Leading oil and gas accounting firm Hein believes industry players should be ready for oil to stay below $60 – $70 per barrel; examines 3 trends affecting oil price

From the Hein Energy Team

Since peaking at $60 per barrel in June 2015, the price of West Texas Intermediate (WTI) crude oil took a sharp nosedive to under half that price before rallying to the low-$50 range by the end of 2016 and has languished between $45 and $55 since. While people are optimistic to see $60 to $70 oil prices sooner than later, there are signs that this might not be the case.

There are a number of reasons to believe that this cycle may not be a temporary event, and that producers will need to position their operations to survive an extended period of crude oil pricing below $70 per barrel.

Here are three key trends fueling this malaise:

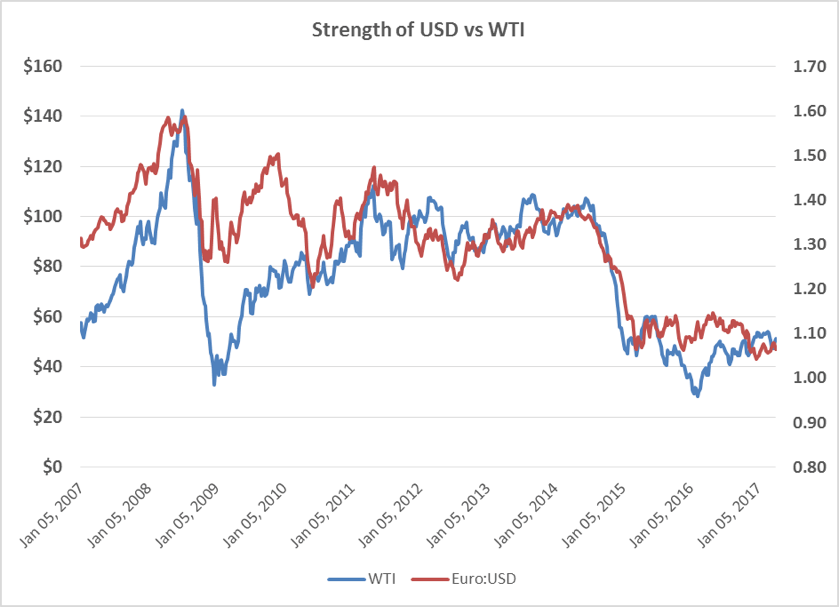

The U.S. Dollar vs. the Euro

Oil is a global commodity that is transacted in U.S. Dollars (USD). For that reason, the recent strength of the dollar against most other developed market currencies – particularly the Euro – has dampened oil price growth. Consider the following chart:

(Source: James Harden, Hein)

Interestingly, when crude oil hit its pre-recession all-time high in July 2008, the USD hit its all-time low against the Euro. More recently, the U.S. economy has continued to gain strength at a rate greater than most other advanced markets, resulting in a stronger dollar that has driven the exchange rate on the Euro down to under $1.10. The coefficient of correlation (r2) between the USD and WTI was greater than 0.73 r2 over the past 10 years and over 0.94 r2 since January 2013.

While a strong dollar policy was initially favored by the fledgling administration of President Donald Trump, in recent weeks the tide has seemingly turned, with Treasury Secretary Steve Mnuchin saying an “excessively strong dollar” might hinder short-term economic growth. However, continued U.S. job market strength, rising government debt levels and upward pressure on interest rates – combined with continued Eurozone debt issues – will make it difficult for policymakers to weaken the dollar’s near-term trajectory.

What’s the bottom-line? As long as the dollar remains strong, it makes U.S. exports more expensive on world markets. If the current dollar-to-euro exchange rate remains near parity, WTI oil prices will linger in the current range, absent an unforeseen supply issue or major geopolitical event. That said, a recent forecast from a major European bank projected the Euro could fall as low as 95 cents on the USD later in 2017, a scenario that would take crude prices much lower, perhaps even below $40 per barrel once again.

Global demand: Long, slow rise

While China remains the world’s largest energy consumer, overall demand from that nation continues to be sluggish. According to a recent Reuters analysis, China’s total demand for oil rose just 2.5 percent in 2016, the third consecutive year in which consumption growth has declined. That’s largely attributable to a slowing Chinese economy, which fell from 7 percent growth in 2015 to 6.7 percent through the end of last year.

China’s decline in energy use is part of a broader global picture. In its most recent monthly report, the International Energy Agency (IEA) noted that global oil product demand rose by 1.6 million barrels per day for 2016 to an overall total of 95.6 million daily barrels of consumption. This year, however, IEA expects the level of growth to drop back to 1.4 million barrels per day, pointing to softer demand in key markets such as Germany, India, Korea and Japan.

(Source: Short-Term Outlook, U.S. Energy Information Agency)

For U.S. producers, a glimmer of hope is on the near-term horizon, as the U.S. Energy Information Agency (EIA) forecasts that growth in global oil demand will inch back to 1.6 million barrels per day by 2018 (chart above). Further, IEA’s 2016 medium term oil market report projected that global oil consumption will rise from an estimated 96.9 million barrels per day this year to 100.5 million barrels per day by 2020, with a slight tightening of global crude oil inventories during that time.

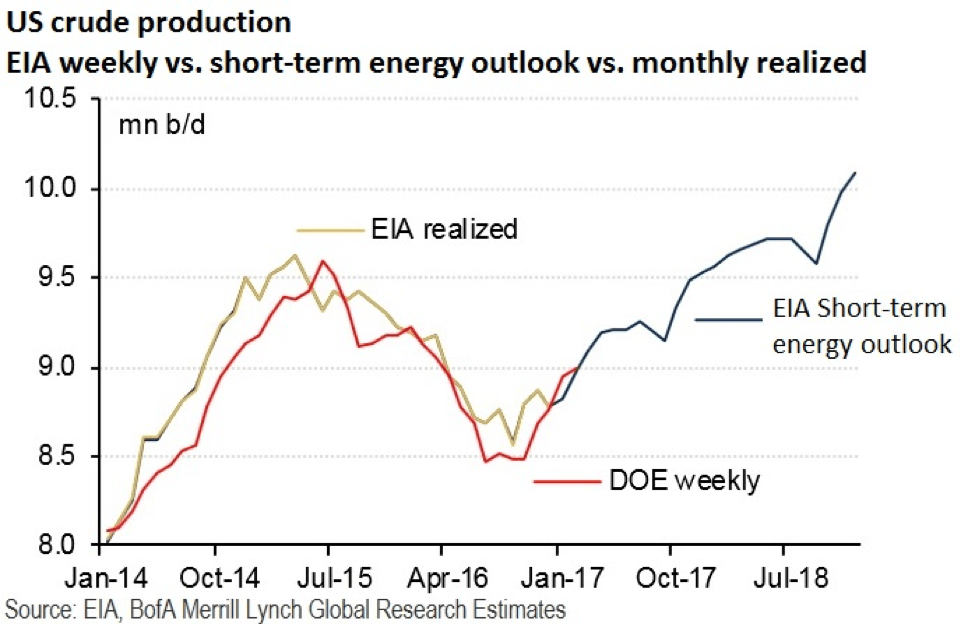

Global production: In search of a balance point

A generation ago, news reports were full of headlines about “energy shortages” and “peak oil,” with doomsday scenarios pointing to how global economies would need new kinds of energy to power themselves in a post-petroleum world. While today’s energy sources are indeed more diverse, so are the ways in which petroleum producers have been able to tap oil and gas reserves previously thought to be inaccessible.

The result? The world is awash in oil and gas supplies, which makes inventory management a critical factor in market pricing.

(Source: U.S. Energy Information Agency, NYMEX and Market Realist)

To help address the supply issue, U.S. oil producers last year hauled back production from 9.2 million barrels per day in January to 8.6 million barrels per day by September (gold line, chart above). While fourth quarter oil production bounced slightly upward, the overall 2016 production average of 8.9 million barrels per day was well below the daily average of 9.4 million barrels recorded the previous year. On the global stage, producers in the Organization of the Petroleum Exporting Countries (OPEC) agreed at the end of 2016 to a historic cut of 1.8 million barrels per day in an attempt to restrict supply and boost crude oil pricing. While some industry analysts question if all OPEC nations will abide by the production cuts, scheduled to last through June 2017, the cartel said it would consider an extension through year-end 2017 if oil supplies and demand had not reached more favorable balance.

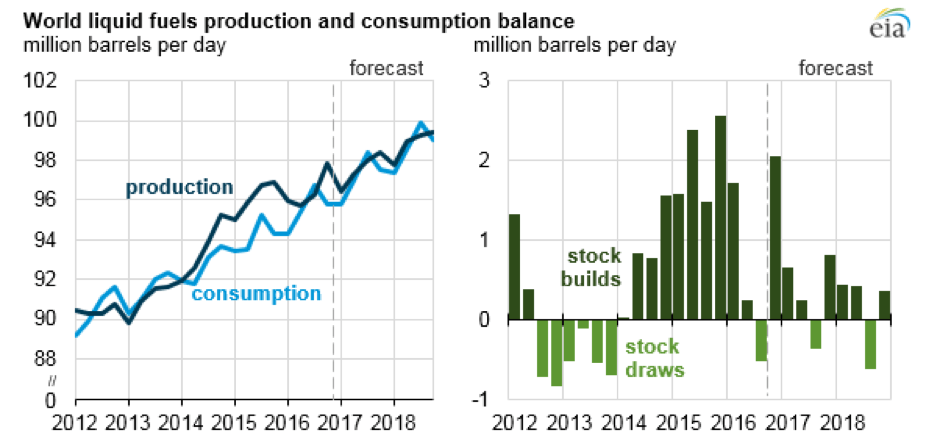

(Source: U.S. Energy Information Agency)

Through 2016, global oil inventories increased an average of 0.9 million barrels per day, including a sharp production uptick in the fourth quarter by both U.S. and OPEC energy firms. However, a short-term outlook by EIA forecasts that overall oil production will rise more slowly in 2017 and 2018, causing existing inventories to gradually decline (chart above). By the second half of 2018, EIA projects that worldwide crude oil inventories will decline by about 0.1 million barrels per day.

In summary, a case for rising crude oil prices in the next several years is dependent on three main factors: A slow (if steady) rise in global demand, U.S. and OPEC restraints on production, and a weakening U.S. Dollar. If the demand and production forecasts hold up, recent OPEC quotas are adhered to, and the euro rallies to the $1.20 range against the dollar, it’s very possible WTI crude pricing could rebound to the $75 per barrel range by 2019 to 2020.

Hein is an Accounting Today Top 100 Firm.