An exclusive Oil & Gas 360® interview with WPX Energy VP of Midstream and Marketing Greg Horne, as WPX and Howard Energy Partners step on the accelerator

In the early days of summer, WPX Energy (ticker: WPX) and privately held Texas midstream company Howard Energy Partners announced that the two companies had agreed to form a joint venture to develop midstream capacity in the Delaware basin.

In its recent Q3 earnings announcement, WPX announced that the two partners had closed the deal during Q3 and that operations were well underway.

The idea behind an E&P getting into the infrastructure business in its operational area is not a new concept. It allows companies to ensure takeaway capacity in a rapidly developing play. But beyond the functionality of moving WPX’s hydrocarbons to market, WPX VP of Midstream and Marketing Greg Horne talked to Oil & Gas 360® about the strategic value of this infrastructure JV and multiple avenues for upside opportunity that it delivers to WPX.

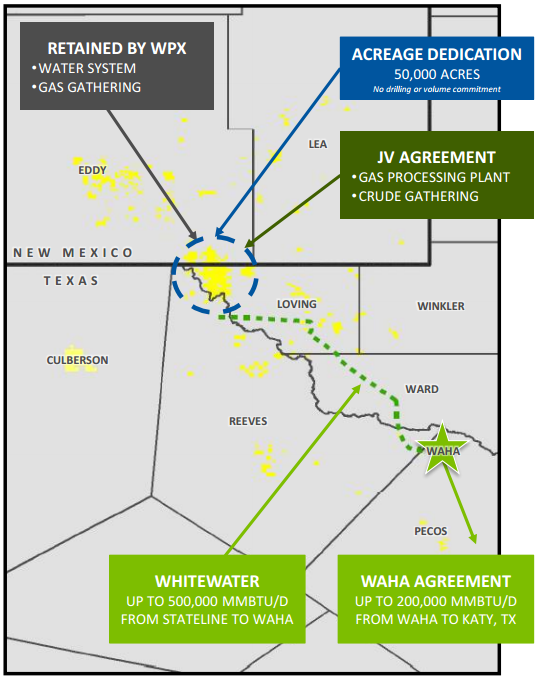

WPX said that the venture will support WPX’s operations in the Stateline area on the border of New Mexico and Texas. In total, the agreement will cover about 50,000 acres, or 37% of WPX’s total Delaware basin acreage.

Howard Energy Partners will construct and operate the JV assets. Howard paid WPX $300 million upfront. In the announcement, WPX said that Howard will also fund the first $263 million of JV capital expenditures, including a $132 million carry for WPX. WPX reports the transaction implies a value of $863 million for its Stateline oil and gas gathering and processing business. WPX reported in its Q3 presentation that it had received $349 million from Howard.

Makings of the deal

To dig further into the deal, uncover the WPX strategy that led to the JV and learn more about the midstream assets and operations, and the potential upside avenues for WPX, Oil & Gas 360® spoke with WPX’s VP of Midstream and Marketing Greg Horne.

Horne has worked at WPX since 2001, coming into the company through Williams. Prior to Williams, Horne was at Koch Industries for 10 years, coming fresh out of the University of Oklahoma, where Horne said he “got an aerospace engineering degree and never really worked in the aerospace business.”

Horne said he mostly worked on David Koch’s chemical technology side of the business. “When a number of Koch folks headed off in the late ’90s to Williams to start up their energy, marketing, and trading operation, I took a role there and proceeded to work on the marketing and trading floor for a number of years.

“I spent a lot of time running around the world chasing global gas ideas—LNG, CNG, all kinds of waterborne natural gas shipping,” Horne told Oil & Gas 360®. “We had quite a bit of gas in the Piceance, and I managed a number of our transportation assets.

“The marketing and trading group was included in the WPX spin-off in 2012 and I came over with WPX and have continued in the marketing group. I’ve been involved on the midstream side of our business since 2014 and was recently promoted to vice president of midstream and marketing for all oil and natural gas.”

[EDITOR’S NOTE: Williams Cos. Inc. announced in 2011 that it would split off its E&P business into WPX Energy Inc., a standalone company]

The Oil & Gas 360® interview with Greg Horne appears below.

OAG 360: How would you generally characterize the takeaway situation in the Permian basin right now?

WPX Energy VP of Midstream and Marketing GREG HORNE: In general, I would say it’s starting to show the early signs of getting stressed. Natural gas prices, if you’ve spent any time looking at Waha, let’s say over the last 12 to 18 months, prices have come under significant pressure. 2018 and 2019 prices at Waha are really moving south. We’re now getting into the 50, 65 cent range. So, it’s showing the signs of what we anticipated when we first got into this basin.

I think that’s why a marketing and trading background is so important at WPX. We take a little bit different view than a some folks in our space, having been part of a big transportation portfolio where we had successes and failures. For example, in the Piceance, quite frankly, our expansive transport portfolio kind of burned us. However, our successes included past endeavors developing transportation portfolios as well as key relationships in the constrained basins of the Barnett and Marcellus which yielded significant value for the upstream assets.

[EDITOR’S NOTE: WPX made a transformative purchase of RKI Exploration and Production in August 2015, launching the company into the Permian basin]

When WPX entered the Permian via the RKI acquisition in 2015, we immediately developed a fundamental viewpoint and saw the natural gas market in the Permian becoming tight in the not too distant future. Mexico demand is just not there yet. Actually, the infrastructure in a number of areas is not even hooked up south of the border and the general consensus is that demand is going to be slower to show up.

While there is physical pipe capacity away from Waha right now, there just isn’t demand taking it away. As producers continue to produce in this $50/bbl price environment, we’re seeing that pressure and a potential glut of supply starting to build in the Permian. On the oil side, we expected that the Delaware would experience some takeaway constraints and as a result, we anchored the Oryx II pipeline and negotiated equity in the deal.

On the NGL side, if we think about the three commodities – gas being the most distressed in the coming years; oil, second; and then NGL is probably third.

There are a number of pipelines out there which can be easily expanded, but there are a couple of new entrants coming into the basin, which we’ll be involved with in terms of takeaway from our Howard JV plants. We’re excited about the competition in the Delaware when it comes to NGL transport space and resulting favorable rates and deal terms. I feel pretty good about the other two commodities for our portfolio. But that’s not to say that some folks won’t experience some pain.

OAG360: If natural gas going into Waha is going to be restrained in the near future. Do you think that this rush of capital to develop the Permian basin is going to create any new points in the market? Maybe the way to say it is, ‘What’s the next Waha’?

GREG HORNE: Well, because of the way Texas works, it’s uniquely positioned in that you can build pipelines in Texas, an intrastate pipeline, and get it done inside 18 months.

Whereas, when you consider other states and a need to get beyond a constraint point like a Waha, take New Mexico, for example – somebody’s going to have to anchor an interstate project, which requires a FERC 7 (c) certificate and takes about three years from start to finish. It’s not an easy task.

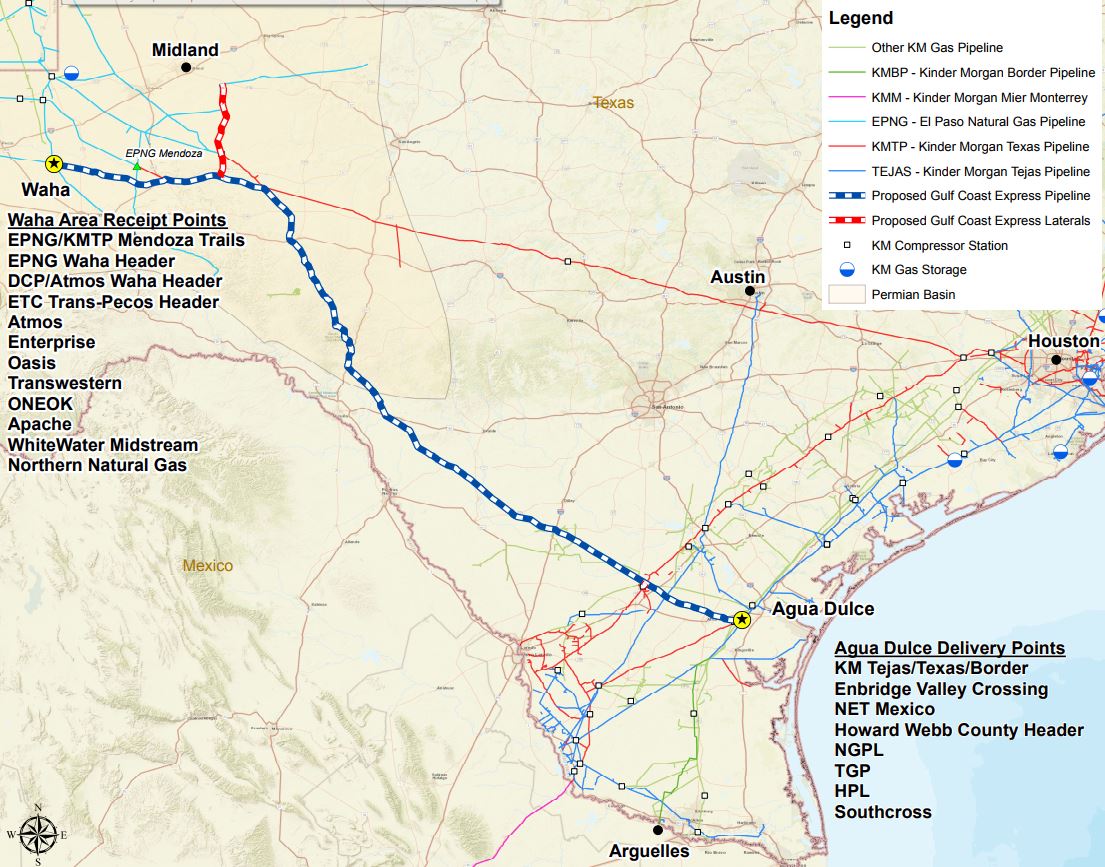

Expanding gas takeaway beyond Mexican exports from Waha will likely consist of two markets. We see the Houston Ship Channel and Agua Dulce as the most likely candidates for developing incremental capacity. The new petrochemical projects and demand that will becoming on over the next two to six years will likely favor options that consider the Houston Ship Channel and Corpus Christi as delivery points.

OAG360: Is there infrastructure to take the gas to those markets, or will that need to be built?

GREG HORNE: There is infrastructure today, but in a year to 18 months it’s likely going to be full. Kinder Morgan recently announced a pipeline with Targa. There are other competing projects, but none have yet to be sanctioned.

We would expect that the spreads between Waha and Houston will have to grow beyond where they are currently trading for producers to justify taking out 10 to 15 year contracts.

So it’ll be interesting to see what happens. You have a number of smaller and mid-cap type companies out in the Delaware and the Permian and it seems there isn’t currently much appetite to step up and anchor these pipelines move gas away from Waha.

OAG360: Are you guys looking at new downstream markets as potential upside for this JV in terms of building new infrastructure? If Waha is going to be constrained, will the JV look at building any pipelines in new markets, or in markets that are underserved?

GREG HORNE: Well, again, we’ve got 200-million a day of takeaway out of Waha and we’ve been pretty out in front on hedging Waha as well. So we feel pretty good about our strategy. Ultimately, you do have to have a mix of transportation assets physically away from constraints and then also a hedging strategy. We’ve got both of those in play.

But, depending on how things go, I think over the next year to 18 months we’ll continue to evaluate options of taking out bits and pieces of transportation to add to our 200 million a day that gets away from Waha.

OAG 360: What was the primary impetus behind WPX making the midstream JV move in the Permian?

GREG HORNE: As I look back to when we did the RKI transaction, we really started planning from day one. Rick Muncrief [WPX chairman and CEO] raised the issue and wanted us to lay out a plan. We responded with a strategy that envisions a future midstream JV transaction as well as developing outlets and potential ownership in downstream assets around crude, gas, and NGLs.

We considered inclusion of our water gathering and our gas gathering and our water disposal assets, but sometimes when transactions get too big, it limits the pool of buyers. But by holding these assets back, we’ve kept a number of options available.

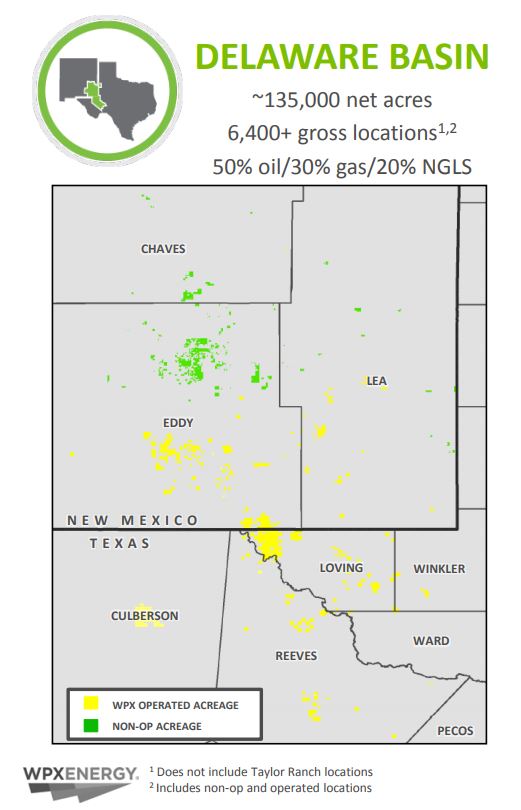

One of the main value components that we considered in the RKI deal was the infrastructure that RKI had out there in the Delaware Basin.

In a roughly 50,000 acre contiguous position which we call State Line, straddling the New Mexico/Texas border, we were seeing other midstream deals with significant transaction values which allowed us to extrapolate a $500 million marker for our newly acquired midstream assets. We arrived at that valuation based solely on the water-gathering and disposal infrastructure and the gas-gathering infrastructure that RKI had in existence and based on the flows at the time.

We didn’t get a lot of pushback in the market from that self-ascribed valuation. As a matter of fact, what happened after the transaction closed was an incredible level of interest and folks knocking on our door left and right. We had inbound calls from strategics to private equity to infrastructure funds that wanted to partner with us, unsolicited offers to come in and buy out our infrastructure.

In terms of making a move in the Permian on the midstream side, it was always part of the original plan that we knew at one point in time we had something we could monetize. But the fact that we had just picked up the acreage and we were in a delineation mode, we wanted to be intentional about developing the asset first.

Right after the transaction occurred, crude prices went below $30. We went from five rigs with RKI down to two. And of course, now in the Permian, we’re back up – at some point in time this year, we’ve run seven to eight rigs out there.

When you think about the point in time around the transaction, the downturn certainly led to a prudent pause in the development. Even in the downturn with crude oil prices below $30/bbl, we still had plenty of people interested in our midstream infrastructure.

As we came out of the downcycle and re-started our development plan, we were asking ourselves: What is the best window of opportunity to do something here in the midstream space?

Around mid ’16, we came together as a management team and began to talk about plans for ’17, including the expectation around increasing rigs and constrained processing capacity . We have a number of contracts that were starting to roll off, so we thought this was an opportune time as we ended 2016 to really start a process and basically respond to the significant market interest in midstream assets.

We went into that process with significant interest from day one. Barclays did an incredible job of managing that process for us which resulted in a great transaction. And when you consider our original $500 million marker assumed in the RKI deal, the WPX-Howard transaction valuation didn’t include the water-gathering disposal and the gas gathering, which points to future upside for WPX’s midstream valuation as throughput grows in the assets.

The JV assets included crude oil gathering and a future cryogenic processing complex. We started building the crude oil gathering at WPX and those assets were about 30% complete as we began the process of finding a JV partner; it’s now about 60% complete. So, Howard will finish it off as the operator sometime in the next six months. And then we’ll have most of our pad development hooked up to the crude gathering system.

Regarding the gas-processing facility, we only had a purchase order in place for a 60 MMcf/d plant that the JV quickly exchanged for a 200 MMcf/d plant, a section set aside where we acquired surface, but there were no significant assets there at the time of the JV transaction. So, when you think about the transaction, very little pipe in the ground and a large processing complex that was yet to be built, it was imperative for WPX to pick a partner who could execute and had previous experience around similar assets.

Holding back the water assets and the infield gas-gathering assets was intentional and it could allow us to consider monetization opportunities in the future.

OAG360: Looking at the JV assets, what are the included assets?

GREG HORNE: It is infield crude oil gathering that stretches up into New Mexico, consisting of a large north-south trunkline, and then a number of east-west lines that go out and connect up to various pad developments.

We have three different downstream connections. We envision that there will be other producers on the system. We have non-op working-interest within our area as well who will likely want to ship on the crude line as the alternative is trucking on lease roads.

If you’ve ever been out to the area, the roads can be challenging to navigate especially under inclement weather. When you get a little bit of rain, it just becomes difficult to move trucks around. Placing the crude on pipe has always been a significant driver for WPX.

Thinking about gas infrastructure, WPX owns in-field gas gathering through a main CDP where we have a number of compressor banks which currently deliver rich gas to four gas processing outlets. WPX’s midstream JV processing complex will ultimately be the 5th outlet.

The WPX-Howard JV processing complex will start as a 200 MMcf/d cryogenic unit sometime during the second quarter of 2018, and then the second 200 MMcf/d train will be ready in early 2019.

OAG360: Howard’s going to fund the first $263 million of Cap-Ex for the projects. So what will the finished infrastructure look like after that investment? And what’s the total expected investment required to fully develop it?

GREG HORNE: On the first question, the $263 million largely covers the fully built-out crude system that can handle over 100,000 barrels a day and connects to most of our acreage. And then two trains, so 400 million a day of natural gas processing.

And on your second question regarding expectations around the nature of the fully developed assets, it’s pretty difficult to sit here and answer today.

Maybe a good way to address your question is WPX has announced it has over 4,000 or 5,000 drilling locations in this area. Depending on where crude oil prices go, the development of the assets will certainly follow suit. Suffice it to say that there’s plenty of running room to continue to add onto this infrastructure over the years to come. I don’t know what it will look like when it is fully developed, but it’s a safe bet to say it will likely be north of the $263 million investment.

OAG360: So after these are built out, what’s the route to market served by the oil gathering and then also cryogenic units and the gas pipes?

GREG HORNE: There are three crude outlets and one of them serves local refining; one of them gets to Midland, and then the main one that we’ve talked about publicly is the Oryx line, Oryx II, which delivers to Crane and Midland. The Oryx system will be our main line but we have the option to send volume to other outlets which will be a little bit smaller in nature.

In terms of markets for the natural gas liquids, a good majority of it will go to Mont Belvieu and then a smaller portion will head to markets in Corpus Christi.

On the natural-gas side, we’ve got two outlets, both of which move gas to Waha – El Paso Natural Gas and WhiteWater Midstream’s Agua Blanca line. We own an equity stake in the Whitewater line. Additionally, we proactively pursued 200 MMcf/d of takeaway from Waha to Katy, Texas beginning service in 2018 under a 10-year contract with ATMOS pipeline.

OAG360: As we said, WPX has said that the JV with Howard doesn’t include the 150 MCFs a day of natural gas compression capacity in the area. Could you talk about those assets?

GREG HORNE: So right now we have three compression banks consisting of 10 compressors each capable of moving approximately 150 MMcf/d of gas. A fourth bank is in the permitting process and we will continue to bring on new units to stay in front of our development plan. As it stands, we’ll continue to keep compression in our scope until we decide to do something different.

OAG360: What would you say is the most important aspect and outcome that you have achieved, or hope to achieve from doing this deal?

GREG HORNE: That’s a good question. I think for WPX, this deal has been unique in the midstream space. I run into a lot of midstream companies that are very congratulatory towards WPX on the transaction, and they might be saying that with a little bit of tongue-in-cheek. We were able to achieve a good valuation through a competitive process while avoiding a volume commitment. Granted, the superiority of the rock, the sheer quantity of the stacked pay, and the fact that the transaction contemplated midstream assets in the hottest basin in the U.S. likely had something to do with the valuation. For example, our previous midstream transactions over the last couple of years included volume commitments. That was largely due to those areas having less inventory and the basins not being named “Permian.”

I think we set the bar pretty high for others as they contemplate similar transactions. I have had conversations with other producers thinking along the same lines and stating something to the effect of: “You guys at WPX did a great deal, so if we’re going to go out and structure a similar transaction, I’m looking forward to similar valuations per acre or drilling locations.”

I think an important aspect of the transaction is that while we have great commercial people on our midstream and marketing team at WPX, we don’t have all the skillsets that midstream companies like Howard can bring to the table in order to execute such a robust midstream development plan. A key component of our doing this deal was to find a partner who was going to be a great operator, who knew how to move quickly, and who could stay in front of us.

We did contemplate selling 100% of the asset but we wanted to have a say in how things got developed and be on the board of the joint venture. So, we had to find the right partner that was agreeable to these terms, and the guys at Howard ended up at the end of the day being that partner for us.

So I think the outcome of doing the deal was a 50% ownership stake for WPX in what promises to be a great midstream business that is well positioned in the heart of the Delaware basin to offer services to other producers in the area.

OAG360: WPX says the JV is positioned to become a premier Delaware and midstream provider. Could you provide some quantification – what’s going to bring the most impact to WPX as far as value?

GREG HORNE: Well, when you look at the initial assets, they’re set up for WPX. However, in bringing on Howard as a partner, we immediately benefit from a wealth of experience when it comes to growing midstream assets and contracting with multiple producers. They know Texas very well. Early on, they’ve already been showing us significant deal flow in terms of how they can bring third parties into the system. Due to our 50% ownership, WPX is aligned and supportive of their efforts to bring in additional producers to a system that is well positioned to access multiple residue lines in the state of Texas, multiple crude outlets, and multiple NGL outlets.

We’ve got the opportunity to be a part of something that grows and is unique to the Delaware Basin.

OAG360: Could you talk about takeaway agreements that you have in place, who they’re with? Can you name any parties?

GREG HORNE: On the oil side, Oryx is the main one. And Oryx, again, goes to Crane and Midland. From there, we enter transactions to further move our crude downstream to markets such as Cushing, Corpus, and Houston.

On the NGL side, we have recently executed two transactions for transportation and fractionation which provide diversity of markets by reaching Mont Belvieu and Corpus Christi.

On the gas side, as previously mentioned, it’s primarily WhiteWater and El Paso to get to Waha. Again, as we started off the conversation, we see Waha becoming pretty constrained over the coming years and so we got out in front of it and worked with ATMOS Pipeline to move a significant portion of our gas down to Katy, Texas.

OAG360: WPX talked about creating long-term shareholder value with the Delaware midstream JV. You’ve got a lot of options and a lot of upside available, so how would you summarize that?

GREG HORNE: Well, you think about some of the recent transactions that have been announced and the EBITDA multiples that they’re fetching, we’re pretty excited about the future valuations for WPX and our partner. A few recent transactions point to valuations with EBITDA multiples in the high teens.

As we look at our EBITDA in two to three years associated with this midstream entity, you can just kind of imagine – let’s say, the options that become available to WPX. They’re anywhere from a monetization of our interest to developing a larger stand-alone midstream entity.

When you think about some of the other producers and what they’ve done with public entities around midstream assets, a significant piece of the valuation and annual growth comes from the decades of drilling inventory underneath the acreage.

WPX Director of Communications KELLY SWAN: It’s no secret that the Permian is the future of WPX and we’ve invested heavily there in acreage and have decades of drilling ahead of us. And it’s where we’re going to put more capital than anywhere else. And so making sure that those barrels have a home is absolutely critical. We’ve set some really aggressive production targets and that’s going to be key in delevering the company.

And so having this clear pathway to make sure we’ve got a market to which we can ship all of our products –that’s going to keep energy flowing, that’s going to be critical to the future of the company.