OPEC and Russia looking hard at ending cuts, but maybe not till after end of the year

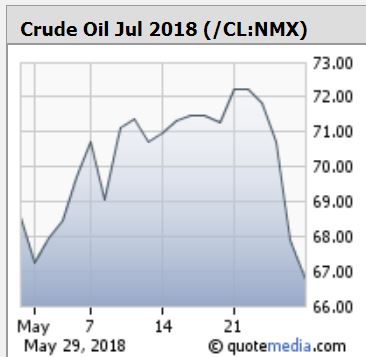

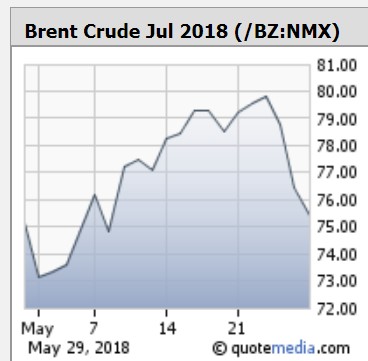

Reacting to comments from the Saudi oil minister, crude oil prices fell more than $5 per barrel between Friday and Tuesday. Brent crude oil grew from about $73 per barrel at the beginning of May to kissing $80 last week, then falling to just over $75 by the close of trading on Tuesday. But oil rallied Wednesday when some reports came out saying OPEC will keep crude production status quo until year end.

What caused the quick drop

Crude prices began falling when the Saudi oil minister told the St. Petersburg economic forum that Russia and OPEC nations were in talks to increase their oil output.

The production cuts that lifted prices from the $50s to the $70s per barrel during the past year have eaten away at the oil glut and most analysts believe that supply and demand have evened out. “It is the intent of all producers to ensure that the oil market remains healthy, and if that means adjusting our policy in June, we are certainly prepared to do it,” Saudi energy minister Khalid Al-Falih told the panel.

Saudi Arabia’s energy minister said OPEC and Russia could together increase production by approximately a million barrels. He indicated that a decision will be made or a plan rolled out after OPEC has its 174th ordinary meeting in Vienna on June 22.

Two of OPEC’s producing members, Venezuela and Iran, because of its deteriorating production and economy, or from the effect of sanctions, respectively, have pushed OPEC/non-OPEC production cut-compliance to rates between 150% to 160%. And that opens the way for other producers to fill the void, something that U.S. shale has been doing at a steady pace thanks to record-breaking production growth.

So far, oil prices have fallen by about 8% since the May 25, 2018 announcement. The faster and farther drop in price for WTI added to widening the spread between the two global benchmarks—WTI and Brent—to more than $7 a barrel for the first time since mid-2015.

“Two years ago we pulled supply. I think in the near future there will be time to release supply,” Al-Falih said at the forum. “It’s likely that it will happen in the second half of this year. We’ve had intensive discussions [with Russian energy Minister Alexander Novak], and I think we’re aligned on that,” the Saudi official added.

“Whether it’s a million barrels [or] more or less, we think we’ll have to wait until June before making that announcement,” he said.

What about U.S. shale?

The shale revolution has without question transformed the American energy industry, making the U.S. officially the world’s largest producer of hydrocarbons. The country has now retained this crown for five years in a row, surpassing both Russia and Saudi Arabia. The U.S. produced just under 30 MMBOEPD in 2017, an all-time record.

The U.S. shale industry learned how to navigate continued production growth in a low price environment during the 2014-2016 downturn, albeit not without a slew of painful bankruptcies and some consolidation. But the nimble producers trimmed the fat, reduced debt and made themselves and their drilling processes much more efficient. They essentially cracked the code on how to produce a lot of oil and make money doing it, even in the $50 per barrel range–half the triple digit oil that launched the shale boom. And some companies say their breakevens are even lower–down in the $40s for certain plays. The Permian Basin being the most notable.

But as to whether the U.S. shale producers will continue their record-breaking pace if the OPEC/Russia cartel creates another price drop, it’s going to depend on how deep and long the price correction is. Most analysts don’t expect to see another long lasting price downturn.

West Texas Intermediate crude oil climbed back over $68 on Wednesday.