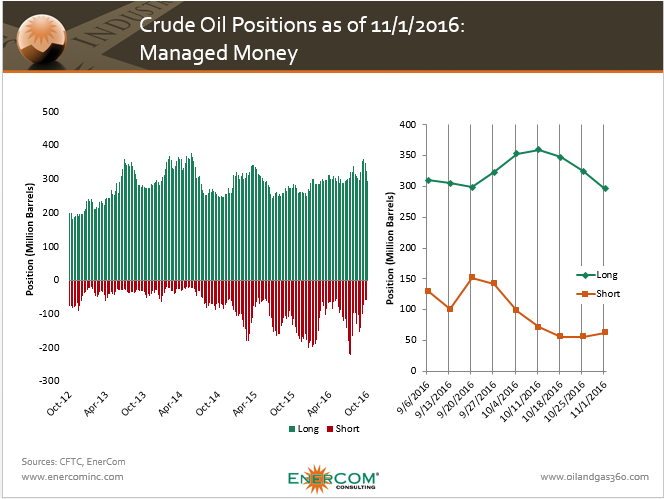

Money managers have reduced their bullish crude oil bets due to disputes among OPEC members on how to implement the output ceiling agreed to in late September. Managers reduced their net long positions by 9% (28 million barrels) the week before November 1.

According to Reuters, hedge funds ramped up their net long positions by 218 MMBO in the two weeks after the surprise accord was reached at the end of OPEC’s Sept. 28 meeting. The deal sparked a short-covering rally, resulting in the unwinding of many extra bearish positions. Prices have since returned to their pre-deal levels.

While managers have pulled back on their bullish stance, bearish outlooks for oil remain lower than before the OPEC agreement was announced. Managed money short positions are down 56% from September 27 (one day before the agreement was announced) and 52% less than October 27 of last year, when oil prices were still heading down.

Disputes continue between OPEC members about how the 32.5-33.0 million barrels per day ceiling should be shared. Many members continue to raise production and push actual output further above the ceiling agreed to at the meeting.

Producers, merchants, processors, and users as well as swaps dealers continue to be net short. Managed money often serves a market maker role, serving as a counter party to PMPUs and swaps dealers.

OPEC’s next official meeting will take place in Vienna November 30. The group hopes to come out of the meeting with a definitive production agreement among its members.

{kind=link}