Raymond James Cuts Long Term Henry Hub Price to $3.25

The industry buzz word for the last several years has been “liquids,” as the majority of companies have focused on oil-rich plays and realigned drilling operations to higher condensate areas. Companies like Penn Virginia (ticker: PVA) and Callon Petroleum (ticker: CPE) strategically shifted their portfolios to oil basins from their traditional dry gas projects in search of the highest return. As oil prices climbed above $100/barrel last year (trading at four times the amount of gas, on a BOE basis), natural gas prices were somewhat of an afterthought.

Traders and companies are scrambling in the aftermath of the oil price shock, but the steep downswing is somewhat of an old hat for natural gas-centric companies who survived the decline in the late 2000s. From about 2005 to 2010, gas prices swung violently from $4/Mcf to as high as $10/Mcf, affected largely by seasonality and unforeseen disruptions. Today, prices hover consistently in the $3 to $4 range but have remained below $3/Mcf since mid-May.

Shaky oil prices are still in search of price stability. Various factors such as supply/demand imbalances and political influences consistently rattle the oil cage, but the gas market, on the other hand, has found its range. But, similar to oil, it is still trying to even out a supply surplus like the one that led to oil’s inevitable decline late last year.

Downward Price Pressure Remains

Last week, the Energy Information Administration projected natural gas production across all major shale regions will decline for the first time since the inception of its Drilling Productivity Report in October 2013. The decline, however, comes on the tail-end of Northeast production reaching an all-time high of 20.4 Bcf/d in the latest Natural Gas Weekly Update. The expected decline took more than six months to finally come to fruition after E&Ps companies pulled back on development projects and slashed their drilling budgets. The latest Baker Hughes rig count places 202 United States gas rigs in operation – down 40% from one year ago.

The slow process of leveling off the supply fundamentals is increasingly stretching further into the future. In a note on August 31, 2015, Raymond James & Associates clipped its long-term Henry Hub forecast to $3.25/Mcf, down from its previous bet of $3.75/Mcf. “Put simply, there is plenty of U.S. natural gas to meet rising demand at prices of $3.25 (or possibly lower) for the next five years,” the firm said. Factors like lower drilling costs and an unexpectedly weak outlook for industrial demand growth have pulled down future estimates.

From an outside perspective, the possibilities of natural gas use seem both abundant and endless. The versatile fuel was viewed as the successor of coal to provide cheap electricity to consumers. However, the previously mentioned lower demand from the industrial side, combined with lower than anticipated future demand from China, India and Japan, is clouding the attractive possibility of natural gas prices recovering.

A study published by the University of Oxford’s Oxford Institute for Energy Studies in December 2011 may be dated but is still accurate in terms of natural gas evolution. The study, entitled “The Outlook for U.S. Gas Prices in 2020: Henry Hub at $3 or $10,” reviews the effects of gas prices sloping off and the prospects of new markets revitalizing gas prices. A factor discovered by the study, then in 2011, still holds true today, as it explained: “Erosion of natural gas prices occurs largely because new sources of supply seek markets where natural gas is already being utilized. Patterns of demand use in the U.S. are well established. Creating new demand, for instance through natural gas vehicle transportation, is attractive but historically fraught with difficulty.”

Lagging infrastructure has limited the effectiveness of natural gas vehicles. Honda discontinued its compressed natural gas and hybrid Civic models in June, intending to head to a more electric-based approach in future models. Management directly mentioned the scarcity of fueling stations as too much of a hurdle, combined with the dropping price of gasoline.

Gas Prices Overlooked

Henry Hub prices, though still obviously significant, have become somewhat of an afterthought in a hydrocarbon market hanging on every piece of action in the oil market. In the Raymond James note, the firm admitted not previously changing its gas forecasts was partly due to a lack of outside interest. “Frankly, we have not really been tightly focused on this side of the U.S. energy equation since investors seem to have totally forgotten about U.S. natural gas,” says the note. “We NEVER get questions on U.S. gas prices!”

The reduced future gas price estimates are placed squarely on booming production from the Appalachia region, which has been fueled by well efficiencies and breakneck extraction. Since 2012, the Marcellus/Utica area has driven 85% of shale gas growth and per well efficiencies have multiplied exponentially. In the meantime, infrastructure has been tripping over itself in an attempt to catch up, forcing some bottlenecks in select regions. The dropping rig counts are finally beginning to show signs of a slowdown, as previously mentioned in the EIA report, but Raymond James believes a different factor will have a great effect on gas prices.

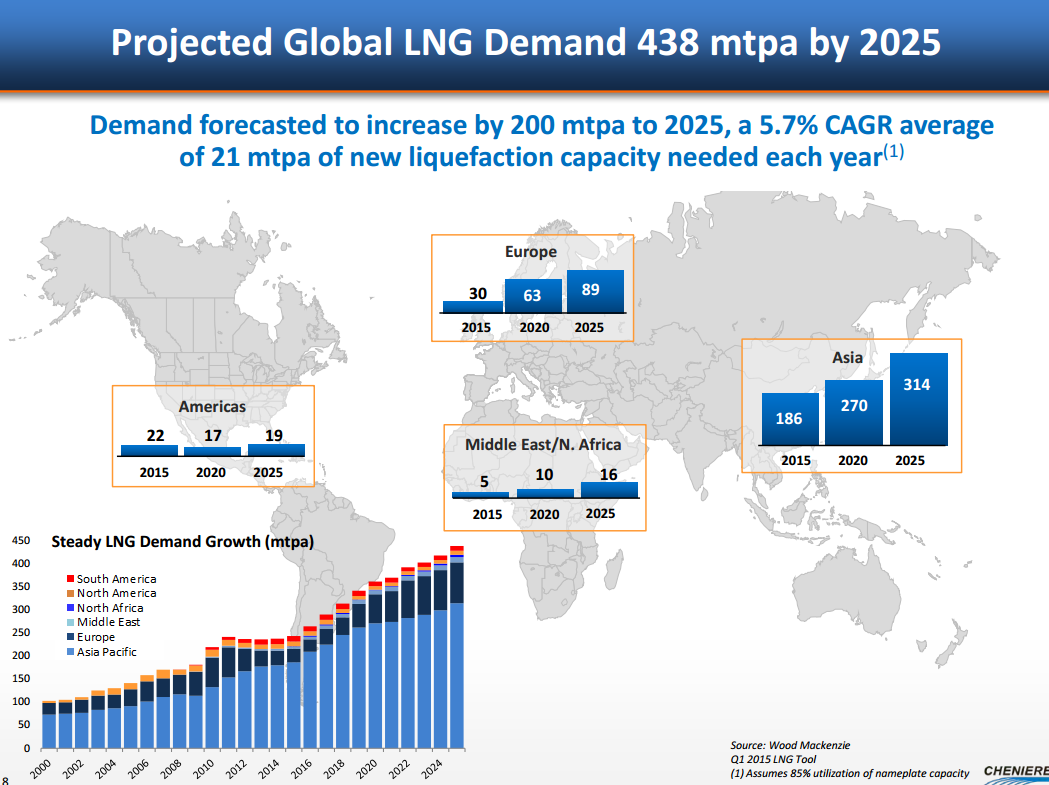

“The bigger issue is that estimated Marcellus growth (~1.5 Bcf/d) combined with soon-to-open pipeline takeaway capacity (of which we have identified ~4 Bcf/d) is set to more than compensate for price-driven associated gas production declines elsewhere,” the firm says. “Of course, LNG projects should help in 2016/17, but there should still be more than enough gas at $3.25/mcf to satisfy this growth… While there are reasons to believe that the demand picture will look more encouraging in 2017 and beyond, the industry’s ability (and willingness) to deliver low-cost supply represents an offset to any gas demand resurgence.”

LNG Exports: Coming Global Market for U.S. Natural Gas

In an exclusive interview with Oil & Gas 360®, Charif Souki, CEO of Cheniere Energy, keyed in on the low price of natural gas. Souki spoke about the U.S.’s cost advantages over other global LNG export projects. “We have the lowest cost of gas in the world. We have a very, very low cost of infrastructure building, including our own terminals. It gives [the U.S. LNG export projects] a huge competitive advantage compared to the rest of the world in terms of building liquefaction capacity and supplying the world with LNG,” Souki said in the interview.

Cheniere Energy expects to begin production of LNG at its Sabine Pass, Louisiana, plant in late 2015. The company already has contracts in place to ship LNG to European and Asian customers.

Safe Haven

The stability in the market prompted a piece from The Wall Street Journal to declare natural gas as a “safe haven” in an energy market that has seen its fair share of bumps and bruises this year. A note by Citigroup said the reliability of prices “potentially makes gas an oasis amid market turmoil,” backed by the inconsistencies of oil prices. With the winter season looming and production rolling over, there is potential upside to prices that are currently trading below $2.70.

“The volatility, when it comes in natural gas, it comes like no other asset class,” said George Zivic, portfolio manager for the Oppenheimer Commodity Strategy Total Return Fund, in an interview with The Wall Street Journal. “It is by no means benign. It is just benign now, at the end of the summer, when we have a lot of supply.”