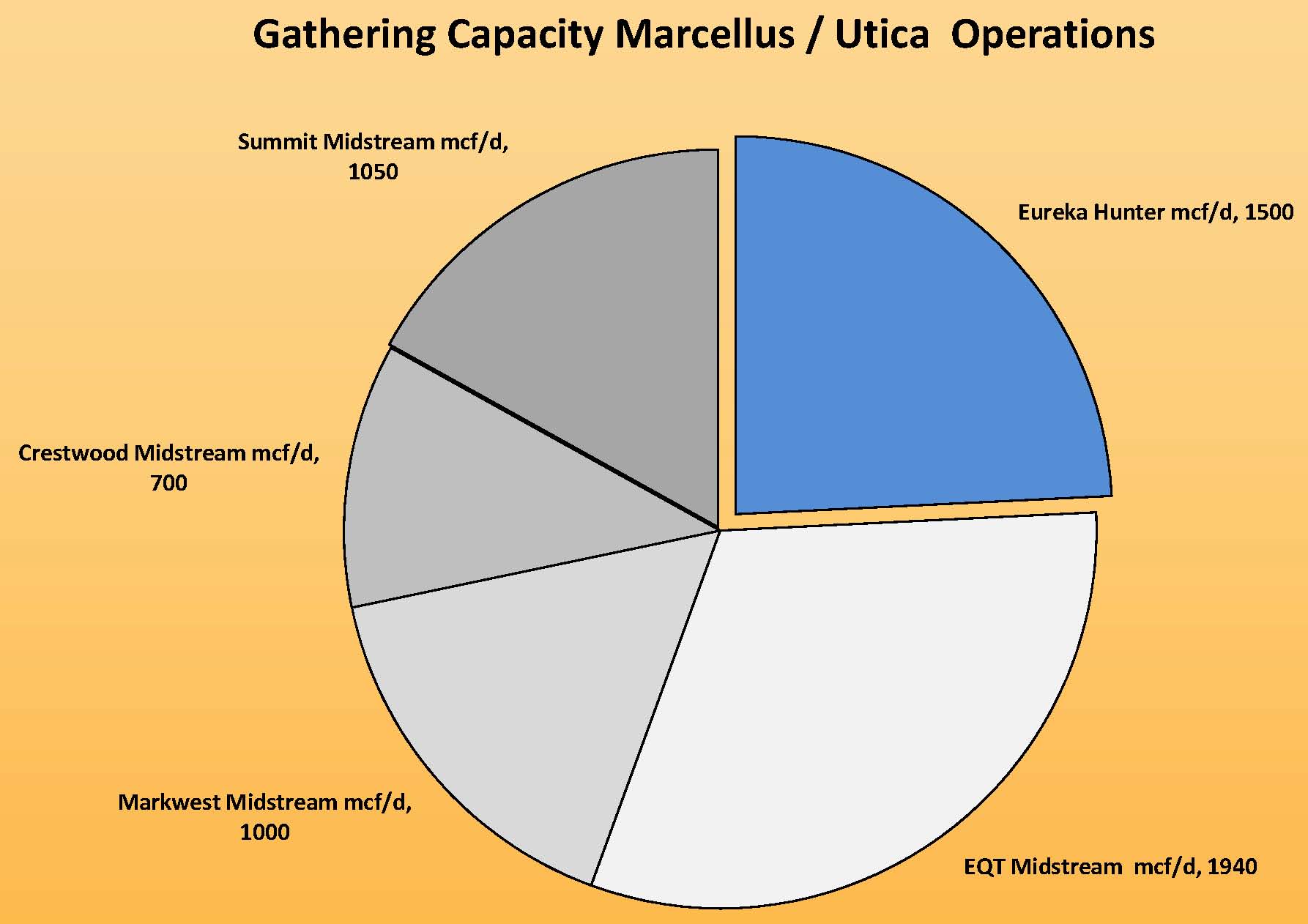

The month of September was one for the record books for Magnum Hunter Resources (ticker: MHR). The Marcellus/Utica E&P reported initial production of 46.5 MMcf on its Stewart Winland 1300U well – the highest flow rate of any well to date in the Appalachia region. Eureka Hunter, its midstream division, also set a new company record of 316,500 MMbtu/d in takeaway rates. The rising production and takeaway rates are expected to continue their upward trend, and management believes MHR can more than double its Q2’14 volumes to exit 2014 producing 32.5 MBOEPD.

Oil & Gas 360® interviewed Gary Evans, Chairman and Chief Executive Officer of Magnum Hunter Resources, to discuss what’s next for the growing E&P.

OAG360: Many companies are paying big to move into the oil plays, but Magnum Hunter is focusing more and more on the Appalachia. What’s the reasoning behind your strategy?

Evans: In the Appalachia, we have very wet Marcellus and a combination of both dry and very wet Utica. So, it’s almost like the inverse of a Permian, Bakken or Eagle Ford, but the switch is not as black and white in terms of going from oil to gas. We’re a company that’s weighted more towards gas, but we still have lots and lots of liquids.

It really boils down to rate of return. This business is all about the quality of the rock and we believe our acreage position is in the core of the Marcellus/Utica, and therefore we are getting better results. The kind of commodity is indifferent here because we have such good quality rock. The rates of return we’re generating in the Marcellus/Utica are two to three times greater than the returns we were getting in the Bakken.

We just set a record well and we think we can duplicate that many, many times. There’s nothing that leads us to believe that these won’t get better. I have no doubt in my mind we’ll be putting on 50 MMcf/d wells.

OAG360: You believe your operations team has the Marcellus “code” down. How are they progressing in the Utica?

Evans: The Utica is, from a geological standpoint, a much more difficult regime. Especially in the areas where we are, because there is some faulting and those faults are typically resource charged. From a technological standpoint, we’re constantly changing the way we do things, to be safer and be better prepared for when we hit these faults. We’re also looking at doing more seismic in the area. You’ll see some announcements within our own organization soon about some management changes in order to reinforce our team to be able to address that. The good news is, we have a very high pressure resource play, and that will result in very high returns.

OAG360: Have you noticed any changes in the industry regarding acreage pricing or midstream accessibility near your core area?

Evans: No, mainly because we already have almost everything tied up. All we’re buying is infield properties, and the fact that we have such a large footprint already pretty much keeps our competition away.

OAG360: Is that a big advantage over your peers?

Evans: I believe we have several. First of all, we’re local and we have more than 300 employees there. We bought two local companies that were 25 years old and kept the name (Triad Hunter). So we’re viewed more from the neighbors as somebody who’s local rather than being a company from out of state.

We have drilled many wells and have our own pipeline. The landowners have actually seen our operations and want us to come in and drill a well for them because they’ve seen us being efficient and responsible. We had some companies come in before us that left a bad taste in the mouths of some of the residents, but that has actually helped us because we’re deemed as one of the local good guys.

What can we expect from an infrastructure standpoint after Eureka Hunter goes public next year?

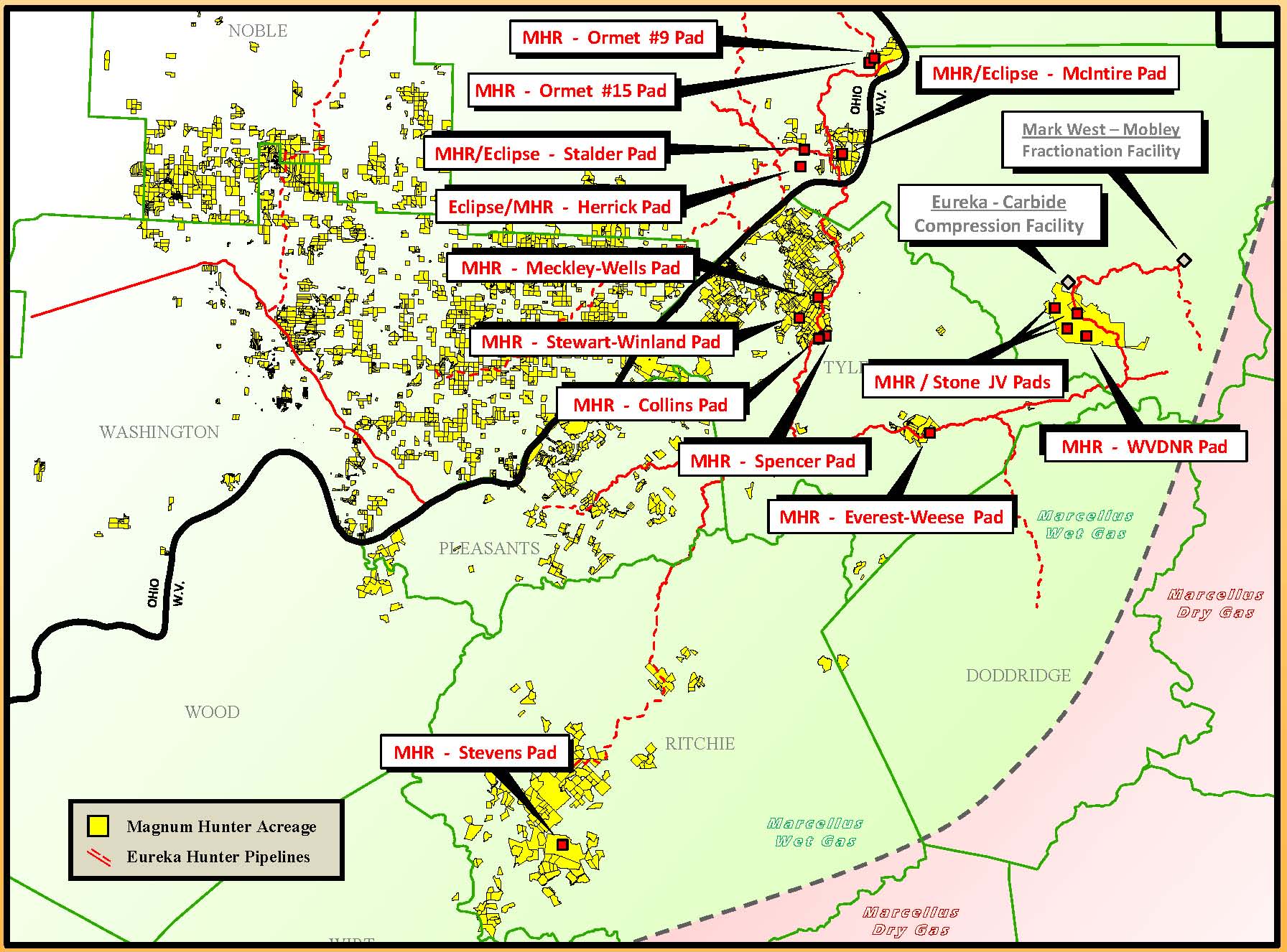

Evans: Infrastructure will continue to grow. We have four crews out there building pipe for Eureka Hunter. You’ll see us much more involved in cryogenic processing. Today, we have nine producers flowing into Eureka and that number will probably grow. You’re going to see not just a wet line, but dry lines also because the Utica on the southeastern portion of the play is very dry gas and there’s no reason to be comingling dry gas with wet gas. So that allows us to build new lines that will flow directly into trunk lines, so you’re going to see a lot of different types of lines instead of just one pipeline.

OAG360: Can you comment on the recent divesture of MHR’s Bakken properties?

Evans: We’ve sold $125 million in assets this year. Our goal is to be out of North Dakota by year-end, and that should be another $400 million to $500 million in assets. That completely changes up our balance sheet and we think that’s the right move.

OAG360: Thank you for your time.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.