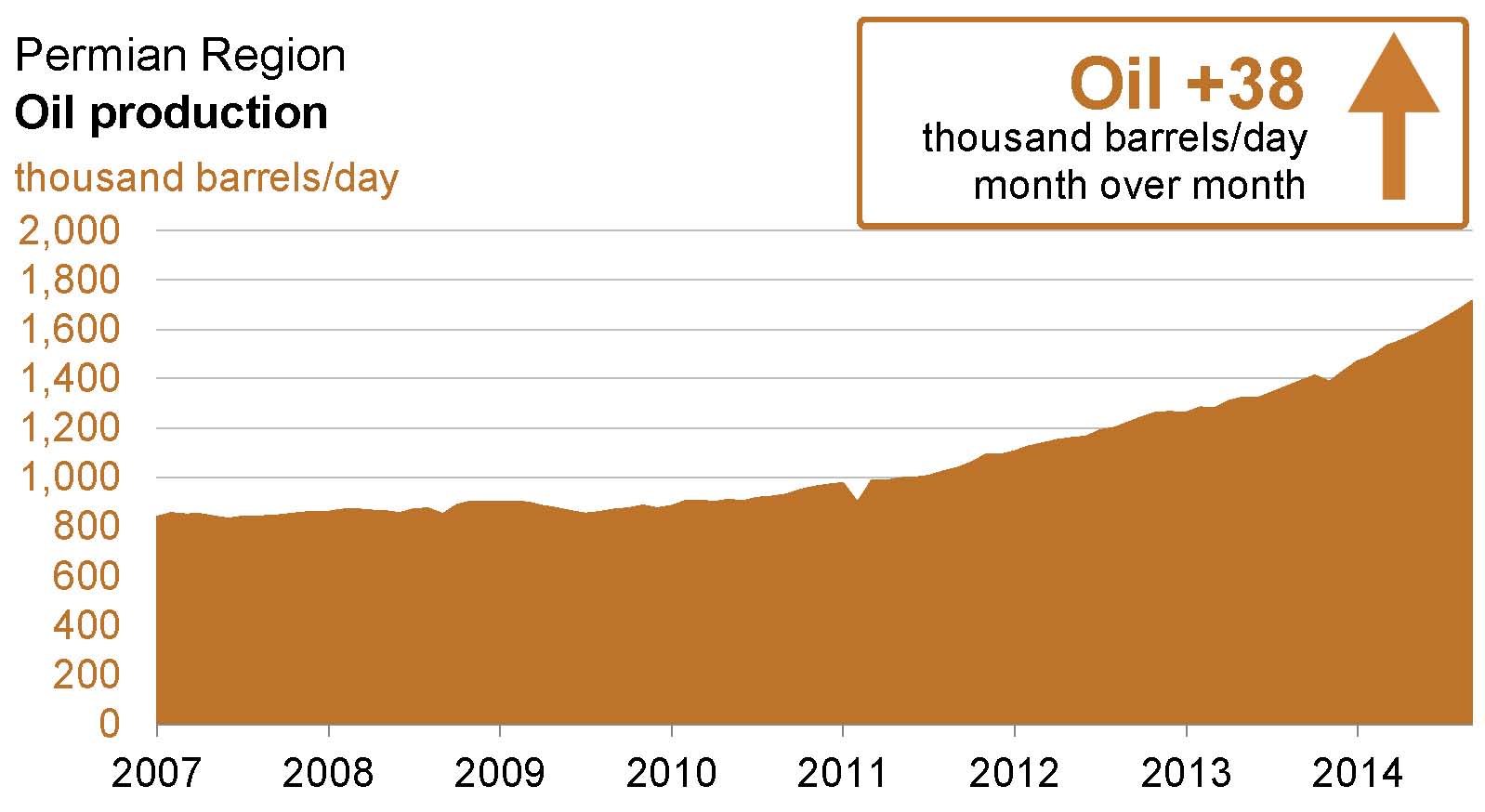

Production in the Permian is at an all-time high, but its prices per barrel are a different story.

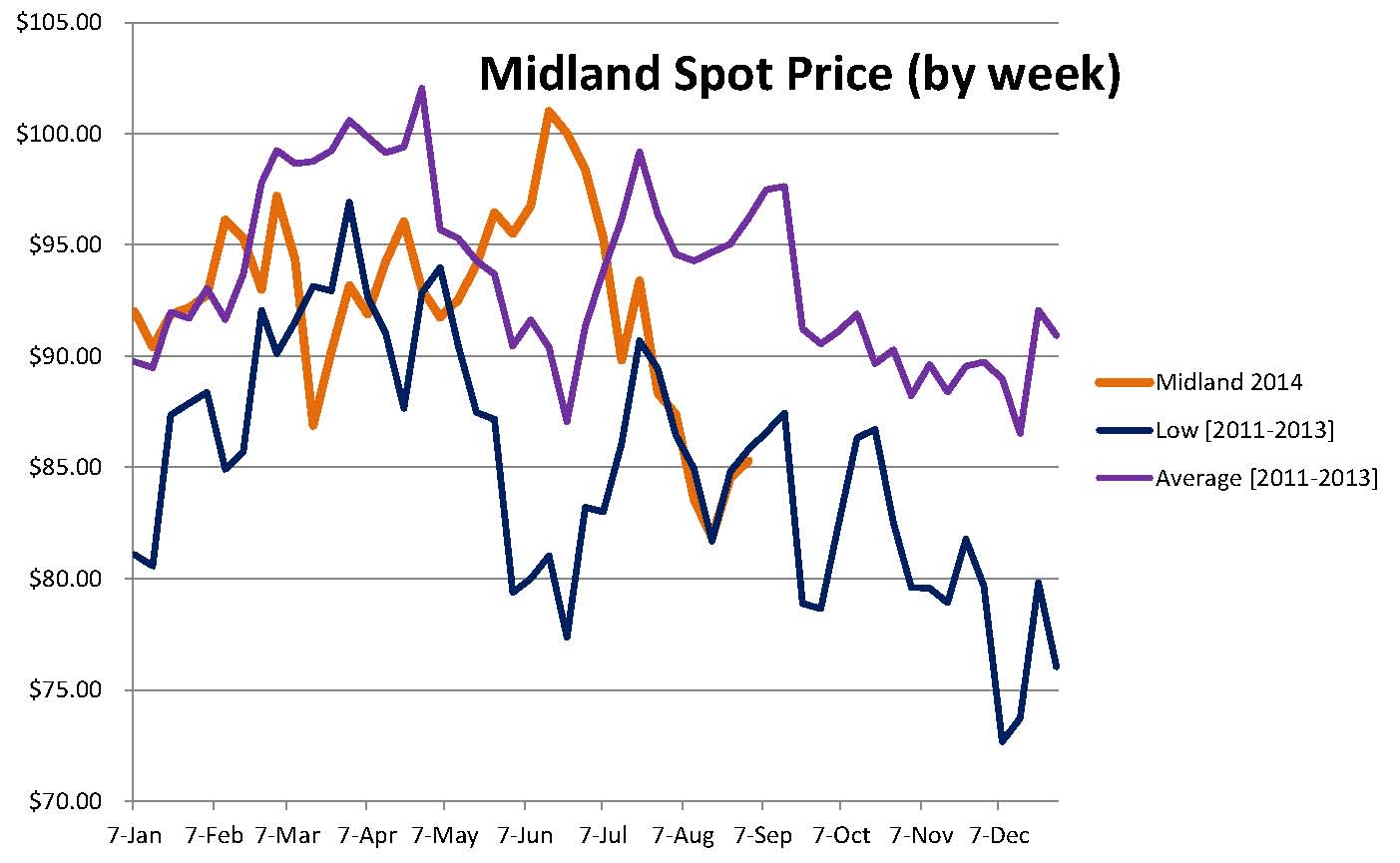

Spot prices at the Permian’s main hub in Midland, Texas, are trending among three-year lows. Its differential on August 25, 2014, was roughly $8 below the West Texas Intermediate (WTI) price and approximately $17 below the Brent spot price. The growing differential between the two chief spot prices has widened in the midst of growing supply in the United States and political unrest overseas.

Brent dipped below the $100 per barrel threshold on August 18, 2014, marking the first time the spot price had fallen below the mark since May 1, 2013. WTI, on the other hand, has dropped by more than $10 per barrel since its ending price of $104.29 on July 30, 2014.

Oversupply Concern

Many questions regarding the price differential were aimed at Permian operators in their respective breakout sessions at EnerCom’s The Oil & Gas Conference® 19 last week in Denver. According to a note by SunTrust Robinson Humphrey on August 21, 2014: “The recent success of big new oil wells in the Permian and sizable new gas wells in the Utica/Marcellus have led to a mismatch between the amount of oil or gas being produced and the ability to move it… The price of oil was $73.48 per barrel in Midland on Tuesday (8/19) versus the benchmark pricing point for U.S. crude contracts in Cushing OK at $94.48 per barrel. The $21 Permian discount was the widest since at least 1991, when regular tracking of the price differential began.”

Energen Corp. (ticker: EGN) in particular fielded many questions about its current setup in the Delaware Basin and if any constraints will hamper future development.

The rapid rise in Permian horizontal drilling has contributed to the boom. According to the Energy Information Administration (EIA), the Permian had less horizontal drilling rigs than both the Eagle Ford and Williston at the beginning of 2013. By the end of the year, the Permian climbed past the two other basins and had 215 rigs in operation – more than four times the combined increase of the Eagle Ford and Williston.

The EIA’s 2014 Annual Energy Outlook anticipates production from tight oil sands will lead to a production increase of 48% by 2019 in comparison to 2012 volumes. The Permian currently accounts for 35% of all crude production in the United States, according to the EIA’s most recent Drilling Productivity Report. A Raymond James note on August 25, 2014, concurred with market assessments. “The Permian midstream system is stretched, and the stocks are feeling it,” the note said.

Market Playing Catch-Up

The high production rates may be pressuring E&Ps, but The Market Realist believes the volume is opening up doors for other players in the industry. “The spread widening is potentially creating opportunities for midstream companies with transportation and logistics assets based in that region. So, the price differential between WTI Midland and WTI Cushing benefits companies with assets that can move crude from a low priced region to a higher priced region. It also favors companies that supplies oil to the demand source such as a refinery.”

The report adds, “Over the longer-term, sufficient investment from midstream companies will likely serve to balance the crude oil supply/demand dynamics in the Permian.”

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.