Penn Virginia Corporation (ticker: PVA) is an independent oil and gas company engaged primarily in the development, exploration and production of oil and natural gas in various domestic onshore regions, including Texas, Oklahoma, Mississippi and Pennsylvania – however, the company expects its Eagle Ford (EF) operations to fuel its growth and transition to oil thru 2015.

PVA’s 2014 plans include running six rigs and the expected drilling of 98 gross (53 net) wells. Average initial production rates for its last 17 wells are 1,700 BOEPD, and PVA notes its growing knowledge of the play is boosting returns and lowering costs.

OAG360 notes that Penn Virginia’s strategic switch dates back to 2010, in which it began divesting natural gas assets to gain a foothold in the Eagle Ford. The Eagle Ford’s meteoric rise in popularity began at the same time PVA became involved in the play. According to the Texas Railroad Commission, 1,130 drilling permits were issued from 2008 to 2010. Since the beginning of 2011, more than 12,000 drilling permits have been issued. The production leap resulted in the Eagle Ford’s 2013 average production of 688 MBOPD, up from just 15 MBOPD in 2010.

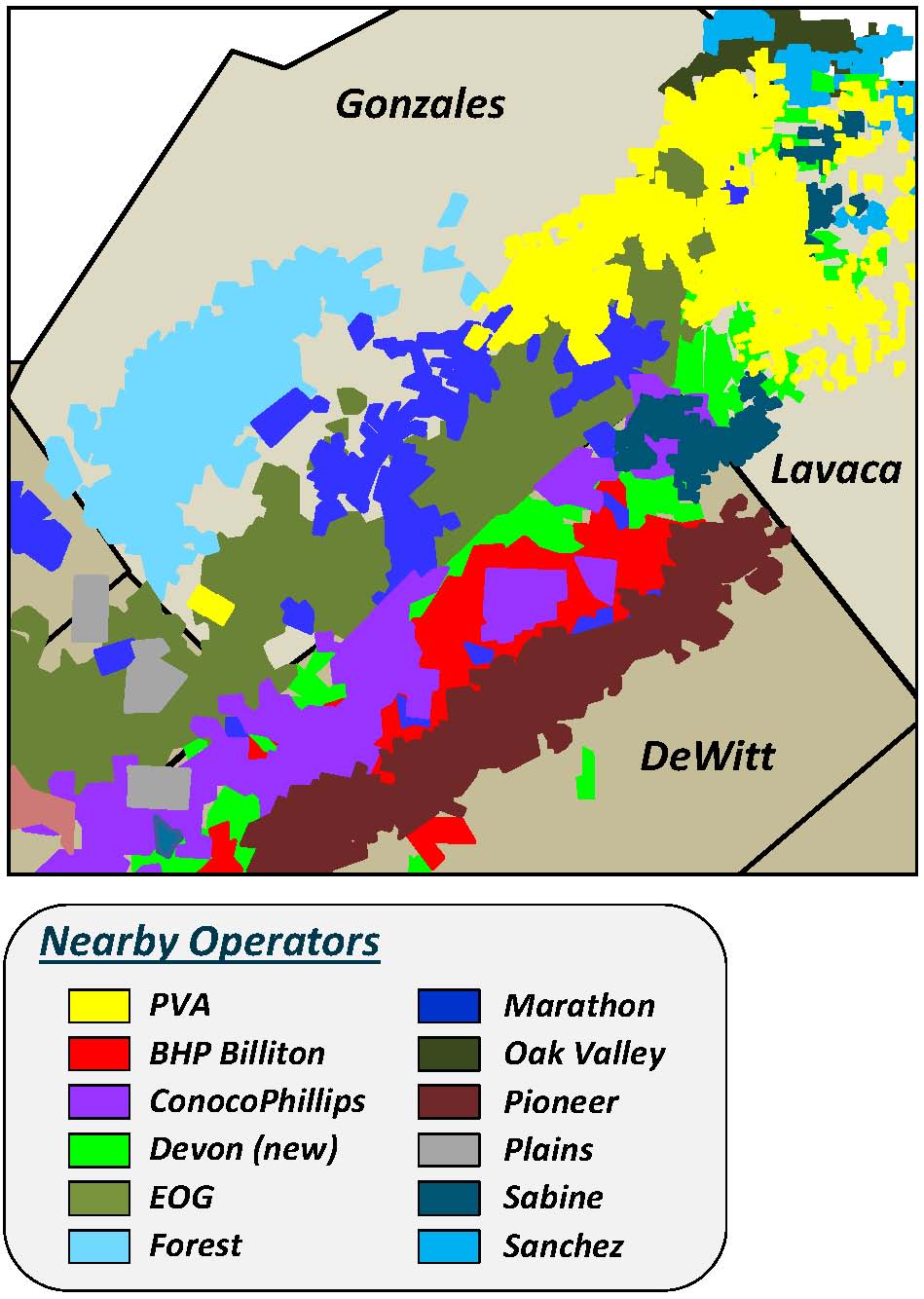

Success Shared by Neighboring Operators

PVA’s results are complemented by well-known E&P operators in the area. EOG Resources (ticker: EOG) holds acreage adjacent to PVA and recently reported five new wells produced a total of more than 13 MBOEPD. The wells averaged between 2,314 and 3,071 BOEPD (91% to 97% oil). According to Bloomberg, the wells were completed between March 13 and March 21 and the filings were lodged with the commission on March 27 and March 28.

EOG’s fields continue to increase in size and have boosted reserve estimates by 250% since 2010. Its increasing knowledge, effective downspacing and increased hydraulic fracturing are being realized on the balance sheet. When comparing 2013 to 2011, new techniques have increased initial production rates by 39% (2,077 BOEPD from 1,493 BOEPD) and decreased well costs by 24% ($5.5 million from $7.2 million). The company expects it can spend less than 12 drilling days per well moving forward. As evidenced by its footprint in the play, EOG has singled out the Eagle Ford along with the Bakken and Leonard Shales as the company’s three focus areas moving forward. The company plans on drilling 520 net Eagle Ford wells in 2014 alone, according to its March 2014 presentation. Roughly 1,200 have been drilled to date, with another 6,000 identified wells in its inventory.

EOG Production Makeup

Penn Virginia’s Eagle Ford Future

Penn Virginia currently holds 123,700 gross (84,300 net) acres in the play and operates 109,200 gross (77,800 net) acres. The company held 107,100 gross (67,000 net) acres in the EF and operated 93,800 gross (60,500 net) acres in its last update in November 2013.

Roughly 4,900 net acres have been added since February 2014 as the company continues to bolt-on acreage to its position just north of EOG’s territory. Approximately 32,000 net acres have been added since acquiring properties from Magnum Hunter Resources (ticker: MHR) in April 2013. PVA intends on compiling 100,000 net acres by year-end 2014, and its current operations have yielded an estimated 10 years worth of drilling inventory.

PVA’s Future

PVA said Eagle Ford pad drilling will result in somewhat lumpy growth but Q2’14 is expected to be the strongest quarter of the upcoming year. The exit rate for 2014 is expected to exceed 2013’s by 35% at its midpoint, which would amount to more than 25 MBOEPD. The company anticipates compounding growth by an additional 30% in 2015, despite capital expenditures expected to decrease in the same time period. PVA will follow the same trend through 2017 and is hopeful the company will become cash flow neutral by that time.

PVA continues to tack on more acreage through small acquisitions and joint venture projects. Despite rising industry interest in the play, PVA added more than 13,000 net acres since August 2013 at a price of roughly $2,800 per acre. Management has also expressed interest in exploiting the Upper Eagle Ford formation, and success in its testing would push its acreage above 100,000 net acres without the acquisition of any new assets. Regardless of the new testing, management said it will continue to add to its reserves by expending roughly $2,500 to $3,000 per acre.

A Catalyst to Keep an Eye On

Soros Fund Management LLC disclosed in March 2014 it had become PVA’s largest shareholder and that they would be exploring strategic alternatives. A recent Businessweek story reported Soros Fund Management LLC said options for increasing value could even include talking to possible acquirers. The stock has increased approximately 26% since the announcement.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.