ExxonMobil (ticker: XOM), the largest publicly traded international oil and gas company, uses technology and innovation to help meet the world’s growing energy needs. ExxonMobil holds an industry-leading inventory of resources, is the largest refiner and marketer of petroleum products, and its chemical company is one of the largest in the world.

ExxonMobil ‘s fiscal 2013 production averaged 4.0 MMBOEPD, a decrease of approximately 4% from 2012, according to its Analyst Day on March 5, 2014. The 2013 total fell short of XOM’s guidance of 4.2 MMBOEPD, marking the fourth time in the last five years the company has missed production guidance. Pro forma for reported production, XOM has revised its 2017 production estimates to 4.3 MMBOEPD from 4.7 MMBOEPD, with anticipated yearly production increases of 2% to 3%. The company originally set guidance rates projecting 4.3 MMBOEPD by year-end 2014.

ExxonMobil plans on spending $39.8 billion in 2014 and expects to cut expenditures to $37 billion annually (9% decrease) through 2017. Liquids are expected to rise to 53% from 50% of its production stream during the stated time period. Three LNG projects in Australia and Asia are expected to start in 2014, including a Papua New Guinea project (32% working interest) that is believed to hold 9 Tcf of resources.

ExxonMobil’s Near-Term Outlook

The company will initiate 21 projects through 2017, adding an expected total of more than 1 MMBOEPD. Ten projects (eight with a liquids focus) are expected to begin in 2014 alone, with an added 0.3 MMBOEPD of peak production capacity.

The company reported a rise in its 2013 resource base to 90 billion BOE (28% proved) from 2012’s total of 87 billion BOE, with 6.6 billion BOE of the total added through discoveries and acquisitions. XOM believes it holds more than 40,000 MMBOE in unconventional resources, which is double the amount from 2005. Production from unconventional plays in expected to increase as the evolving industry continues to move forward.

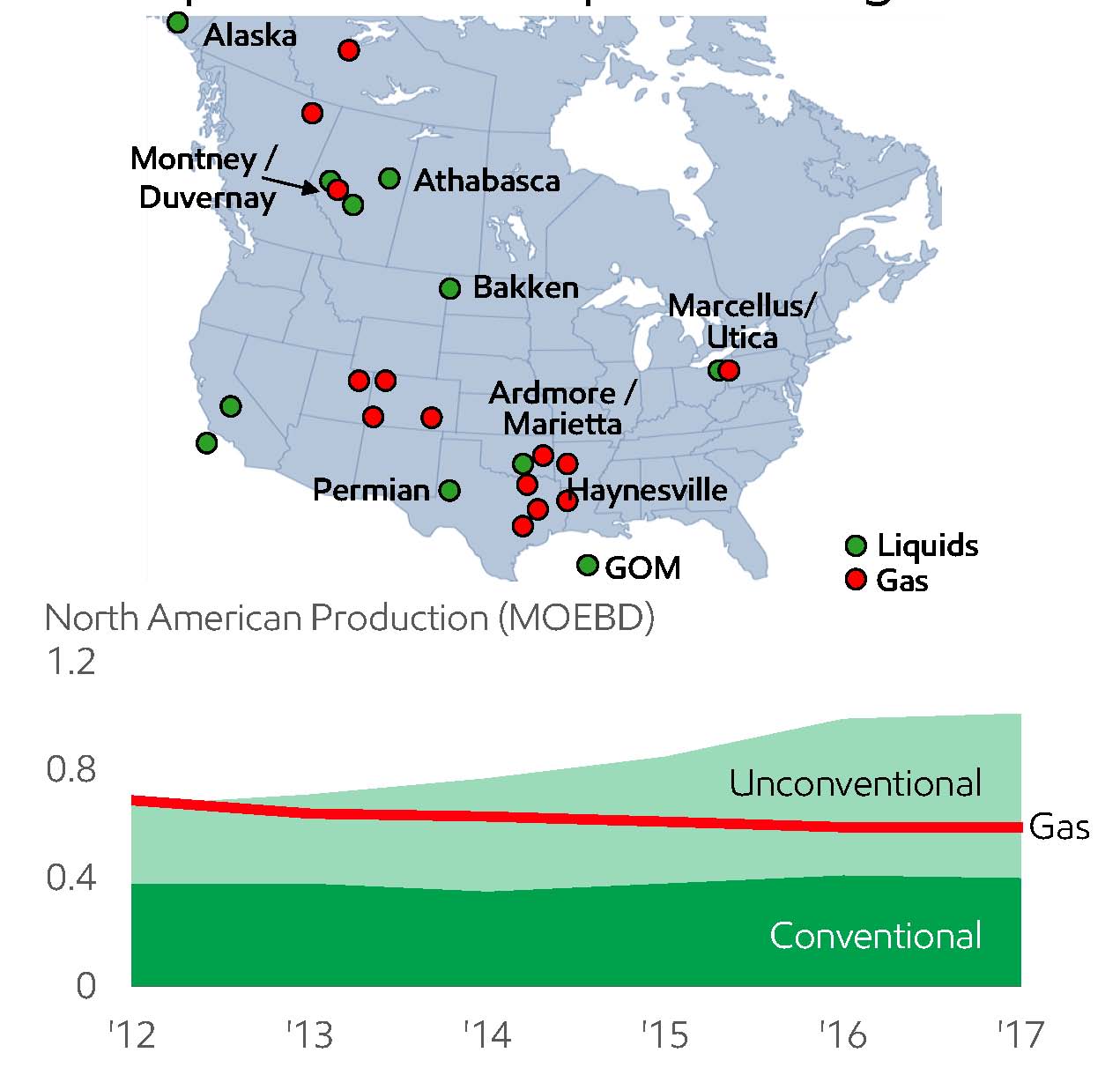

North America Focus

North America is expected to be a driver moving forward, particularly involving unconventional resources. The exploitation of liquids is a cornerstone of XOM’s future plans, and exploiting the resource from North American unconventional is a top priority. XOM estimates it holds more than 8 million unconventional acres on the continent and is currently running roughly 40 rigs across its North American properties. Eight of those rigs are in the Permian Basin, where the company holds more than 1.5 million acres and produces roughly 90 MBOEPD. Another ten rigs are in the Bakken, responsible for 65 MBOEPD of XOM’s production.

The Woodford Shale, however, is currently Exxon’s top unconventional target. Twelve rigs are running on its 280,000 acres and 30-day production rates rose 17% in 2013. Regional production has not been disclosed since Q2’13, but XOM noted totals are expected to increase 36% per year through 2017. Management said production in 2013 alone increased by 70%. If 2012’s total of 10 MBOEPD is taken into account with XOM’s guidance, Woodford production is in line to reach nearly 80 MBOEPD by 2022.

The boost in unconventional resources provides XOM with a unique ability to dial up production if demand rises. Its emphasis on liquid-heavy projects is reflected in the production forecast on the right. Mark Albers, Senior Vice President of Exxon, said 85% of its rigs are focused on liquids-related projects. Production from unconventional resources are projected to reach 225 MBOEPD by 2017, up from 2010’s total of 85 MBOEPD.

The United States’ natural gas potential will make it a chief exporter of the resource by 2020, according to the Energy Information Association. Current prices have prompted Exxon to reduce its emphasis on gas, but its massive acreage position and abundance of opportunities provides the company with availability to the resource if the need arises.

Peer Comparison

While Exxon has reduced its guidance rates and lowered production, other large E&P companies are preparing for near-term growth. Noble Energy (ticker: NBL) has forecasted compound production growth rate of 18% for the next five years, while operators like Devon Energy (ticker: DVN) set company production records in Q4’13. EOG Resources (ticker: EOG) believes its company will grow by 9% in 2014, fueled largely by its growing oil production in the United States.

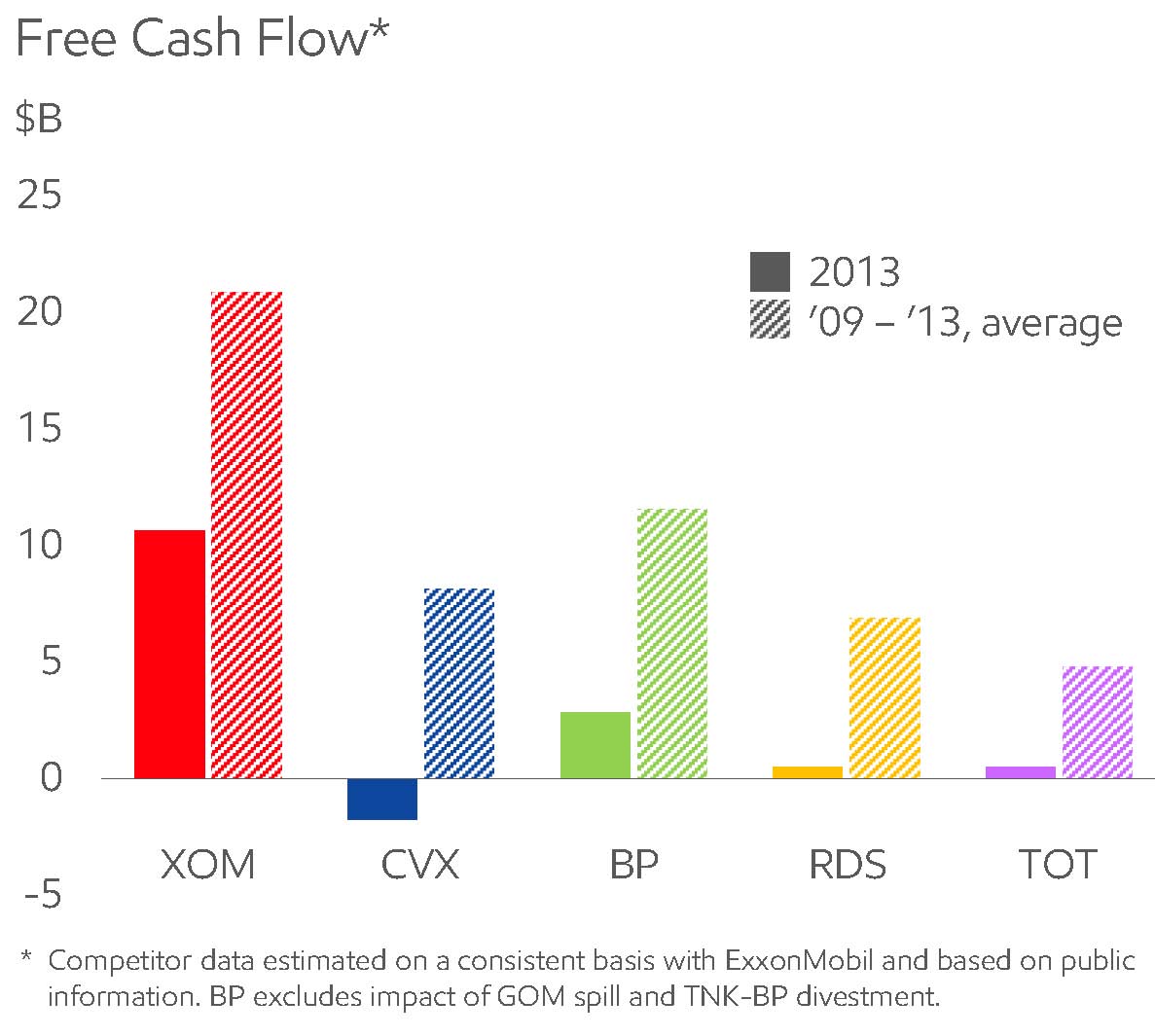

Despite a production decline, XOM anticipates oil extraction to contribute to free cash flow. The company anticipates reaching $17.3 billion in free cash flow by 2018 – up from 2013’s total of $11.2 billion ($15.5 billion excluding acquisitions). The oily returns have many operators projecting increases in equity, but XOM has historically surpassed its competitors in the free cash flow department. The company returned roughly 54% of such earnings to investors through dividends and share repurchases in 2013.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. As of the report date, neither EnerCom nor any of its employees has a financial interest in any equity or debt of any company mentioned in this report.