CEO Hager: STACK is “the best emerging development play in North America”

Devon’s STACK position has grown by more than 150,000 net acres in recent months

Devon Energy (ticker: DVN) has secured the strongest foothold in the Cana-Woodford, pro forma for its $1.9 billion acquisition of Felix Energy LLC on December 7, 2015. Rumors of the impending cash-and-stock exchange were first brought to light by Reuters on December 3, but today’s announcement carried additional acquisitions that were unforeseen in the preliminary report.

In addition to Felix Energy, Devon purchased $600 million of acreage in the Powder River Basin from an undisclosed private seller. A third deal, in conjunction with EnLink Midstream Partners (ticker: ENLK), involved the purchase of privately held Tall Oak Midstream for $1.55 billion. Tall Oak’s assets consist of gathering and processing assets located in the Cana-Woodford region, or the STACK (Sooner Trend Anadarko Basin Canadian and Kingfisher Counties), as Devon calls it. Both Felix Energy and Tall Oak Midstream were financed by EnCap Investments, a private equity company with approximately $27.5 billion of limited partner capital interests in the oil and gas sphere.

Collectively, the three acquisitions announced by Devon and EnLink amount to $4.05 billion. Total costs to Devon were $2.50 billion and will be funded with approximately $1.35 billion of equity and $1.15 billion of cash on hand.

Click here for a presentation addressing the announcement.

The Devon/EnLink Overlap with EnCap

EnLink was formed in March 2014 with the merger of Devon and Crosstex Energy, and Devon remains the majority owner of the midstream provider today. DVN is EnLink’s largest customer and accounts for more than half of its business, and DVN management says its ownership interest is currently valued in excess of $3 billion. Similarly, the EnCap-backed companies of Felix Energy and Tall Oak midstream developed an upstream/midstream buildout in what Devon President Dave Hager called the “best emerging development play in North America.”

Devon and EnLink’s collaboration in the STACK region was perhaps the chief reason behind the acquisitions, a process that DVN management said was privately negotiated. “We would not have been able to secure the Felix assets without EnLink,” said Hager in a conference call following the release. “We leveraged the midstream relationship to secure the Felix transaction and the EnLink relationship gave us a strategic advantage in [the Tall Oak] transaction.”

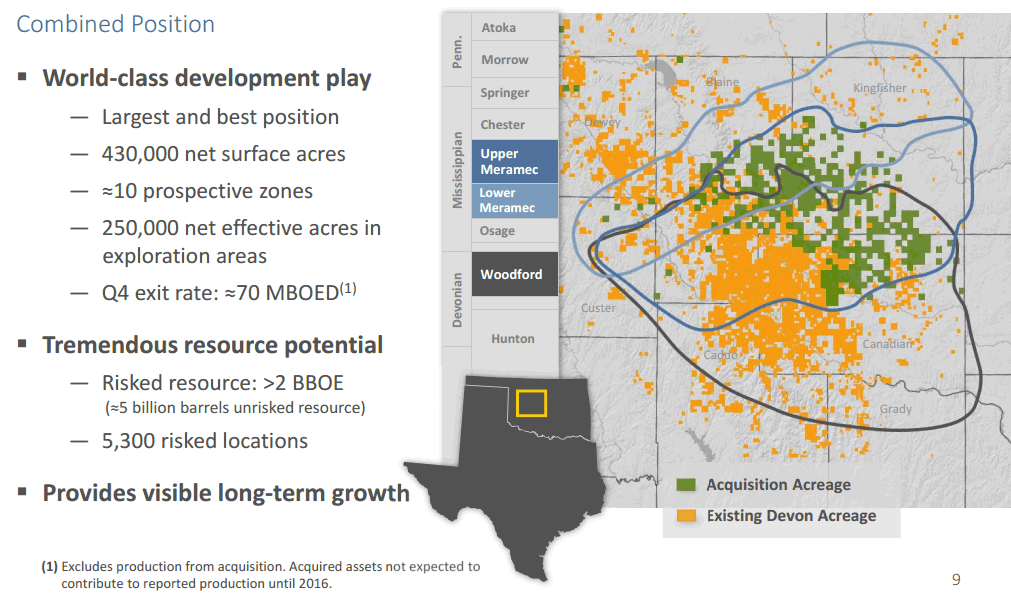

STACK Overview

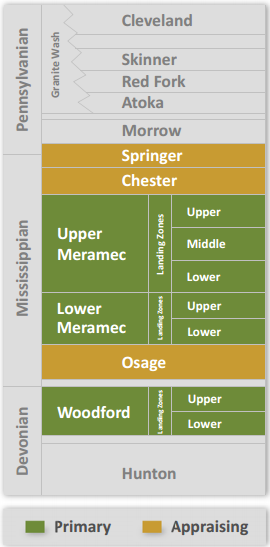

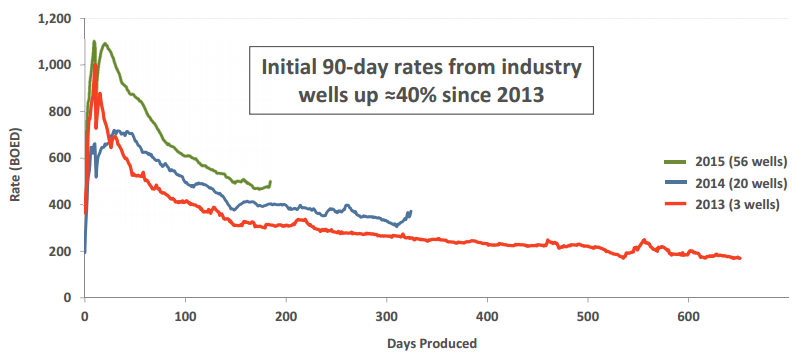

On the upstream side, Devon acquired 80,000 net acres in the STACK for $1.9 billion, with volumes of 9,000 BOEPD and estimated risked resource of approximately 400 MMBOE. Felix established type curves of 1,360 MBOE for the Meramac formation and was generating returns of greater than 40% at current strip prices. “This zone is predictable, repeatable and very large,” said Skye Callantine, President and Chief Executive Officer of Felix, while presenting at EnerCom’s The Oil & Gas Conference® 20.

DVN management estimates only 10% of the acreage has been developed to date, and its drilling inventory consists of 1,400 and more than 3,000 risked and unrisked locations, respectively. Overall, DVN is now exposed to 430,000 net surface acres and 5,300 risked locations in the STACK. In its most recent presentation leading up to the acquisition, Devon listed its position at 280,000 net risked acres. Management acknowledged “accumulating” an additional 70,000 net acres leading up to its Felix Energy acquisition, ultimately increasing its STACK position by more than 50%.

“I can see the acquired position approaching 100 MBOEPD, easily surpassing a materiality of our current position,” said Tony Vaughn, Executive Vice President of Exploration & Production. “Numerous pilots are underway [in our nearby acreage], we’re currently testing at the eight wells per section in the Meramec and 11 wells per section in the Woodford, all in the same lateral interval. The Upper Meramec is big enough to stagger wells, which could essentially double the number of locations that we have estimated.”

DVN management was careful with the details, but did mention three of the pilot wells produced more than 2,000 BOEPD.

Powder River Basin Overview

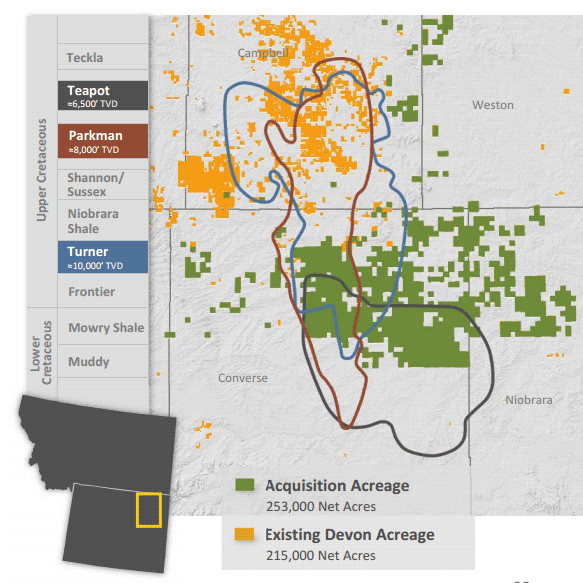

The Powder River Basin acquisition is also significant and possibly lost some of its news appeal due to the size of the STACK announcement, but the $600 million purchase (50% equity) adds 253,000 net acres to DVN’s portfolio. The area is producing 7,000 BOEPD and includes a 60% working interest, more than doubling the company’s previous position. Listed valuations were $1,100/undeveloped acre.

Vaughn said DVN’s legacy activity and “considerable amount of technical work in the area” will be leveraged in its future development. The company’s production from the Rockies increased by 61% on a year-over-year basis, according to its Q3’15 release. In the call, Hager said DVN will likely continue a running rig count of “one or two rigs in the Powder that can easily grow to seven on the new acquired position and probably four or five on our legacy and a different business environment.”

Next Step: Asset Sales

Synonymous with previous landmark acquisitions by Devon, the company will divest a similar amount of asset valuations to essentially offset its latest purchase. This most previously occurred with the $6 billion acquisition of its Eagle Ford position, which was followed by nearly $5 billion in divestures leading up to today’s announcement.

Devon plans on selling between $2 and $3 billion of assets in accordance with today’s announcement. Management has listed its Carthage, Mississippi Lime, Granite Wash and select Midstream Basin positions as possible targets. The listed properties are currently producing 50 to 80 MBOEPD. A minor sale for some of its San Juan Basin position has already been executed for $70 million. Existing midstream positions may also be for sale, including a potential drop-down to EnLink Midstream. Access Pipeline, located in Alberta, is essentially a sure-fire divesture that may be sold as early as the first half of 2016.

Prior to the announcement, Devon had an undrawn revolver of $4 billion, providing some comfortability in the near term.

Market Reaction

Analyst firms acknowledged the attractiveness of the STACK acquisition. The price, however, was a different story.

“We think stock likely comes under pressure,” said a note from Wells Fargo Securities, addressing the announcement. “In sum, levering up in this environment will likely not be well received, Felix price tag looks rich, and some conversations last week (regarding this potential transaction) had investors questioning what we don’t know about their Permian position.”

Capital One Securities had a similar take, saying, “We think the acquisitions announced today are attractive assets and are a good strategic fit, but it appears that DVN is somewhat paying up and the deals are slightly dilutive.” DVN management said about 30 million shares will be issued in accordance with the acquisitions, diluting its share count by about 8%.

Overall, the metrics for the STACK acquisition on a per-acre basis range from $19,800 to $23,000 per acre net of production, based on analyst estimates. On a simpler, black and white breakdown, DVN paid $23,750/acre and about $210,000/flowing BOE. That compares to $9,960/acre and about $86,000/flowing BOE in regards to a May 2014 transaction conducted in the same region.

Newfield Exploration (ticker: NFX), a prominent operator in the region, benefitted from the valuation: its stock dropped only (2%) today when the S&P Energy 1500 Index declined by nearly twice that amount as oil prices slid to a seven year low. Devon closed about (10%) lower.

Moving forward, Devon anticipates the STACK will receive 20% to 25% of its 2016 budget, which is forecasted at $2.5 billion, and the plan is expected to provide oil growth of 10% in 2016.

Seaport Global Securities was a bit more bullish on Devon’s Three Pronged Strategy than some of its peers, saying: “DVN had one of the lowest corporate Q3 recycle ratios in the large cap space based on our recent study, so we think adding the very economically promising Stack to its top-tier Delaware and Eagle Ford assets and doing it in conjunction with a commitment to shed $2B-$3B in non-core assets makes strategic sense.”