Estimates Reserve Replacement of 247%

Operational execution was the primary takeaway from PDC Energy’s (ticker: PDCE) Q3’15 results, and the progressing development of the company’s Wattenberg assets carried over into its 2015 year-end reserves update. The news release, issued on January 20, 2016, reported proved reserves of 272.8 MMBOE and total 2015 production of 15.4 MMBOE, representing year-over-year increases of 9% and 65%, respectively.

Bart Brookman, President and Chief Executive Officer of PDC Energy, credited the improvements to both asset quality and PDCE efficiency in his prepared remarks. The company will host an Analyst Day in Denver, Colorado on April 7, 2016.

PDCE’s Wattenberg Position is Growing… and not Because of Acquisitions

Although overall production exceeded the top end of guidance, PDC actually increased its proved undeveloped acreage to 74%, compared to 70% at the end of 2014. The source of the extra undeveloped reserves comes from its successful Middle Wattenberg downspacing program, which PDC expects to double its well density to 16 wells per section.

Although overall production exceeded the top end of guidance, PDC actually increased its proved undeveloped acreage to 74%, compared to 70% at the end of 2014. The source of the extra undeveloped reserves comes from its successful Middle Wattenberg downspacing program, which PDC expects to double its well density to 16 wells per section.

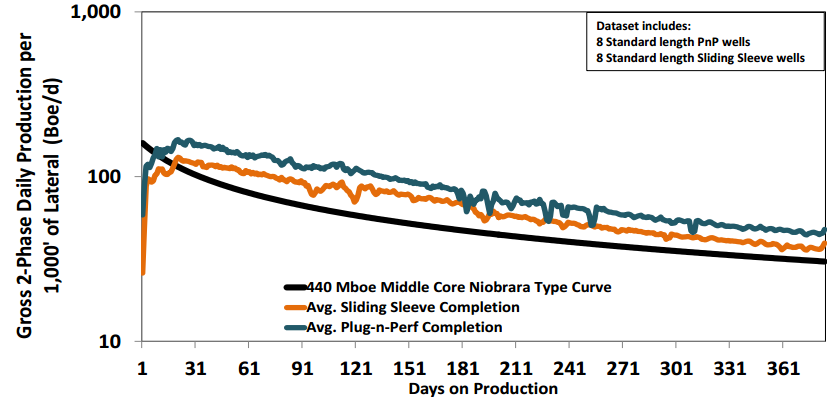

As PDC discovers additional drilling locations, its efficiencies are driving the prospect of even further growth. The company has realized improvements of 15% with its plug & perf completions compared to the sliding sleeve method. Management believes additional uplift of 5% to 10% is possible with the AccessFrac process – a method that will be tested throughout its 2016 program.

PDC listed 790 total gross proved undeveloped locations in the Wattenberg as part of its five-year plan.

But What about $30 Oil/$2.50 Gas?

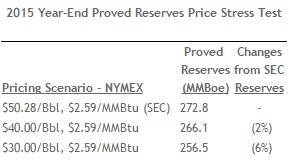

In its latest presentation, PDC believes its 96,000 net Wattenberg acres hold more than 2,600 proved and possible drilling locations. The 272 MMBOE is based on current SEC prices ($50.28/barrel and $2.59/MMcf) But these how much of its near-term drilling program is uneconomical in the current commodity market?

As it turns out, the vast majority is, in fact, viable in today’s environment. The details are on the right.

As it turns out, the vast majority is, in fact, viable in today’s environment. The details are on the right.

As noted, only 6% of PDC’s current reserves are proved uneconomical at $30 oil as compared to $50 oil.

What’s Planned for 2016?

“Our top priority for 2016 is maintaining our solid balance sheet and strong debt metrics,” said Brookman in the release. All things considered, PDC is in a very enviable position at the moment. In the coverage universe of Capital One Securities, PDCE is one of only two companies positioned for 2016 growth of at least 35% while maintaining a debt/EBITDA ratio of below 2.0x.

Its operational execution is also in the top percentile in EnerCom’s E&P Weekly Benchmarking Report. Based on in-house estimates at PDC, the company registered reserve replacement of 247%. In EnerCom’s database, the company has averaged three-year production replacement of 690% – well above the 90-company median of 348%, and its trailing twelve month capital efficiency of 284% is more than double the median of 107%.

For the time being, PDC is targeting cash flow neutrality in its 2016 budget of $450 to $500 million. Volumes are supported by a hedging program that covers 50% and 62% of oil and gas volumes, respectively, at approximately $85/barrel and $3.65/Mcf. The program held a mark-to-market value of $250 million as of November 30, 2015.

Perspectives on Valuation

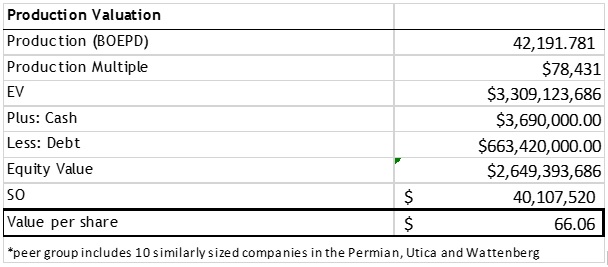

Based on a multiple of production valuation methodology, PDC shares could trade at roughly a 34% premium to its closing price on January 21, 2016, based on its updated production metrics.

Analyst firms believe production specifics may be altered, especially since PDC has flexibility on its rig contracts. The company is currently running four rigs in its Wattenberg region.

The company also provided some insight on the effects of new SEC reserve pricing, as its Nymex oil and gas prices fell by more than 40%. In a note to clients, David Tameron, Senior Analyst at Wells Fargo Securities, said the realizations from the new SEC pricing will be indicative of PDC’s peer results. “If anything, given PDCE’s asset base and the fact that it actually grew reserves (whereas many of its peers will be flat or down) means PDCE’s YoY change may be in better tier of results,” explains Tameron. “PDCE remains well positioned, has production and re-investment visibility, and remains inexpensive versus peers.”