Petróleos Mexicanos, or Pemex, is Mexico’s sole producer of crude oil, natural gas and refined products. The company provides Mexico with one-third of government income and was the ninth largest oil producer in the world in 2012. The oil and gas industry in Mexico has been nationalized since 1938, but production has declined every year since 2004 (24% overall).

However, Mexico’s President Enrique Peña Nieto and the government privatized the industry in December 2013 in an effort to revive Mexico’s deteriorating energy environment.

Mexico will hold its first bidding round in 77 years in June 2015, according to Pemex’s Energy Secretary. The bid for future development of the country’s hydrocarbons was submitted to the Energy Industry on March 21, 2014. Mexico, per conditions of the bid, will retain:

- 100% of its proven reserves, listed at 14 billion barrels of oil

- 83% of 2P reserves (24.8 billion barrels), leaving 4.2 billion barrels available to investors

- 31% of 3P reserves (118 billion barrels), leaving 36.6 billion barrels available to investors

Exact details of the locations have not been released.

How do United States Operations Translate to Mexico?

While Mexico has held a stranglehold on operations on its turf, private U.S. E&Ps focused both on and offshore are in a buying frenzy. Numerous operators in the Gulf, including Energy XXI (ticker: EXXI), have experienced growth through acquisition, exploration and exploitation. The Bureau of Ocean Energy Management in Louisiana has conducted four lease sales since 2013 and netted roughly $2.4 billion. Regular participants in the sales have included supermajors like ConocoPhillips (ticker: COP), ExxonMobil (ticker: XOM), Apache (ticker: APA), Shell (ticker: RDS.B), Chevron (ticker: CVX) and Anadarko (ticker: APC). The capital and offshore expertise (both elements that Pemex severely lacked) of many of these companies make them likely candidates in the bidding rounds.

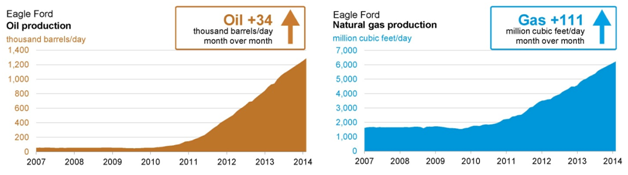

Onshore, production from the Eagle Ford Shale of Texas skyrocketed to more than 1 million barrels per day. The Texas Railroad Commission reports more than 11,000 drilling permits have been issued since January 2011 and 250 rigs are currently running in the region. Oil production has increased by 408% during the given period. A study by IHS shows roughly half of the Eagle Ford’s 38,000 square mile field lies in Mexico. However, shale production by our southern neighbors is scarce and hydraulic fracturing is uncommon. Furthermore, the region is home to drug trafficking, gang wars and theft that could potentially pose a hazard to oil workers. Considering most Mexicans weren’t too pleased with their country’s energy reform, companies may be hesitant to jump into the region.

Energy Independence Could Receive a Boost

The United States attained the title of the world’s greatest energy producer in 2013. Its close partnership with Canada and booming production made the country less dependent from overseas imports. With Mexico joining the fold, the need for oil outside of North America could drop even more. Since 2008, United States oil production has jumped by 30% and Canadian imports have risen 25% (accounting for roughly 33% of all crude imports). Mexico has averaged about 10% of the U.S.’s crude import makeup during the time period. In the meantime, crude imports on a worldwide level have dropped by 26%, including a 40% decrease in reliance from OPEC members.

The United States has capitalized on Mexico’s struggling industry by exporting natural gas to the energy-thirsty region. Gas exports have climbed 65% since 2008 and are transported almost entirely through pipelines. Ongoing relations between all North American countries can only strengthen the United States’ energy portfolio.

Mexico’s Entry into Privatization may be Difficult

The full-scale shift from nationalization to privatization is not as easy as it may seem. A report from Control Risks Group titled “Mexico’s Second Revolution” details several potential problems with Mexico’s adaptation to its energy reform. The report reads:

“It would be uncharitable – and inaccurate – to ignore the achievements of Peña Nieto’s reform programs to date… But the passage of legislation and the implementation of the details are not the same thing. Often, the interpretation taken by a government’s myriad bureaucracies and courts can be affected by lobbying and less savory forms of pressure by interested outsiders, blunting or changing the emphasis of language now written into law.”

While Mexico may hold the world’s eighth largest oil reserves and sixth largest gas reserves, Control Risks believes the country’s unfamiliarity with an expanded energy sector and risk-by-production mantra for operators can be troublesome. The report outlines governmental responsibilities for the energy sector makeup is spread broadly across seven sectors – two of which are entirely new. In addition, the report says operations governed by a state-owned enterprise can be “fraught with pitfalls” due to unforeseen taxes and levied fees. The report also points out the government-dominated process can hamper regular operations due to the required learning curve. As a result, the Ministry may enforce rules and regulations that ultimately inflict more harm than good. Finally, the midstream network must not price itself out of the market. Considering Mexico has not shared oil revenues with a partner in more than a generation, agreeing on a fair price may be an issue.

However, energy reform has been the staple of President Nieto’s campaign and he has assured the change will revive his country’s economy. Knocking down a 75-year old piece of the Mexican Constitution is already an achievement in itself. Control Risks Group points out Mexico has plans in place to double the capacity of its ports by 2018. International investment is starting to trickle in, and General Electric (ticker: GE) announced plans with Mexico to develop offshore infrastructure by signing a contract on April 8, 2014. Canada-based ScotiaBank also announced it plans to invest $10 billion in Mexico projects through 2018. Demand in bonds, according to Pemex, was at an all-time high when it sold $4 billion worth in January 2014.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. A member of EnerCom, Inc. has a long-only position in Energy XXI and Shell.