Rystad Energy

Oil & Gas 360 Publishers Note: Rystad is a great resource for world energy information. There are some great nuggets in this article. However, in this conclusion I do not agree. Check out our live daily show: Energy News Beat

As the 2020 presidential election in the US is approaching, Rystad Energy has looked at how the country’s oil industry has performed under different presidents and evaluated the plans of this year’s candidates, shedding light on what the US oil industry may have in store in the next four years.

Technological innovations, aided in part by record high oil prices in the first part of the past decade, unleashed a new unconventional sector that catapulted the US to the league of top oil producers worldwide, dramatically changing the global supply landscape. Ample supplies have helped keep US pump prices low, maintaining macroeconomic stability with benign inflation despite supply disruptions amid geopolitical upheavals in the Middle East, North Africa and Latin America.

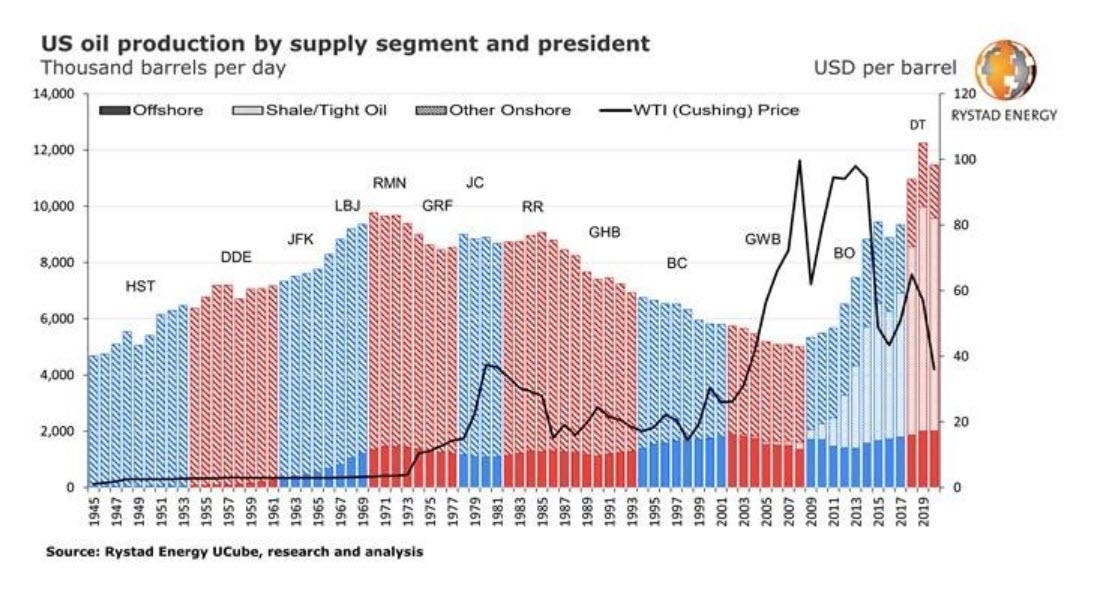

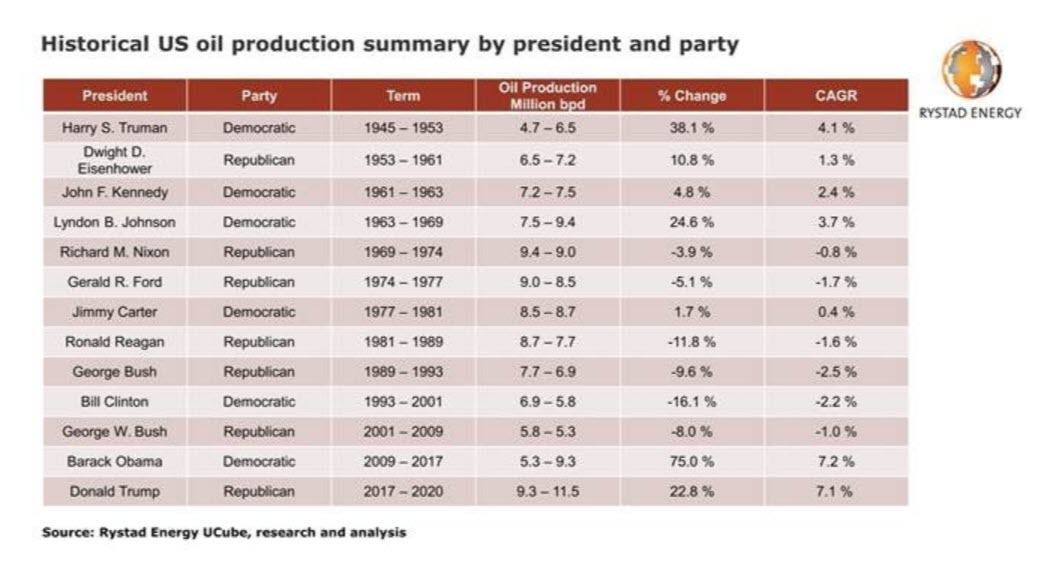

Since World War II, US oil production has increased on average 2.6 % per year under Democrat presidents and stayed almost flat with average annual growth of only 0.1 % under Republican presidents. The turnaround for the US oil industry came as George W. Bush exited Washington in 2009. Boosted by thriving new production from shale and tight oil in response to advances in drilling technologies, production sky-rocketed through 2017 under Barack Obama’s leadership.

The 7.2% CAGR over this period is the highest in US history for a single president, despite the oil market downturn in 2015 and 2016. It is in contrast with the broader opinion that Obama was generally more sympathetic towards the environment than his predecessor and successor.

Production continued to increase after Donald Trump entered the White House in 2017 with a CAGR of 7.1%, even though the market has experienced another downturn. The US became a net crude oil and total product exporter in late 2018 for the first time since the 1950s, and net imports/exports have hovered around zero ever since.

Under Donald Trump

Since taking office, and following on from his 2016 campaign pledges, President Trump has enforced various energy and environmental sector policies. Just four days after being sworn in on 24 January 2017, the president signed executive orders to allow construction work to begin on the divisive Dakota Access and Keystone XL oil pipelines.

These proposals were previously vetoed by President Obama, partly due to environmental concerns in Nebraska. If built, Keystone XL would provide the US with improved access to supplies from Canada and transport links from North Dakota, Montana and Oklahoma to Gulf Coast refineries, in addition to generating jobs, additional tax revenue and investment from the industry.

On 4 August 2017, barely six months after Trump’s inauguration, the administration submitted a formal request to withdraw the United States from the Paris Agreement, a United Nations-led accord to address and combat climate change. Although the withdrawal is not formalized until three years after the agreement came into effect, on 4 November 2020 (a day after the election), this action makes the US stand out as the only country out of 197 to reject the agreement.

The government reduced the federal corporate income tax rate from 35% to 21% (reducing the combined rate from 38.9% to 25.7%) when the 2017 Tax Cuts and Jobs Act (TCJA) was passed by Congress and signed by Trump in December 2017.

This cut in the marginal tax rate has improved the liquidity of oil and gas producers, reducing breakeven prices. Taking ExxonMobil’s US operations as a specific example, we estimate that in 2018 the company saved $193 million (36%) in corporate tax, reducing asset breakeven oil prices by as much as 5.3%.

The true impact of the changes varies from company to company, but in a sample of 50 operators our study estimates that operating cash flows for all companies could increase by more than $5 billion per year (with an average of about $250 million to $300 million per year in tax benefits) due to the TCJA.

The TCJA also incorporated provisions to establish an oil and gas program in the Arctic National Wildlife Reserve (ANWR) in Alaska. This legislation concerns the 1.57 million-acre Coastal Plain area, where directives to establish and administer a competitive program for leasing and development of oil and gas assets were signed into law.

The Biden plan

In terms of environmental issues, Democratic candidate Joe Biden’s ultimate goal is to make the United States carbon-zero by 2035. Widely considered to be more understanding of the fossil fuel industry’s impact on climate than his adversary, Biden in July announced a $2 trillion investment plan, spread over four years, to counter climate change.

The plan covers reforms in infrastructure, transit, the automobile industry and the power sector, and the former Vice President claims it will create millions of new jobs along the way. Biden vowed in a public address on climate change on 15 July that, if elected, he would re-enter the US into the Paris Agreement, also stating a desire to “reverse Trump’s rollbacks of 100 public health and environmental rules”.

The Biden plan has championed the Green New Deal as an essential component in the fight against climate change and underlines the ‘banning of new oil and gas permitting on public lands and waters’.

The state likely to lose the most from this plan is New Mexico, which houses some of the Permian Basin’s Delaware region and gets 65% of its production from federal acreage. Other potentially affected states are Wyoming and Colorado, with the Powder River Basin and DJ Basin, which get 37% and 11% respectively of their production from federal acreage. North Dakota, where part of the Bakken shale formation is located, generates 16% of state production from federal land.

Even so, we do not expect a potential federal land fracking ban would have any immediate impact on nationwide Lower 48 output (excluding the Gulf of Mexico). That’s because activity would migrate from federal acreage to equally commercial state and private lands. However, the industry landscape has changed dramatically this year – and with reduced production and lower prices, ¬the assumed impact may have a different gravity than previously thought.

We see clear evidence that a significant number of US onshore operators with a presence in low-cost federal acreage, particularly in New Mexico’s Delaware basin, are factoring in the uncertainty associated with future oil and gas activity on federal lands in their operational plans. Many are now fast-tracking the permitting process on federal land to ensure that significant inventory will already be approved if an activity ban on federal acreage is implemented in the future.

The basin-wide share of federal land in total new drill permitting activity has been in the 73%–87% range since the fourth quarter of last year, in contrast to staying around 60% in 2017‒2018 in Eddy and Lea counties. Among the eight largest operators, six companies show more than 80% contribution from federal acreage to their total approved new drill permits in 2020. In the case of Devon, Occidental and ExxonMobil, the share of federal acreage had already risen in the 2017–2019 period. EOG, Marathon and Matador really accelerated their permitting process on federal land in 2020.

A potential fracking ban on federal acreage would hardly have any impact on nationwide oil and gas output in the medium term, given the already existing depth of low-cost inventory and activity migration. This outlook may actually increase the likelihood of a fracking ban being implemented should Biden become the next president and pursue his campaign pledge, as there would be no major damage to the US oil and gas industry from a macro perspective.

Nevertheless, more new restrictions on federal land are not impossible. Restrictions on federal land leasing would also affect Alaska and the Gulf of Mexico and operators invested in these regions. The details on the extent of any potential ban are limited at present but we have modeled scenarios of increasing severity.

We currently estimate that there are 42.4 billion barrels of economically recoverable oil in Alaska and the Gulf of Mexico, of which 6.4 billion barrels are held in producing fields as proven developed producing (PDP) reserves. If there were to be a ban on all new leases, as proposed in the Biden plan, then the industry would effectively lose 16.2 billion barrels of oil. Stricter regulations including a ban on exploration would remove a further 6.1 billion barrels from licensed fields, while a complete ban on all drilling would remove another 13.7 billion barrels. Although realistically not tenable, the heaviest restriction of all would be to ban all production, which would leave the remaining 6.4 billion barrels under the ground, too.

“The more restrictive measures related to oil and gas activity on federal land will have a more pronounced impact on activity offshore and in Alaska. Ironically, a ban on new exploration or lease rounds on federal land might result in increased interest in US onshore development, as many operators with a presence in the Gulf of Mexico, primarily the supermajors, also hold significant onshore positions,“ says Artem Abramov, Rystad Energy’s Head of Shale Research.

Total ban on fracking?

Although no commitment has been made to ban all hydraulic fracturing activity, as promoted by Senator Bernie Sanders and other candidates in the primaries, such a scenario would destroy US shale entirely, and the destruction process would be quick and painful. With no new wells being put on production, hypothetically from 2021, only wells that are already producing would contribute to output.

US light oil production from horizontal wells peaked at 8.5 million bpd in March and is expected to decline to between 7.0 million and 7.2 million bpd by the end of the year due to a collapse in activity in the second quarter, factoring in the reactivation of curtailments in the third quarter. However, if no new wells are put on production from January 2021, this year will mark the beginning of a swift phase of decline, with US light oil output likely falling to less than 3 million bpd by the end of 2023.

Shale gas and associated gas output from light oil reservoirs would experience a less steep but still severe decline, from 78 billion cubic feet per day (Bcfd) in December 2020 to 40 Bcfd in December 2023, without any new completions.

A theoretical fracking ban in the whole country, if implemented, would result in rekindled interest in conventional enhanced oil recovery (EOR) projects. With key purely conventional companies such as Denbury, California Resources Corporation and Sheridan going through severe financial challenges and debt restructuring, it would take a long time for conventional activity to pick up speed again. In any scenario, we do not anticipate increased US onshore conventional activity to deliver sufficient incremental volumes to offset light oil’s base decline.

Statistics from the Bureau of Labor show that the E&P industry employed 157,000 people as of February this year, with another 315,000 in the oilfield services sector. Around 60% of the total are estimated to be employed in the onshore unconventional business. Employment numbers had already fallen significantly due to declines in the oil market as shale operators scaled back 42% of their workforce following the 2016 downturn.

An outright fracking ban would result in a considerable portion of the current workforce being made redundant. We believe the labor data from the bureau does not accurately reflect the total workforce in all business segments directly related to the oil and gas industry.

The actual number of employees in various industry segments – exploration and production, service providers, suppliers, manufacturers, midstream and downstream companies and advisors – is close to 1.5 million. This represents almost 1% of the total US workforce of 158 million, and any restrictions on the oil and gas industry would have a significant impact a large portion of the US workforce.

Conclusion

If Joe Biden becomes the next US president, there are clear expectations of an increased focus on the environmental aspects of US oil and gas operations. While some additional environmental policies might challenge the US producers’ economics, it is quite possible that Biden’s policies will be beneficial for them – at least in the short term.

A potential end to the ongoing trade war with China would surely help support demand and oil prices. Similarly, an increase in measures to prevent the spread of Covid-19 would benefit oil prices in 2021–2022 in our view. A potential fracking ban on federal land, as discussed above, would also most likely have a positive impact on oil prices in the short term.

Taking all these factors into consideration, it seems entirely plausible that the US oil and gas industry could benefit from a Biden presidency during the first quarters of his term amid a recovery in oil prices.