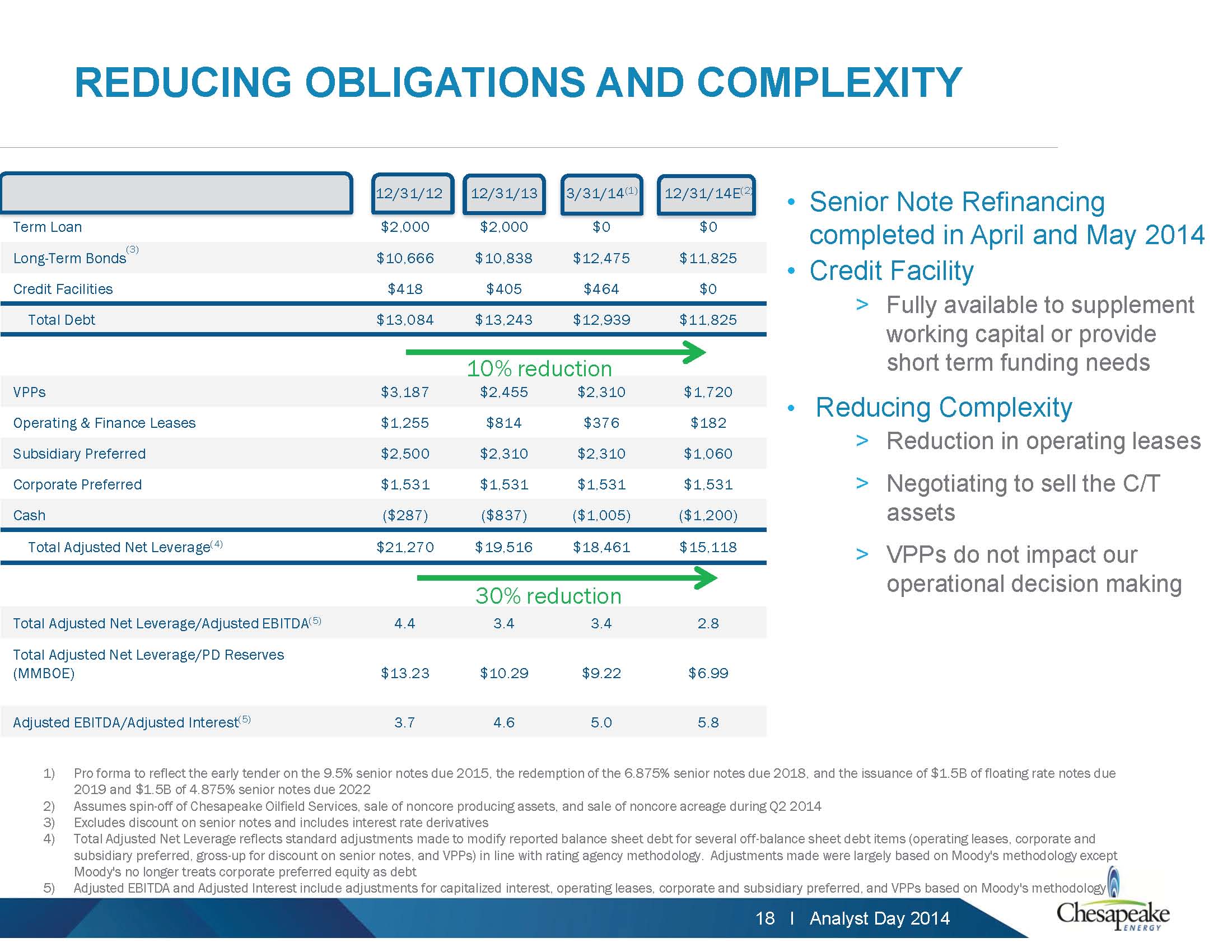

Chipping Away at Debt

Reducing debt and leverage has been a staple of CHK’s business operations since 2012 and divestures have accelerated since management changed in January 2013. By December 2014, as forecasted by CHK management, debt will drop to $11.8 billion, which is 10% lower than December of 2012. Adjusted net leverage is expected to drop by 30% over the same time frame, or $6.2 billion less.

CHK is enforcing the debt reduction trend by hedging the majority of its 2014 production. Approximately 64% of its natural gas is hedged along with 70% of oil production. The company has also moved to a pad drilling system that will account for 90% of all drilling operations by year-end 2014. A total of $470 million is expected to be saved under the new format coupled with faster drilling times and longer laterals, and a total of $1 billion in annual costs are projected to be saved if the supply chain is considered.

Remaining Properties Expected to Grow

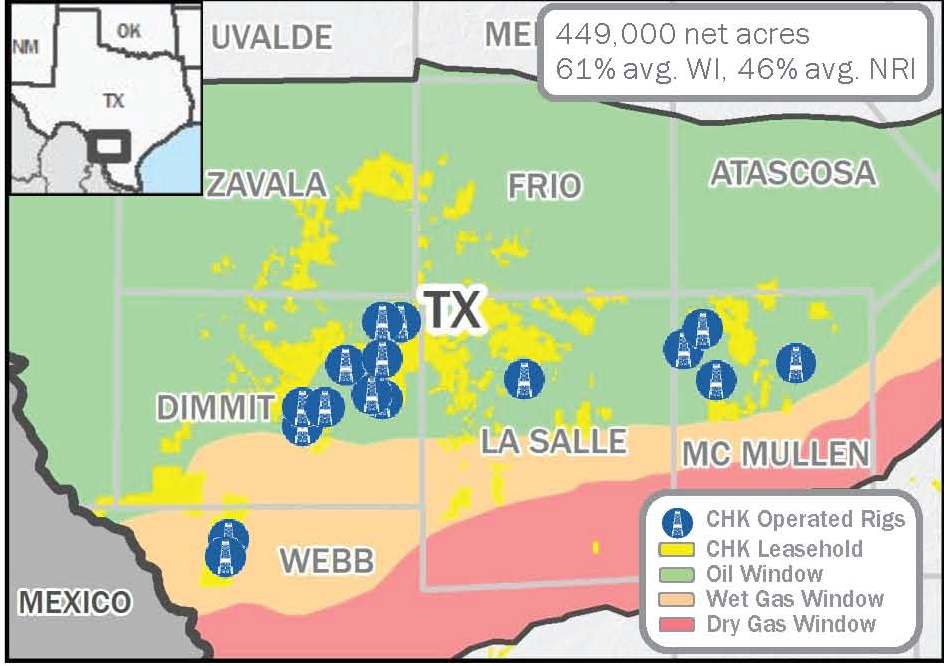

The Eagle Ford remains the focus of CHK’s new properties and will receive 35% of expenditures in 2014. The company plans on running 15 to 20 rigs in the play and 2015 production, adjusted for divested 2014 production, will grow 7% to 10% on a year-over-year basis. The growth is not projected to be a one-time occurrence – CHK expects five year annual production growth of 7% to 9%.

2014 production will start the trend by increasing 9% to 12% compared to 2013. Forecasted production is 675 MBOEPD to 695 MBOEPD, and revenue from liquids is expected to increase by 29% to 33%. The Eagle Ford has rapidly become one of the top hydrocarbon plays in the United States. Sanchez Energy (ticker: SN) operates almost exclusively in the region, and other majors like EnCana Corporation (ticker: ECA) and Devon Energy (ticker: DVN) have spent $3 billion and $6 billion, respectively, to jump into the region.

Nick Dell’Osso, Chief Financial Officer of Chesapeake, declined to rank the projects, but did single out other plays. “We love our position in the Eagle Ford,” he said. “The Utica is very strong for us. The Marcellus is very strong, Haynesville emerging with the strength that we are seeing there, it continues to look very good so it’s a little bit difficult to say, because they are all contributing. And the beauty of this Company is we are not a one trick pony. We’ve got a portfolio of assets that can be optimized to drive greater value.”

While gains have been made, Dell’Osso said work is still left to be done. “The strategy is not to become investment-grade. Becoming investment-grade is an outcome of the strategy. The strategy is to create value. The strategy is to grow this company and in doing that, the things that you are seeing in this presentation and the things that you will see all day today equate to a company that has a much stronger balance sheet and has investment-grade credit metrics, which gives us the confidence that this will happen and it will be an outcome.”

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.