WPX Energy acquires 6.5 MBOEPD of production and 120,000 net acres in the Delaware Basin

WPX Energy (ticker: WPX) announced today that the company has acquired Panther Energy Company II, LLC and Carrier Energy Partners, LLC, expanding its footprint in the Delaware Basin. The acquisitions includes approximately 6.5 MBOEPD (55% oil) of existing production from 23 producing wells (17 horizontals), two drilled but uncompleted horizontal laterals, 18,100 net acres in Reeves, Loving, Ward and Winkler counties in Texas and 920 gross undeveloped locations in the Delaware, WPX said in a press release Thursday.

Acquisition highlights

- Expected to be immediately accretive to WPX shareholders on a cash flow and NAV basis

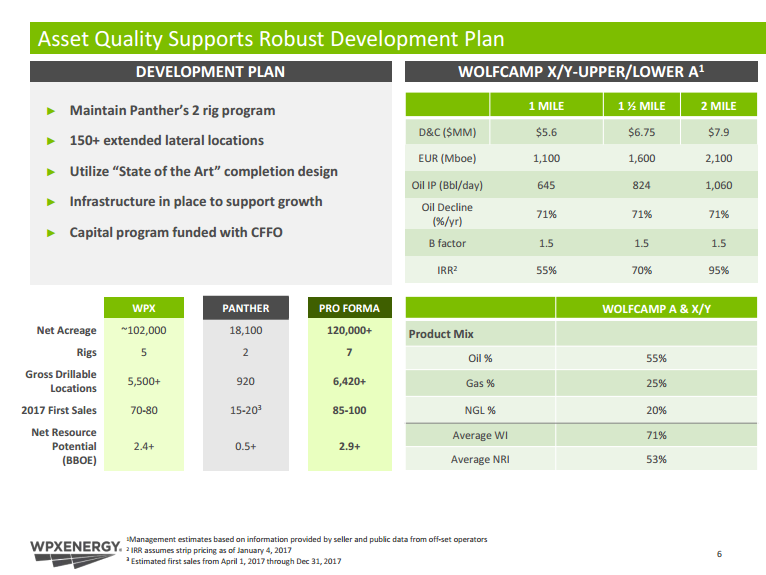

- Projected IRR on wells ranging from 55%-95% at current strip pricing

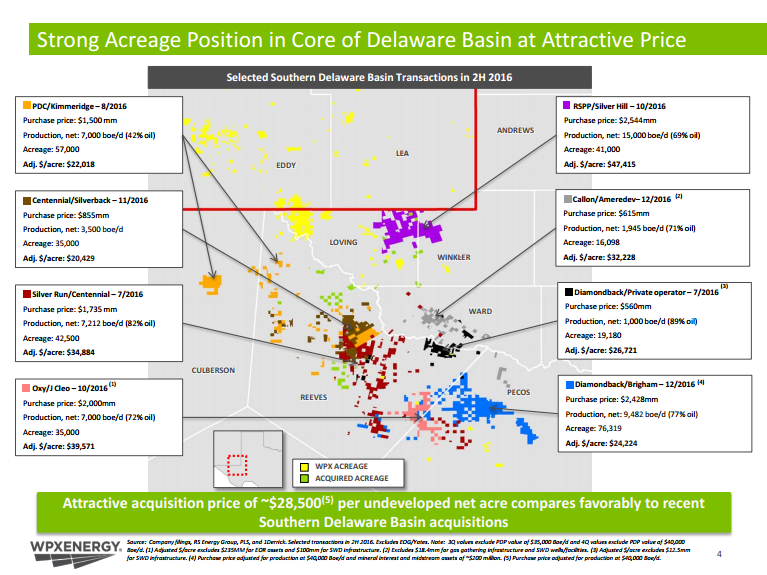

- Estimated acreage cost excluding flowing production is ~ $28,500 per acre

- Transaction valued primarily on three zones with upside in five additional zones

- EUR’s of ~ 1.0 MMBOE for Wolfcamp A and X/Y 1-mile laterals (55% oil)

- Increases WPX’s total gross drillable Delaware locations from ~5,500 to ~6,400

- New drillable locations include more than 150 long laterals (1.5-2 miles)

- Increases WPX’s growth trajectory for 2017-2020

- Offset operators: RSP Permian, Anadarko, Shell, Matador, Cimarex, Concho and Centennial.

Including the Panther transaction, WPX has added approximately 32,000 net acres in the core of the Delaware Basin at an average cost of $18,600 per acre since its transformative purchase of RKI Exploration and Production in August 2015. The average cost excludes flowing production.

A note from BMO Capital Markets following the deal estimates the transaction at $29,000 per acre, and notes that, at that price, the deal is accretive to where WPX trades ($42,000), while 2018EV/EBITDAX is reduced by 0.6x, and 2018 Debt/EBITDAX is lowered by 0.1x.

WPX expects the incremental cash flow from the purchase to fund the existing two-rig program on the acquired acreage, bringing WPX’s total rig program to seven rigs.

WPX also reaffirmed its full-year 2016 production guidance and announced that its fourth-quarter 2016 oil production is expected to exceed the company’s 42-44 MBOPD range, despite recent weather conditions in North Dakota’s Williston Basin. Additionally, WPX’s 2017 guidance remains unchanged prior to the pro forma impact of the bolt-on acquisition.

On a pro forma basis, WPX is now targeting 30 percent oil growth and 25 percent overall production growth in 2017, along with a targeted net debt/EBITDAX ratio at the lower end of the company’s previously announced range of 2.0x to 2.5x by year-end 2018.

WPX finances the deal with $600 million public offering

WPX plans to use cash on hand and the proceeds from an equity offering the company announced following the acquisition to finance its most recent Delaware expansion. The company announced Thursday that it has priced 45 million shares of its common stock at a price of approximately $13.35 per share for gross proceeds of approximately $600.8 million, according to a press release from WPX. The company is also granting underwriters a 30-day option to purchase up to an additional 6,675,000 shares of WPX stock.

The offering was upsized from the previously announced offering of 42,000,000 shares of common stock with an option to purchase up to an additional 6,300,000 shares.

The completion of the offering is not conditioned upon the acquisition, and if the acquisition is not consummated, WPX would use the net proceeds from the offering for working capital needs or general corporate purposes (which may include the repayment of indebtedness and other acquisitions), WPX said in the release.

The public offering will dilute WPX’s share by approximately 15%, according to a note from SunTrust Robinson Humphrey following the deal.