High acreage costs beginning to affect economics in the Delaware

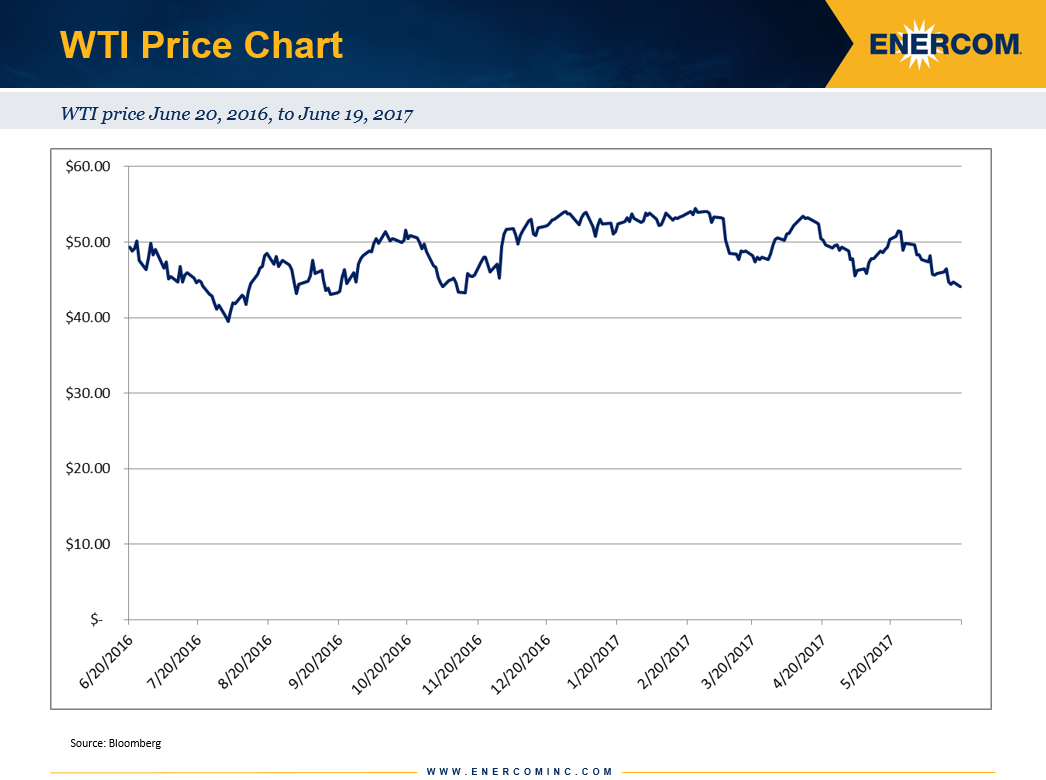

The Permian has enjoyed a rush of capital since oil prices began to recover from a low of $26.21 in February of last year.

The play is home to some of the best economics in the country, making it a prime target for E&P companies looking to maximize profit in a lower price environment. But the surge in land costs is leaving little room for new investors to profit.

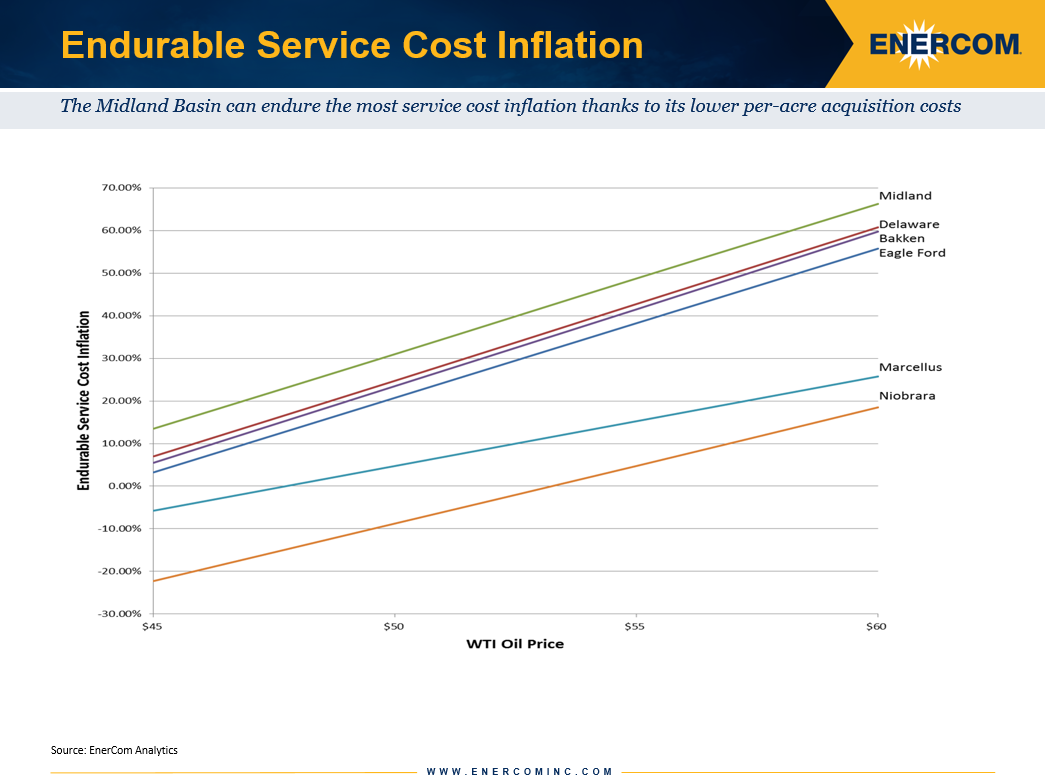

The Delaware basin, the Permian’s hottest zone, is beginning to become a victim of its own success. EnerCom Analytics’ well economic models indicate that the internal rates of return (IRRs) in the Delaware are now lower than those seen in the Midland due to the high cost of land.

At $45 WTI, EnerCom’s well economics models show IRRs in the Midland of 22.8% compared to 21.5% in the Delaware when acreage costs are included in the equation. The cost per-acre in the Delaware is 65% higher than in the Midland at an average of $33,000 per acre.

Economics in every basin are expected to see pressure as oil prices remain in the low- to mid-$40 range and oilfield service providers, who are in high demand for well completions and drilling, look to increase their prices. Combined with the high premiums in the Permian, this barrage of pressuring factors are making it more difficult for new investors to enter the play, and those with exposure are beginning to pull back.

Service costs are expected to increase between 10% and 15%, according to EnerCom Analytics, with some E&P companies saying they could increase as much as 20%. In EnerCom’s March Energy Industry Data & Trends, the firm found that most basins could absorb even the high-end of those estimates at $50 per barrel WTI, but with prices floating around $45 per barrel, it will be much more difficult for E&Ps to continue generating 20% IRRs or better.

Based on EnerCom’s models, only the Midland could handle more than a 10% increase in service costs at $45 per barrel with the high per-acreage cost of the Delaware pushing the play’s IRRs beneath the 20% IRR threshold.

Eight hedge funds have reduced the size of their positions in ten shale firms with exposure to the Permian by over $400 million, according to information from Reuters. The value of these funds’ positions in the 10 Permian companies declined by 14 percent, to $2.66 billion in the first quarter 2017 from $3.08 billion in the fourth quarter of 2016.

Less room to run

Investors continue to give Permian players a premium multiple compared to companies in other parts of the country, but some firms are beginning to worry operations in the region do not merit the higher valuations.

Concern about inflated land costs and weakness in oil prices has some firms worried Permian players may not fly much higher. The 10 companies examined by Reuters were down 18% already this year compared to a 13% decrease in the S&P 500 energy sector.

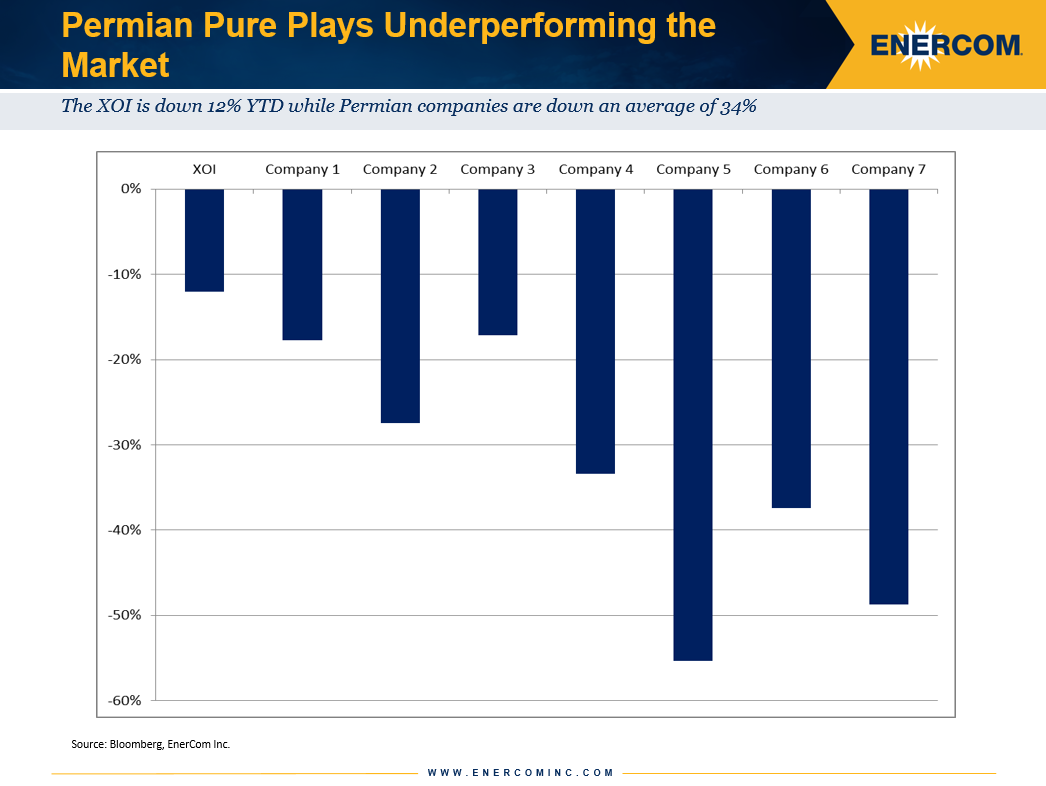

EnerCom’s analysis of a peer group of Permian pure-play companies found the companies were struggling more than the Reuters information indicated. Looking at the performance of seven Permian players compared to the XOI index, companies with operations in the region were underperforming the wider energy index in all cases.

The XOI is down 12% YTD while the seven Permian companies averaged a loss of 34% so far in 2017. WTI is down 15% over the same time period.

Well economics and returns from the Permian continue to be some of the strongest in the country, but companies in the play may see a near-term correction as investors weigh higher land costs and lower oil prices. Already this year, Permian companies are underperforming the wider energy markets and with an expected increase in service costs, it will become more difficult for companies in more expensive parts of the play to compete with other companies around the country for capital.