Range Resources Corporation (ticker: RRC) is a leading independent oil and natural gas producer with operations focused in Appalachia and the southwest region of the United States. The company has line-of-sight growth of 20% to 25% and was producing more than 1 Bcfe/d in its Q1’14 earnings release.

Range Resources completed an acreage swap with EQT Corp. (ticker: EQT) on June 16, 2014. EQT is an integrated energy company with an emphasis on natural gas production, gathering and transmission in the Appalachian area. Its subsidiary, EQT Midstream Partners (ticker: EQM), owns and operates approximately 2,500 miles of pipelines and gathering lines throughout the Appalachia. Per the agreement, first announced on April 30, 2014;

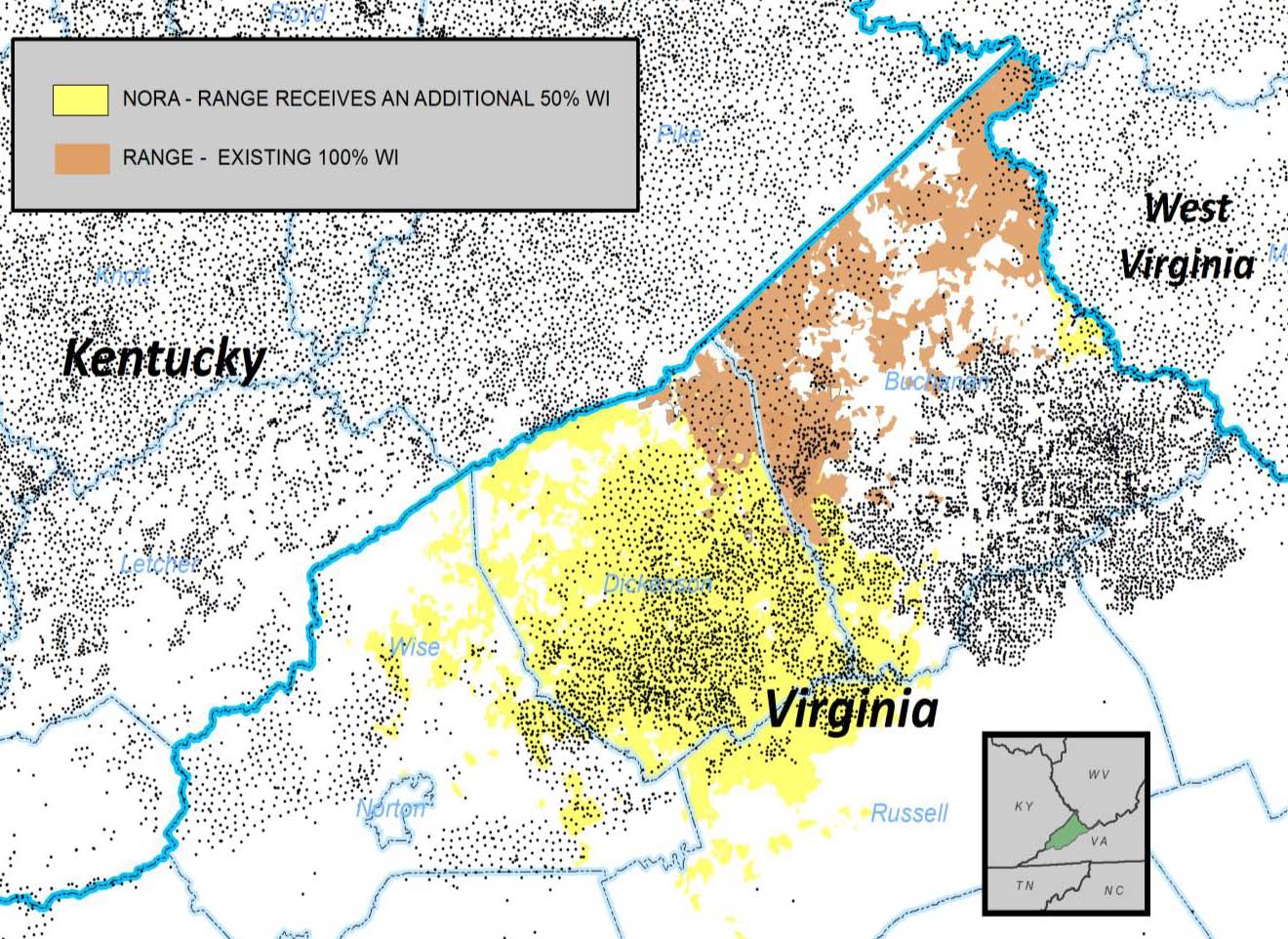

- RRC receives: EQT’s 50% stake in the Nora field of Virginia, giving RRC full operatorship of the area. The assets include 138,000 net acres along with 1,200 miles of gathering pipelines. Current production is 41 MMcf/d and has opportunities in coalbed methane, conventional tight gas intervals and the Devonian shale. Range also received $145 million in cash as part of the agreement.

- EQT receives: 73,000 net acres in the Permian basin, or all of RRC’s Conger properties. The acreage is located in Glasscock and Sterling Counties and is largely held by production. Production at the time of the agreement was 28 MMcfe/d (62% liquids) and consists of potential in the Wolfcamp, Cline and Wolfberry formations.

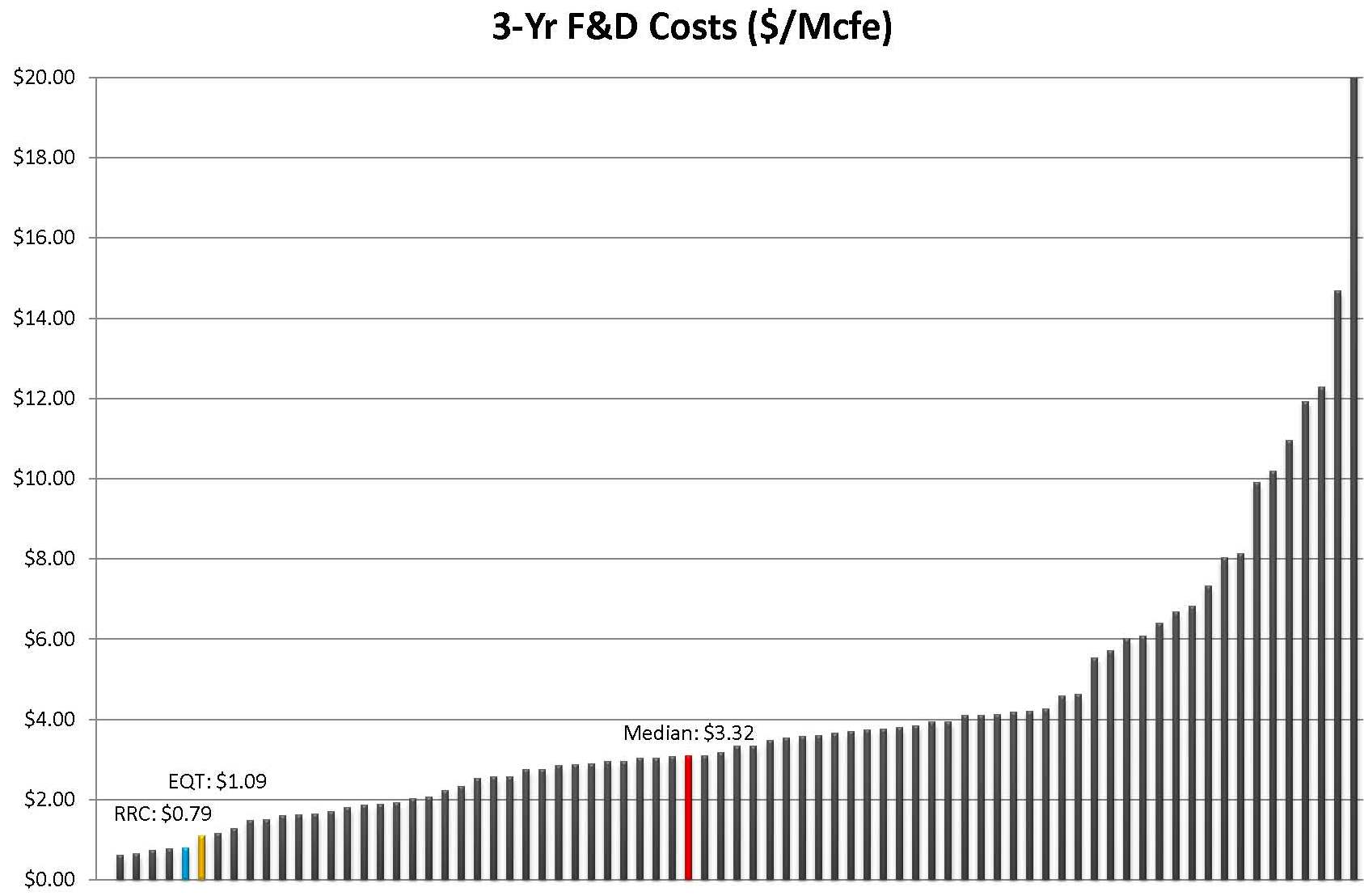

On a metrics scale, the new properties of RRC and EQT are producing 297 cf/d and 383 cfe/d per acre, respectively. The two companies have traditionally been among the lowest cost producers in EnerCom’s E&P database. RRC and EQT rank fifth and sixth, respectively, in terms of three-year finding and development costs per Mcfe. Range’s costs, in particular, are roughly one-fourth of the industry median of $3.32 per Mcfe.

At a conference on May 21, 2014, Rodney Waller, Senior Vice President of Range Resources, said: “We looked at the Nora combined, and we said we can grow better and faster by owning the Nora assets. With the beauty of the bid system, $145 million made sure we didn’t leave any money on the table. Now we have both working interests back together, which gives us a huge amount of integration and value to the half we already owned. So that’s really one of the keys of this trade.”

Range’s Updated Playing Field

Pro forma for the acquisition, Range Resources’ production from Virginia increased to 111 MMcf/d from 70 MMcf/d (59% increase) and its acreage rose to 385,000 gross and net acres from 247,000 net acres (56% increase). The company also has full ownership of 1,530 miles of gathering pipelines and 83,000 horsepower of compression. Range defined the properties as “significantly underdeveloped compared to surrounding fields.

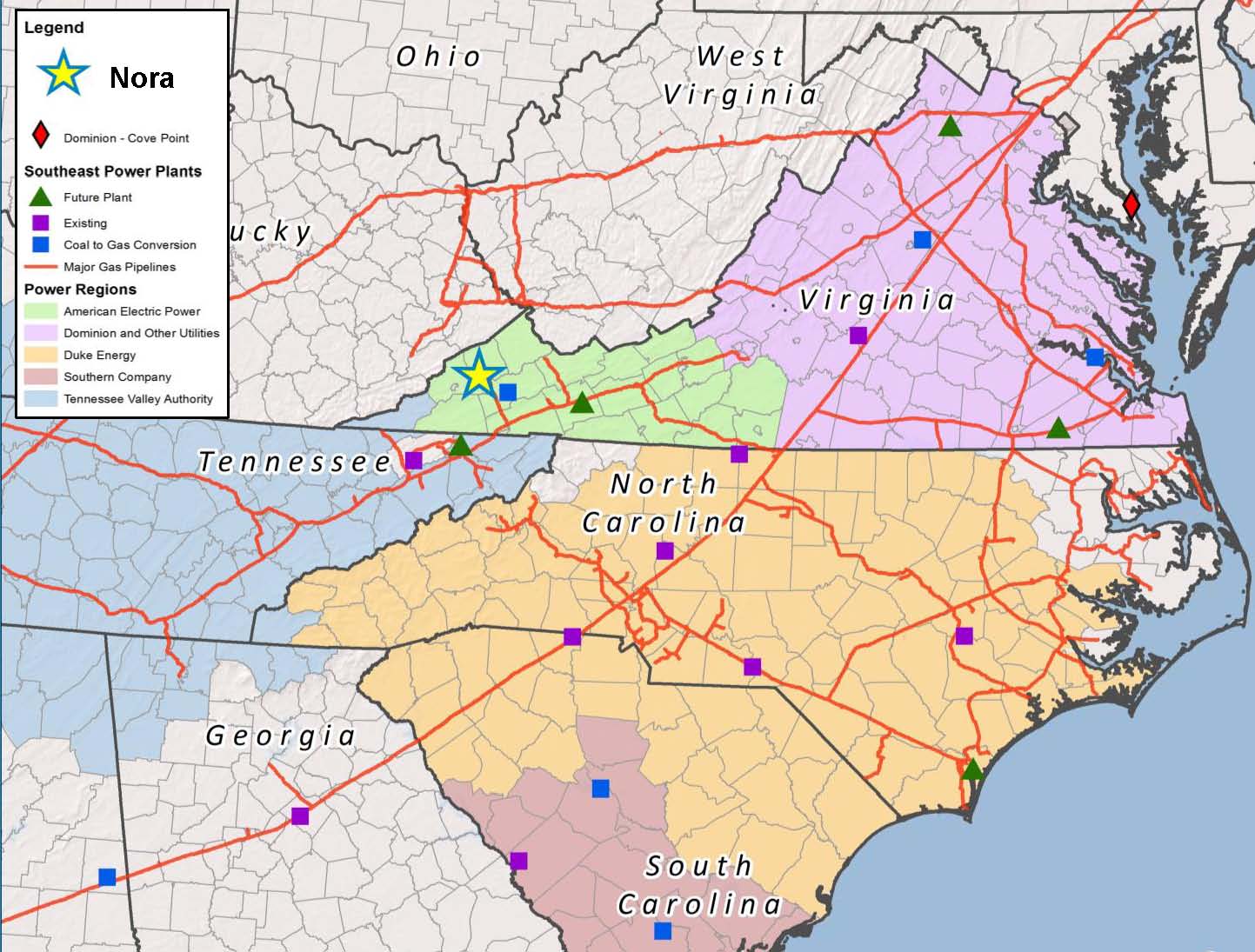

Total resource potential from the new properties is 2.0 Tcfe and total resource potential in Virginia is 5.2 Tcfe, according to Range’s presentation on April 30, 2014. The company believes natural gas demand in the southeast United States is expected to increase by 3 Bcf/d in the next five years. The presentation also said opportunities deeper than 6,000 feet are untested and existing wells hold upside potential.

“More than Cash”

At the conference, Waller was asked why RRC didn’t opt to sell the Conger assets as opposed to the acreage swap. Waller explained the company’s previous arrangement of a 50% working interest was slowing operations because both parties needed to coordinate to engage in operations. Now that Range has full operating interest, the company can increase its stake in the growing energy market in the eastern United States at its own pace.

“This actually gives us a lot more than cash,” said Waller. “It gives us a growth opportunity and enhanced some existing assets to a much higher state.”

Prepping for Exports?

Waller said once international buyers enter the picture, the oversupply of natural gas in the United States will quickly switch to an undersupply on a worldwide level. He said: “What you’re going to see is a lot of people scrambling to make sure they’ve got all their gas sourced before the exports begin. What you’re also going to see, in my opinion, is that when you move to 2016 and 2017, we’ll no longer talk about firm transportations being paid for by the E&P companies. What you’re going to do is you’re going to see it revert back to where I started in the business 30-something years ago, you get it to a pipeline, they’ll take it.”

Range previously divulged details on its low cost structure and marketing arrangements which allows plenty of breathing room for profit. Transport costs are as low as $0.25 per MMBtu and management projects dropping the price to $0.21 per MMBtu by 2016. Management said interest in natural gas from Virginia and the Carolinas factored into its decision to acquire the remaining assets in Nora, and the existing infrastructure allows it to supply the markets at one-third of the transportation costs.

“The real key to this business is to have diversification, optionality, and have a market,” said Waller. “Because of where we’re situated in the Southwest, we have so much diversification and optionality to be able to go multiple directions.”

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.