Sources Say Deal for Felix Energy LLC would be for about $2 Billion, Including Debt

Devon Energy (ticker: DVN) is in pursuit of privately held Felix Energy LLC, according to a report from Reuters on December 3, 2015. Devon supposedly made a cash-and-stock offer to EnCap Investments LP, the financier of Denver-based Felix. EnCap is a mainstay on the oil and gas private equity market, and has approximately $27.5 billion of limited partner capital investments. The firm has investments in nearly 50 other upstream companies, including E&Ps like Eclipse Resources (ticker: ECR), EV Energy Partners (ticker: EVEP) and Halcon Resources (ticker: HK).

Felix Energy Primer

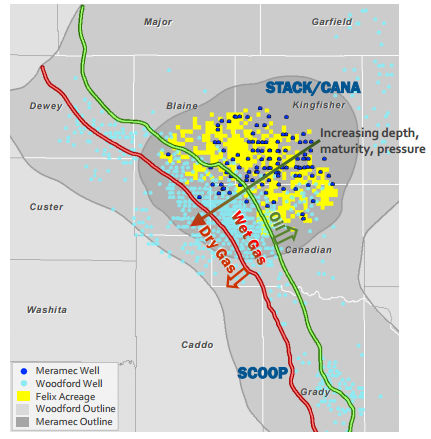

Felix Energy was featured on the private company panel at EnerCom’s The Oil & Gas Conference® 20 in August 2015. Skye Callentine, President and Chief Executive Officer, detailed the company’s position in Oklahoma, which has increased to more than 75,000 net acres in the Cana Woodford and STACK (short for Sooner Trend Anadarko Basin Canadian and Kingfisher Counties) plays.

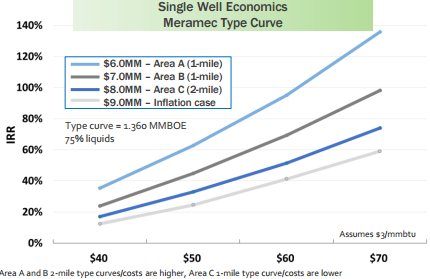

At the time of the Conference, Felix was running three rigs and producing approximately 8,000 BOEPD (80% liquids), with virtually all of its acreage in the liquids portion of the play. The company managed to cut well costs by 40% compared to the time of its initial investment in 2013, and production had increased 40% in the last 12 months based on increased knowledge and efficiencies. The economics for its Meramac wells (located on a bench above the Woodford) generated a type curve of 1,360 MBOE, resulting in internal rates of return greater than 40% at current strip prices on its 2015 program. The formation is also not water-bearing, allowing Felix to avoid additional operating costs regarding water disposal. Callantine described the Meramac as “predictable, repeatable and very large.”

The full webcast of the private company panel can be accessed here.

Devon’s Acquisition/Divesture History

If a deal is reached, it would mark Devon’s first acquisition since the commodity downturn. Its last big acquisition splash occurred in November 2013 when it a transformative, $6 billion acquisition of GeoSouthern’s Eagle Ford assets using a combination of cash and borrowings. Similarly, GeoSouthern was another private company with equity investments from Blackstone Energy – a firm who ultimately exited the Eagle Ford in association with the sale. The development emerges as somewhat of a trend – the company’s other landmark asset acquisition was in 2006 with the purchase of yet another privately held corporation with assets primarily in the Barnett Shale.

Regarding the rumored Felix acquisition, EnCap Investments would be in line to exit the STACK plays if a deal were to be reached. Reuters speculates that a sale would satisfy EnCap’s desire to return money to its shareholders in what has been a difficult year for anybody and everybody associated with the oil and gas industry.

When asked about potential acquisitions in the company’s Q3’15 conference call, David Hager, President and Chief Executive Officer of Devon, said purchases are constantly being evaluated but they must be able to compete with DVN’s existing acreage. “It would have to be very high quality before we would consider adding anything,” he said.

Management also downplayed the notion of any near-term asset sales. The company deserves credit from a timing standpoint, considering it completed approximately $5 billion in asset sales in the window following its Eagle Ford acquisition but prior to the oil price crash in 2014. DVN announced a $2.3 billion divesture of “non-core” United States assets in June 2014, just two months after completing a $2.7 billion divesture of conventional Canadian assets. Other transactions include $3.6 billion in investments from two Asian companies in 2012, in exchange for varying interests. The company also completed its exit from Azerbaijan, Brazil and the Gulf of Mexico in 2010 as part of a $7 billion sale to BP plc.

So Why is Devon Interested?

With the exception of the $6 billion Eagle Ford acquisition, Devon’s lone other purchase in the last nine years occurred in the Cana-Woodford Shale in May 2014. According to a company release, DVN acquired 50,000 net acres for just $249 million (50% working interest with Cimarex Energy), with the assets producing 5,800 BOEPD and holding 23 MMBOE of proved reserves.

In a note covering the announcement, KLR Group said the two companies were “essentially purchasing the assets for the value of the production.”Devon’s primary focus on the May 2014 acquisition was recompletions, and the company anticipated a payback timeline of less than three months.

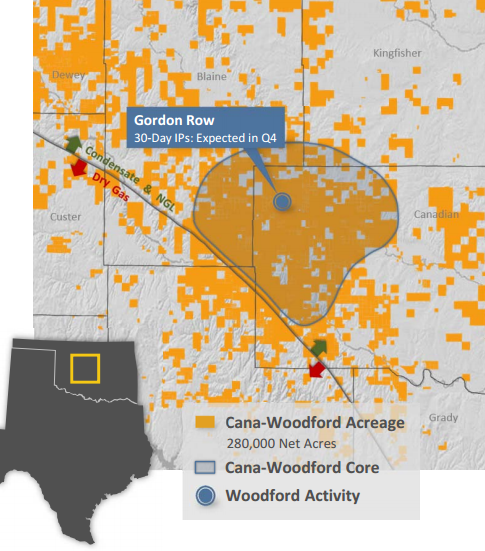

In its latest presentation, DVN listed its Cana-Woodford position at 280,000 net risked acres. The company averaged 64 MBOEPD of volumes in Q3’15 and is targeting a Q4’15 exit rate of more than 70 MBOEPD. As seen in the maps on the right, its position basically overlaps that of Felix Energy, giving it a much more pronounced role in the liquids portion.

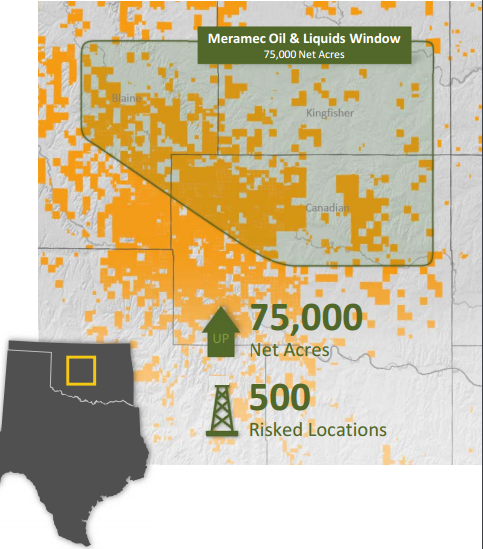

Its assets in the Meramec formation are surprisingly similar to Felix’s stakehold, with its footprint expanding about 75,000 net acres. The initial 19 wells in its program averaged 30-day initial production rates of 1,500 BOEPD at costs of about $7 million apiece. Devon planned on upping its rig count to five in Q4’15.

Tony Vaughn, Executive Vice President of Exploration and Production for Devon Energy, gleamed about the Meramec in the company’s Q3’15 conference call. “It really competes, in our mind, with our top-tier returns from DeWitt County, the Parkman in the Powder River Basin, and also the southern portions of Lea and Eddy County in the heart of the Delaware Basin,” he said, adding the company considers it to be a “top tier” asset. “We’ve characterized about 500 locations there. In my own mind, that’s conservative. So it’s going to be one of our go-to areas as we go forward.”

Quick Hit: The Valuation May Surprise You

The May 2014 price tag, net to Devon, consisted of $9,960/acre, $85,862/flowing BOE and $21.65/proved reserve BOE. West Texas Intermediate and Henry Hub prices averaged $99.74 and $2.24, respectively, for the previous month.

Using the $2 billion estimate for the Felix assets, Devon would pay $26,666/acre and $250,000/flowing BOE. For November 2015, respective prices for WTI and Henry Hub averaged $41.65 and $2.24. The monthly average for WTI was the lowest in more than 11 years.

You read the above correctly.

By the way, The Wall Street Journal points out that Newfield Exploration (ticker: NFX), an E&P focused intently on the STACK formation, is one of the top performing oil companies for fiscal 2015. The company also stands out in EnerCom’s E&P Weekly Benchmarking Report; its 41% increase in stock performance, year to date, is the third-highest out of 89 peers and is one of only 11 companies to improve its stock value in the same time frame. The median performance of the group is (41%).

[box type=”info” size=”small” style=”rounded” border=”full”]Like this article? Sign-up for OAG360’s “Closing Bell Report” and we’ll send you more.

[yikes-mailchimp form=”1″] [/box]