The oil and gas market is approaching the end of 2015—which will no doubt go down as a highly tumultuous year for the industry. In spite of the dive in oil prices, some companies have positioned themselves well for capturing the upside through advantageous acquisitions, reliable takeaway capacity, attractive hedges and low-cost production. Or a combination of factors.

Today’s focus is PDC Energy (ticker: PDCE), one of the fastest growing companies in the Wattenberg Field of Colorado. In the coverage universe of Capital One Securities, PDCE is one of only two companies positioned for 2016 growth of at least 35% while maintaining a debt/EBITDA ratio of below 2.0x. Meanwhile, projected capital expenditures for 2016 are expected to drop by about 11% as the company optimizes its drilling efficiencies.

Below are some of the strengths of PDC Energy:

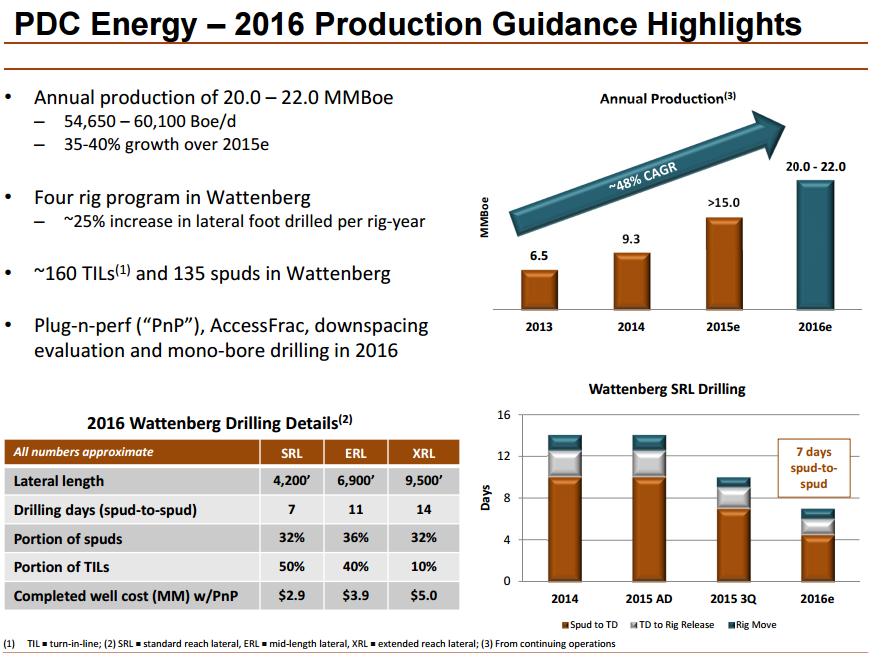

- Targeting 2016 cash flow neutrality with a budget of $450 to $500 million, while providing a year-over-year production increase of 35% to 40%. Operations are expected to be cash flow positive in the second half of the year.

- An ability to adapt to a changing market environment, backed by short-term rig contracts and held-by-production acreage. Its capital efficiency on a trailing twelve month basis is 284% – above the industry median of 106% and ranking third overall among its 22 mid-cap peers.

- Its 2016 production program is supported by a hedging program that covers 50% and 62% of oil and gas volumes, respectively, at approximately $85/barrel and $3.65/Mcf. The program held a mark-to-market value of $250 million as of November 30, 2015.

- Room to run: 70% of its reserves are classified as proved undeveloped, according to EnerCom’s E&P Weekly Benchmarking Report. The percentage ranks fifth overall out of 88 peers and is well above the industry median of 45%.

- Low operating costs. Data from EnerCom Analytics shows that PDC’s asset intensity (defined as the percentage of every EBITDA dollar required to maintain a flat production profile) is just 42%, meaning 58% of EBITDA revenue can be reinvested to shareholders or used for potential acquisitions. The percentage is well below the industry median of 108% and is the eighth-lowest out of its 88 peers.

“The balance sheet and financial strength of the Company will remain our top priorities in 2016,” said Bart Brookman, President of PDC Energy, in a company release. In a conference call following PDC’s Q3’15 results, Brookman added that PDC plans to “Maintain ample liquidity to execute our business plan and operational flexibility to speed up or slow down based on market conditions.”

The borrowing base was recently reaffirmed at $700 million and included a two-year extension on the credit facility to March 2020. Management expects less than $50 million to be drawn on its commitment of $450 million by the end of 2016.

Additional production upside is expected from a newly employed AccesFrac technology along with the plug-n-perf completion method, which has recently become the method of choice. Management says the techniques are providing “sizeable upside” and are believed to add uplift of 15% to its previous type curves of 600 MBOE. Management believes roughly 60 wells will be part of its 2016 backlog and anticipates working off the inventory in the first half of the year.