The Organization of Petroleum Exporting Countries (OPEC) is scheduled to meet for the first time in 2015 on June 5 in Vienna. Assumptions point to the meeting being a terse exchange between the 12 members in an attempt to fulfill their respective end goals in the oil market. Brent oil prices at the time of the meeting are expected to be at their lowest level in roughly six years.

Saudi Arabia has drawn ire from not only its fellow OPEC members, but from other major oil-producing nations, as the world’s top oil-exporting country has ramped up production levels rather than restricting its output. Francisco Blanch, head of global commodities for Bank of America, called OPEC “broken” in a January interview with Bloomberg. However, the Saudis are not the only member opening the throttle in the new commodity environment; Iran is itching to increase its volumes pending an ease on its sanctions, and Iraq has boosted its output on a monthly basis since the November 2014 meeting, despite being mired in a bitter conflict.

The conundrum among OPEC producers has become apparent; all want market share and high prices, but the two elements cannot coexist, thus forcing the member nations to take sides. In this market, however, the market share fighters hold precedence, and those fighting to defend prices have no choice but to continue production in order to keep pace with their peers.

Who’s in the Driver’s Seat: Gulf Countries

Saudi Arabia, backed by 265 billion barrels of oil reserves (second highest globally), has been steadfast and undeterred in its decision to maintain its output stemming back to the November 2014. In fact, the OPEC leader boosted production by 0.2 MMBOPD per month from January through March.

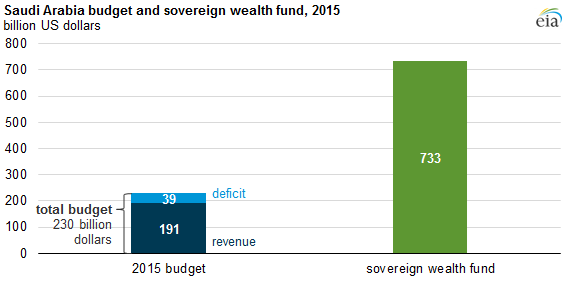

That’s not to say the price cuts haven’t affected the world’s largest oil exporter, at least in the short term. The oil and gas sector accounts for about 50% of Saudi’s gross domestic product, but the country is supported by $733 billion in its sovereign wealth fund. The Energy Information Administration projects the Saudis to operate at a loss of $39 billion in 2015, amounting to just 5% of its existing fund.

Information regarding Iran is not provided by the EIA due to the murkiness surrounding sanctions, but months of talks are signaling a proverbial light at the end of the tunnel for the politically embattled country. If sanctions are indeed lifted, Iran’s oil minister said as much as 1 MMBOPD of exports could be added within just months. Many analysts believe Iran is posturing to a certain extent, but the country is reportedly generating interest from its fair share of international investors, including Russia’s Lukoil. Iran has been forced to draw from its sovereign wealth fund since oil prices went south. The International Monetary Fund estimates Iran needs a breakeven price of approximately $130 per barrel.

Lukoil has also been scouting the prospects of additional production from Iraq. The war-torn nation, however, has fallen behind payments to international investors by about $18 billion in 2015 alone, prompting some hesitation on the investment side. Companies are negotiating with the Iraqi government on revised oil compensation, which has wreaked havoc on Iraq budgets and led to the delayed payments.

Although Iran and Iraq each have their own separate yet similar problems, a poll from the PRIX Index believe the pair will lead the way with increased exports in the near term.

Pressure Outside of “The Big Three”

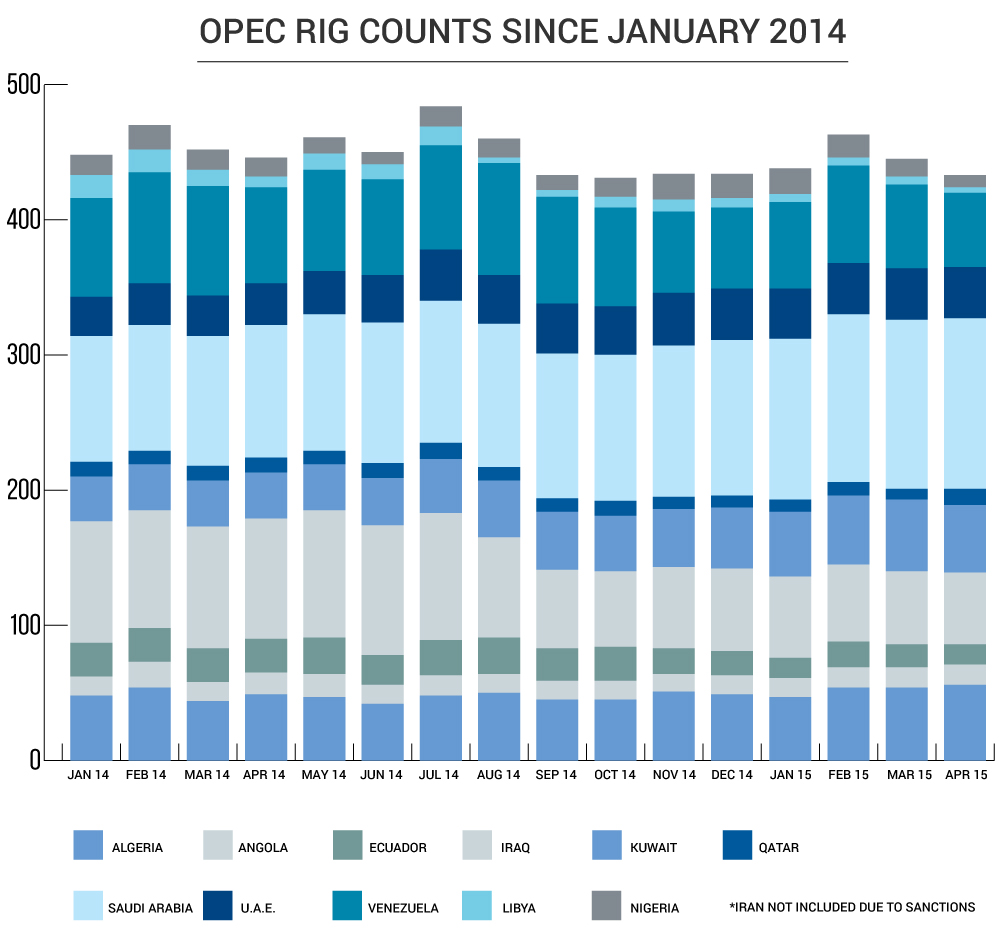

A note published by UBS Investment Research points out that output from Iraq, Kuwait and the United Arab Emirates reached 20-year highs in April. Rig counts have also been relatively steady, as evidenced by the chart below.

The change is a stark difference from operators in the United States and Canada, who are aided by much greater technological advances. Saudi Aramco’s marketing team is putting forth its best efforts to lure jobless American workers overseas to contribute their knowledge of unconventional development. United States rig counts have plummeted by more than 50% amid reduced capital budgets, as several E&Ps are simply trying to wait out the storm.

The UBS note sums it up, saying: “While OPEC again is facing continued oversupply, lower oil prices do appear to be having the intended effect of reducing investment by non-OPEC producers which we forecast will cut non-OPEC growth from 2.1 mb/d in 2014 to 1.3 mb/d in 2015E and 0.1 mb/d in 2016. Thus, we see no reason for the GCC members to shift their position and hence no change from OPEC.”

Frustration Abounds

Frustration from other members of OPEC falls on deaf ears because, frankly, countries like Ecuador, Nigeria and Venezuela are not holding any cards. All have called for an emergency meeting within the last several months, but the Gulf nations have been stone cold. They respond by reiterating their production levels.

Gaurev Sharma, a Forbes contributor with a history covering OPEC, said such countries can only affect the market with verbal darts. When Nigeria’s oil minister hinted at the possibility of a meeting and vaguely mentioned other countries were in agreement, the price of Brent inched up for the slightest moment. The fruitless comments were “straight out of the textbook that I’ve heard being read out umpteen times since I started covering OPEC seven years ago,” said Sharma.

Other more prominent OPEC members have played their cards more close to the vest. Ali Al-Omair, the oil minister of Kuwait, declared the cartel will be “more united” at the next meeting. “OPEC stuck together during a difficult test,” he said, adding that maintaining current production levels is “the best option.”

Libya recently echoed Kuwait’s sentiments, while an Iran spokesperson called a target change “unlikely.” In a 34-person survey conducted by Bloomberg last week, with the exception of one analyst, all who responded expect OPEC output to remain unchanged following next week’s meeting.

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.