Cushing, Oklahoma, is the delivery point for United States West Texas Intermediate crude oil (WTI) traded on the New York Mercantile Exchange (NYMEX) and plays a large part in setting the price of crude oil in the U.S.

Storage at the facilities in Oklahoma represent about 60% of all crude oil working storage capacity in the Midwest and about 19% of all commercial crude oil storage in the United States, according to the Energy Information Administration (EIA).

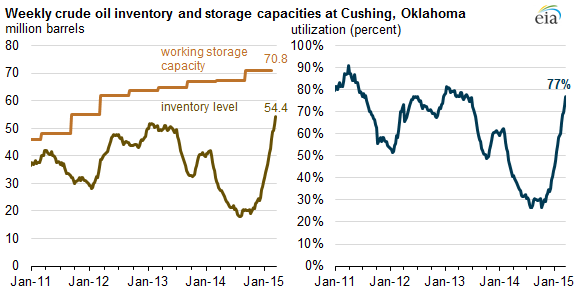

For each of the 7,826 residents of Cushing, Oklahoma, there are approximately 9,046 barrels of crude oil working storage capacity within an easy drive from home. That puts the massive oil storage tank complex in southeastern Oklahoma at about 70.8 million barrels (MMBO) of total working storage capacity.

To put the oil storage numbers in context, the EIA reported the U.S.’s total petroleum and liquids production at 13.9 MMBOPD in 2014. The U.S.’s nearest competitor, Saudi Arabia, was reported to be 11.6 MMBOPD.

Since November of last year, the crude oil levels in the tanks at Cushing have been rising as producers in the U.S. and Canada send their crude oil to

Cushing inventory topped out at 62.2 MMBO and 88% capacity on 4/17/15

Cushing. Many companies have chosen to sell their crude on the futures markets in an attempt to soften the blow of sharply reduced crude oil prices following OPEC’s Thanksgiving Day decision to maintain its level of production. And so the tanks fill up, awaiting future delivery of the commodity. Some people even raised concerns that the crude being held there might eventually reach the top of the tanks. In March of this year, the EIA released a report estimating that storage at Cushing was at 77% of working capacity due to the influx of crude being sold on the futures market.

Concern that crude oil might fill every tank to the brim after 100+ days of massive builds kept downward pressure on crude oil prices. For 17 consecutive weeks, Cushing saw above-average builds in inventories until a draw was made on inventories in the week ended May 1, 2015, pushing the price of WTI above $60 per barrel for the first time in 2015.

Cushing’s oil storage capacity is owned by an assortment of different names in the energy industry. Enbridge Energy Partners (ticker: EEP) owns 20.1 MMBO of storage, Plains All American Pipeline (ticker: PAA) owns 20.0 MMBO, Magellan Midstream Partners (ticker: MMP) owns 7.8 MMBO, and a number of other companies own the rest.

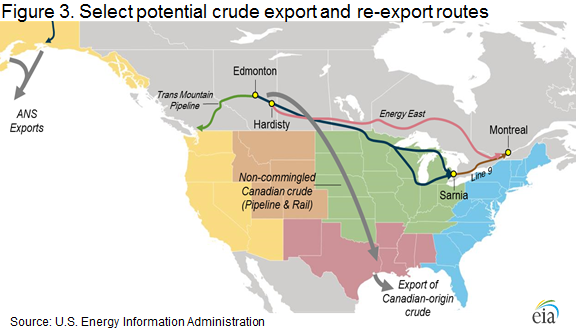

The Canadian Connection: how much of the oil at Cushing comes from Canada?

Estimates vary. The amount of crude coming down from Canada on a daily basis is estimated to be about 350 MBO by experts like Asset Risk Management’s Senior Vice President and Head of Fundamental Analysis Keith Barnett. That’s about a quarter of the total capacity.

The three main lines running from Canada to Cushing have a capacity of approximately 1.383 million barrels of oil per day (MMBOPD), according to data provided by Argus Media. The largest of the three, Flanagan South, has a nameplate capacity of 600 thousand barrels of oil per day (MBOPD). The second largest, the Keystone pipeline, has a nameplate capacity of 590 MBOPD, and the third pipeline, Spearhead, has a capacity of 193 MBOPD. Of the three, Spearhead is the only one that is estimated to be shipping near its nameplate capacity.

“We expect to see this continue indefinitely,” Barnett told Oil & Gas 360®. “The Enbridge Line 9 reversal will send some crude to Eastern Canada, as will Energy East,” but supplies of Canadian crude will continue to make their way to Cushing.

Data provided by Argus shows a different picture of how much oil is coming down from Canada. While Spearhead is the only line running near full capacity, Argus estimates that Flanagan South transports roughly 400 MBOPD and Keystone ships down about 230 MBOPD, totaling approximately 823 MBOPD traveling from Canada to Cushing.

Is the Canadian crude hurting prices?

There have been some concerns about how the addition of Canadian crude coming down into Cushing could be adversely affecting prices as tank levels peak. Today though, crude does not get trapped at Cushing the way it did before, said Barnett. “Crude oil will only get trapped in Cushing if someone pays to trap it there,” he said.

Art Hogan, Chief Market Strategist at Wunderlich Securities, told OAG360® that production is more of concern to pricing than the amount of crude flowing into Cushing. “What really affects prices is how much is already in storage, not how much is coming in on a daily basis,” Hogan said. “Of course, the crude coming from Canada is a piece of that puzzle, but overall production is affecting prices more than how much crude we receive from Canada.”

The ARM estimate of 350 MBOPD of crude coming into Cushing from Canada would not have a major impact on the price of oil, says Hogan. Hogan believes that until production flattens out and drops, prices will stay about where they are now.

Canadian crude is being re-exported through the U.S.

While Canadian crude might not be pushing oil prices down, it does enjoy a certain advantage over U.S. crude in terms of finding a way out of Cushing: Canadian crude can be re-exported while crudes produced in the U.S. fall under the 40-year old export ban. All it requires to export Canadian crude oil from Cushing is a license from the U.S. Bureau of Industry and Security (BIS).

“I’m not sure exactly how hard it is to get one of those licenses,” said Barnett, “but the process to get a permit to export to Canada is quite automatic. I don’t imagine that getting a re-export license for Canadian crude would be terribly difficult.”

The Bureau of Industry and Security told OAG360® that the application process for a license to re-export Canadian crude generally takes four to six weeks.

According to BIS representatives, “’foreign-origin’ crude oil can be exported (with a valid license) as long as it is not ‘co-mingled’ with domestic crude oil.” The BIS allows for minimal amounts of mixing between domestic and foreign-origin crudes through incidental contact in pipelines and storage tanks, but encourages applicants for a re-export license to explain how they will ensure as little co-mingling as possible in their applications.

How much Canadian oil from Cushing is exported from the U.S.?

There is no single entity in charge of the storage and movement of oil into and out of Cushing. Pinning down exactly how much Canadian crude leaves the U.S. from Cushing is difficult, says Barnett. “You can make assumptions about how much is being re-exported if you’re tracking ship movements,” he says, “but in the end it’s still just an assumption.”

EIA data shows between 171 to 185 MBOPD of Canadian crude reaching Texas in the last three months for which data is available (December – February). From the Gulf Coast, cargos of Canadian crude can be shipped around the globe.

Last year, Repsol (ticker: REP) purchased a cargo of 500 to 600 MBO of Canadian crude for delivery to Spain, reported Platts. The Spanish company co-loaded Western Canadian Select (WCS) crude from Freeport, Texas, with 500 MBO of Mexican Maya crude, which was shipped up to the United States from the Mexican port of Cayo Arcas.

“There are players at Cushing who have a physical reason for oil to be at those storage facilities—those who operate the pipes and storage tanks—but those who trade oil from Cushing have a different set of needs,” said Barnett. Those who are trading oil are looking to make profit on the arbitrage of Canadian crude overseas.

When the Repsol deal came to light last year, Platts calculated that price for delivery of WCS to both Mediterranean and Northwest European markets was favorable compared to Russian Urals heavy crude, Europe’s heavy-crude benchmark. The assessment done by Platts estimated WCS crude at about $88.60/bbl at the time, compared to $105/bbl for Russian Urals crude.

Prices today are a much different story. When asked if he thought sellers might get a better price overseas for Canadian crude oil today, Hogan said it was quite possible, but that the spread would be nowhere near the $16.40 it was a year ago. “They might be getting a few dollars more since there’s so much supply here in North America, but I doubt it’s very much,” he said.

The Energy Information Administration’s (EIA) Administrator, Adam Sieminski, told OAG360® during an exclusive interview that he believes most of what is shipped down to the coast is likely refined there as well. “I suspect that the extent of [exports of Canadian crude from the Gulf] would probably be somewhat limited by the fact that the appetite in the Gulf Coast for heavy sour crudes from Canada is probably pretty strong and, as a consequence, Canadian crudes would most likely be used [by refineries] in the Gulf Coast.”

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.