Decades ago, the Organization of the Petroleum Exporting Countries (OPEC) was THE lifeline to the United States’ thirst for oil. Now, record production, horizontal drilling, advanced seismic and completion technologies, and increased spending rates have the U.S. primed to become the world’s top oil producer.

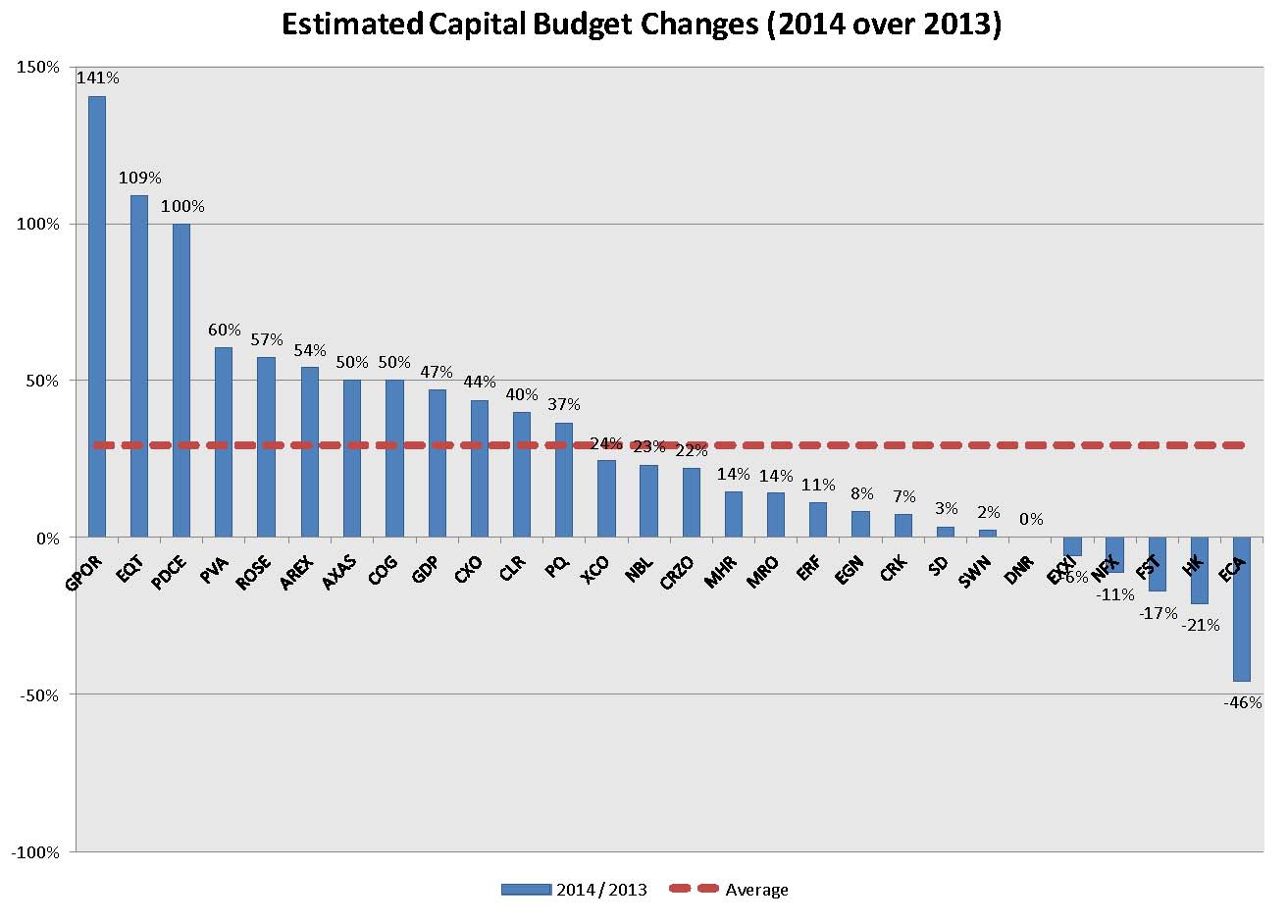

Out of 62 companies for which we have gathered data on capital expenditures and estimates, 28 have announced capital budgets for 2014. These companies are expected to spend a combined $39.5 billion in 2014, or 15% more than they are estimated to invest in 2013 (source: Barclay’s).

Of those 28 companies, 23 of them are expected to increase capital spending in 2014 from estimated 2013 levels and five are anticipated to reduce spending. Companies with expanding budgets are those with high asset quality, operating primarily in resource plays and/or otherwise weighted to crude oil. They include operators in the Marcellus (e.g., EQT, PDCE, COG), the Permian Basin (e.g., AREX, CXO), the Eagle Ford shale (e.g., PVA, ROSE, GDP) and the Bakken oil shale (e.g., CLR, OAS).

Companies that that have staked-out new positions in emerging plays are also among the leaders. Operators fitting that description include PetroQuest (ticker: PQ) in the liquids-rich Woodford shale, Penn Virginia Corporation (ticker: PVA) in the Eagle Ford shale and Goodrich Petroleum Corporation (ticker: GDP) in the Tuscaloosa Marine Shale play.

The chart below plots the estimated growth in 2014 capital budgets from anticipated 2013 levels. The resource boom has prompted some to question the Energy Policy and Conservation Act, a law passed in 1975 that banned the exportation of crude oil. The law was put into effect after OPEC members imposed an embargo on U.S. oil in the 1970s, damaging the country’s economy. The dramatic shift in energy dependence has reshaped the playing field, and several critics are calling on the Obama administration to consider lifting the ban in order to maintain jobs, prices and production.

Lisa Murkowski, the top Republican on the Energy and Natural Resources Committee, has made headlines for publicly encouraging President Obama to review the issue. Her aides say she plans on submitting a white paper on the matter if the President does not act in the near future. Edward Moniz, the nation’s Energy Secretary, has called the ban “dated.” At the Platts Energy Outlook Forum on December 12, 2013, Moniz said, “There are lots of issues in the energy space that deserve some new analysis and examination in the context of what is now an energy world that is no longer like the 1970s.”

Lisa Murkowski, the top Republican on the Energy and Natural Resources Committee, has made headlines for publicly encouraging President Obama to review the issue. Her aides say she plans on submitting a white paper on the matter if the President does not act in the near future. Edward Moniz, the nation’s Energy Secretary, has called the ban “dated.” At the Platts Energy Outlook Forum on December 12, 2013, Moniz said, “There are lots of issues in the energy space that deserve some new analysis and examination in the context of what is now an energy world that is no longer like the 1970s.”

The Energy and Natural Resources Committee is hosting a full hearing on lifting the crude export ban on January 30, 2014 at 10:00 am ET. A live webcast of the event will be featured on its site.

Current Export Situation

The United States presently exports roughly 100 MBOPD of light crude to Canada, and all companies participating in the process have been granted licenses by the Department of Commerce. Some analysts predict the number will soon double to 200 MBOPD. At this time of writing, Canada receives nearly 100% of crude exports. U.S.-based producers have been shipping light crude to Northeast markets since most refineries on the Gulf Coast are better suited for heavy crude. Included in the Northeast are Canadian refineries well-equipped to handle the resource, explaining why our neighbors to the north are on the receiving end of crude being sent abroad.

The United States presently exports roughly 100 MBOPD of light crude to Canada, and all companies participating in the process have been granted licenses by the Department of Commerce. Some analysts predict the number will soon double to 200 MBOPD. At this time of writing, Canada receives nearly 100% of crude exports. U.S.-based producers have been shipping light crude to Northeast markets since most refineries on the Gulf Coast are better suited for heavy crude. Included in the Northeast are Canadian refineries well-equipped to handle the resource, explaining why our neighbors to the north are on the receiving end of crude being sent abroad.

However, there is a slim opening for crude exports. The process is allowed if, and only if, it is in the best interest of the United States, and that decision lies solely at the discretion of the government.

Redefining Types of Crude May be a Starting Point

Blake Clayton, an Adjunct Fellow for Energy at the Council on Foreign Relations, wrote a Memorandum on redefining trade restrictions in an article on July 2013. One suggestion is to allow the export of light oil, which is also known as lease condensate, due to inadequate infrastructure. He writes, “With few viable domestic buyers, producers are forced to choose between leaving oil in the ground and pumping it at depressed prices. These artificially low prices slow additional U.S. crude oil production. New refineries and pipelines currently under construction will help remedy some of these market distortions over time, but a simpler, more cost-effective solution would include allowing U.S. crude to be exported.”

He notes that doing so would lead to the export of more than 500 MBOPD by as soon as 2017. Wells Fargo Securities estimates lease condensate at just 1 MMBOPD (roughly 9%) of U.S. liquids production and effects on gas and diesel prices would be minimal since the hydrocarbon is not a feedstock for refined products. Clayton agrees with the assessment in his article.

Change, while not Imminent, is Approaching

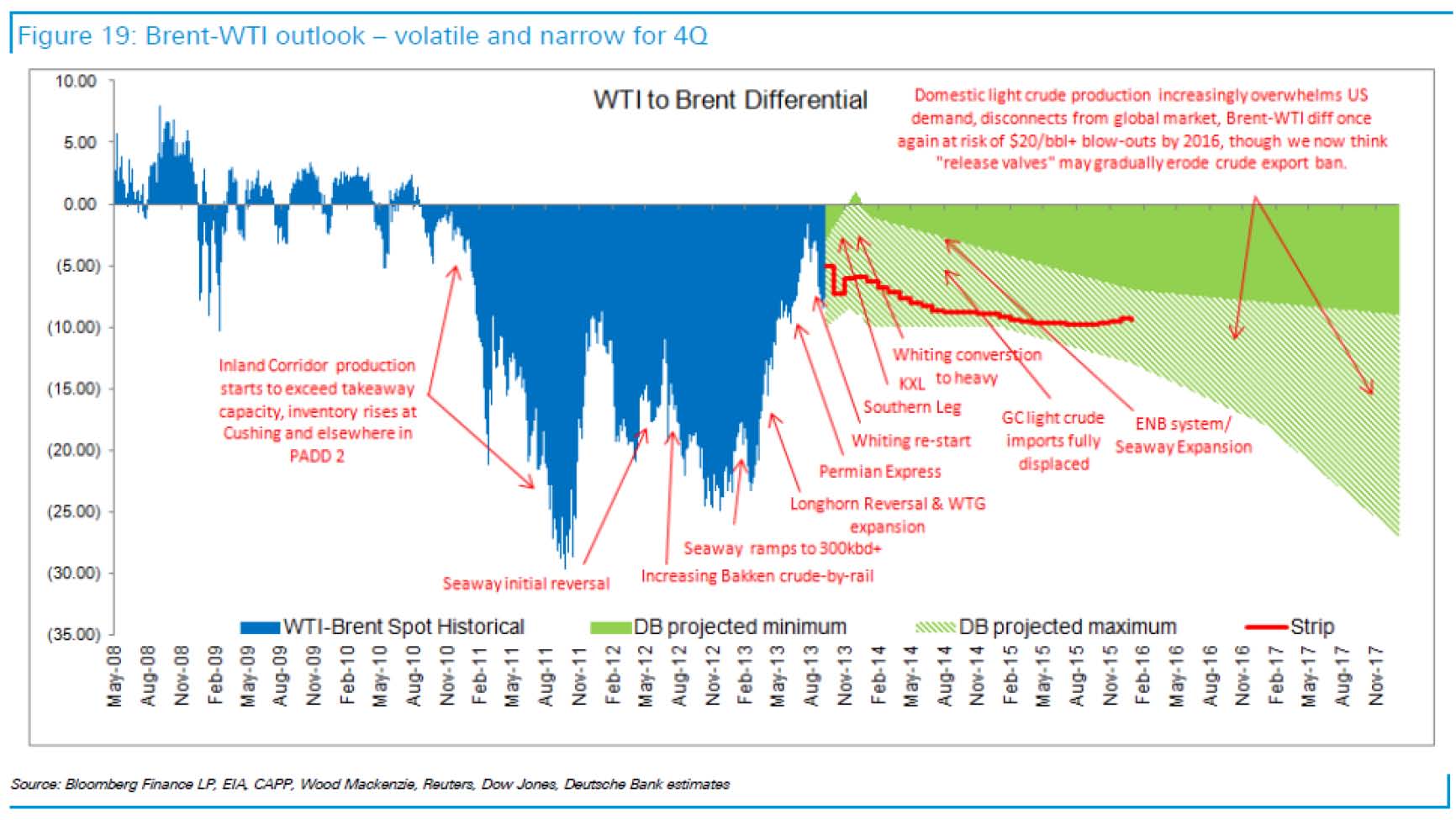

Analysts for Wells Fargo Securities said they are, at present, favorably disposed towards the refiners and do not believe a major change is likely to occur any time soon. However, the research team does believe the situation will be addressed by mid-2014 or 2015 if differentials in U.S. crude prices persist (shown to the right). In response, Wells Fargo anticipates producers becoming more aggressive in formulating exports to Western Europe and Mexico, in particular. Altering the standards for exportable crude types or more clearly defining “national interest” are other possibilities.

Analysts for Wells Fargo Securities said they are, at present, favorably disposed towards the refiners and do not believe a major change is likely to occur any time soon. However, the research team does believe the situation will be addressed by mid-2014 or 2015 if differentials in U.S. crude prices persist (shown to the right). In response, Wells Fargo anticipates producers becoming more aggressive in formulating exports to Western Europe and Mexico, in particular. Altering the standards for exportable crude types or more clearly defining “national interest” are other possibilities.

What’s In Store?

Condensate production is likely to increase in the coming years as the Eagle Ford shale and its light oil is primed for mass production. Global Data says companies will spend roughly $30 billion on exploiting the play in 2014. More than 250 rigs are running in the region, and major operators are expecting to drill for at least five years at the current pace. The Texas Railroad Commission reports that more than 11,000 drilling permits have been issued since January 2011, resulting in a 408% increase in oil production.

With in-house U.S. production rising, imports are declining. In fact, the U.S. trade deficit reached a four-year low in November 2013 due to lower imports. A popular opinion derived from increased shale production is that emissions will also increase. However, the oil and gas boom has steered the United States away from reliance on coal, which emits roughly twice as much carbon as shale. The EIA expects clean natural gas to steadily replace coal use, resulting in emissions staying below 2005 levels for the next three decades.

In spite of recent developments, Wells Fargo analysts believe lifting the ban is unlikely due to the Obama administration’s emphasis on climate change and emissions. However, the company believes the United States ‘desire to support positive economic development, improve trade relations and gain influence in global energy markets may lead to support for adjustments to the current export restrictions.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.