Projected Average Annual Capex from 2017-19 will be 33% Below Capex from 2013-14

Margins are as important as ever in the new commodity environment, and Total S.A. (ticker: TOT) is setting some high benchmarks to reduce costs as much as possible.

In a corporate strategy and outlook presentation on September 23, 2015, the France-based exploration and production company increased its capex reduction targets while maintaining an asset sale program that is expected to deliver $10 billion in sales by 2017. For the same time frame, TOT increased its operating expenses reduction initiatives by 50% ($3 billion from $2 billion) while dialing back its capital expenditures by $2 billion per year. Capex from 2017 through 2019 will be in the $17 to $19 billion range – down nearly one-third from 2013’s mark of $28 billion.

Part of the Reasoning: 20 New Startups

Total invested heavily in new projects in recent years, and the reduced capital intensity is one of the reasons the company has slated a lower budget for the remainder of the decade.

Production volume, meanwhile, is expected to grow by 5% annually from 2014 through 2019. Russia is a major piece of Total’s plans: management expects the country to be its most important region for development by 2020, with targeted volumes of 0.4 MMBOEPD. In March, Patrick Pouyanne, President and Chief Executive Officer of Total, said he expected oil prices to remain depressed in 2015 but stressed the silver lining of the situation. “For me, I see this period as an opportunity to clean up the cost base of our company,” he said.

Divestments Underway

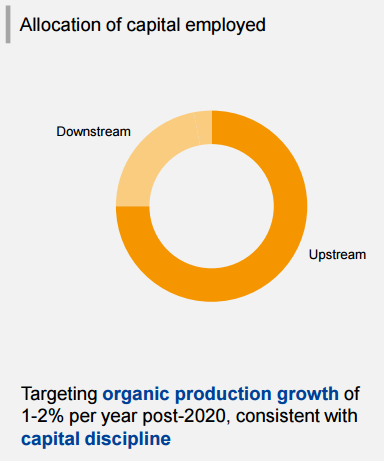

Total sold about $1.3 billion in assets earlier this month in two separate deals, divesting service stations and midstream assets in Europe. The company sold a 17% interest in a Germany refinery for $300 million in June. Approximately 75% of its capital will be employed on upstream projects related to its updated guidance. The company plans on divesting an additional $5 billion through 2017, amounting to $10 billion total for the three-year time period.

Sees No Reason to Touch the Dividend

The main goal of the capex reductions is to fully protect the dividend. At the event, Total management said its dividend can be covered by free cash flow through 2017, based on prices of $60/barrel. Any upward fluctuations in oil prices will be viewed as a bonus to the balance sheet.

“From 2017, we’ll benefit from stronger cash flows for two reasons: higher production and because we exit on the intensive CapEx five-year,” said Pouyanne. “We have flexibility there, so there is no reason why we should touch this dividend.”