Russia at risk of a Fed rate-raise – Moody’s

A report from Moody’s Investors Service named Russia among four emerging markets most at risk from a potential increase in the U.S. interest rate, news that sent the ruble falling in value against the dollar for the first time in four days. The Russian currency slipped 0.6% to 65.86 to the dollar the day before the Fed’s decision, surpassed only by South Africa’s rand and Brazilian real, which along with the Turkish lira were cited by Moody’s as facing “exchange rate and financial-market instability,” according to Bloomberg.

Russia’s deputy finance minister downplayed the risks associated with a Fed rate raise, saying the ruble has already suffered a “hard adaptation” to the prospect of U.S. tightening. In its report, Moody’s said there is still a low risk for a “disorderly reaction” following the initial Fed liftoff in Russian markets.

Yesterday, the Federal Reserve decided not to increase its key interest rates from historic lows, citing persistently low inflation and concerns over the international market. The focus on the global economy creates a new precedent for the Federal Open Market Committee (FOMC), Art Hogan, director of equity research and chief market strategist for Wunderlich Securities, told Oil & Gas 360®; “The Fed [added] a third mandate: stability in world markets,” he said.

While the Federal Reserve did not decide to raise the interest rate, Russia’s currency still took a noticeable dip following the news. At 1:59 EST, the ruble stood at 65.81 to the dollar; following the announcement at 2:00 EST, it shed 0.7% of its value, falling to 65.38 at 2:01 EST. The value of the ruble fell further to 65.02 against the dollar before recovering.

Fed’s effect minimal on Russian bonds

A note from Citigroup Inc. disagreed with Moody’s assessment on the importance of the Fed’s decision on the Russian market, saying the decision would not trigger a “significant” move in the nation’s debt because the “single most important factor” for investors is the oil price.

“We see oil as the biggest risk factor for Russian assets,” said Viktor Szabo, a money manager who helps oversee $12 billion of developing-nation debt at Aberdeen Asset Management to Bloomberg. “From a macro point of view the dollar rate is less relevant for Russia now, as it is being shut out of the international financial market for new capital.”

The role of oil & gas to Russia’s economy: 50% of revenues

Oil and gas play a tremendous role in the Russian economy. In 2013, 50% of the federal budget revenues and 68% of total exports came from oil and gas, according to the Energy Information Administration. Rosneft (ticker: RNFTF) alone contributed about a quarter of the entire country’s tax revenue.

The difference in yield between Russian Eurobonds and U.S. rates has narrowed to the least in one-and-a-half months as oil prices stage a recovery, JPMorgan Chase & Co. data show. The gap widened to the most since March three weeks ago amid a renewed decline in the commodity.

With many foreign investors out of the Russian bond market following the implementation of international sanctions on Russia over its involvement in Ukraine, the path of domestic borrowing costs and the ruble are of greater importance in determining local sentiment toward OFZs, the Russian federal bond.

“Speculative capital left Russia last year,” Evgeny Shilenkov, the head of trading at Veles Capital in Moscow, said. “The Russian bond market is very locally driven now, liquidity is low.”

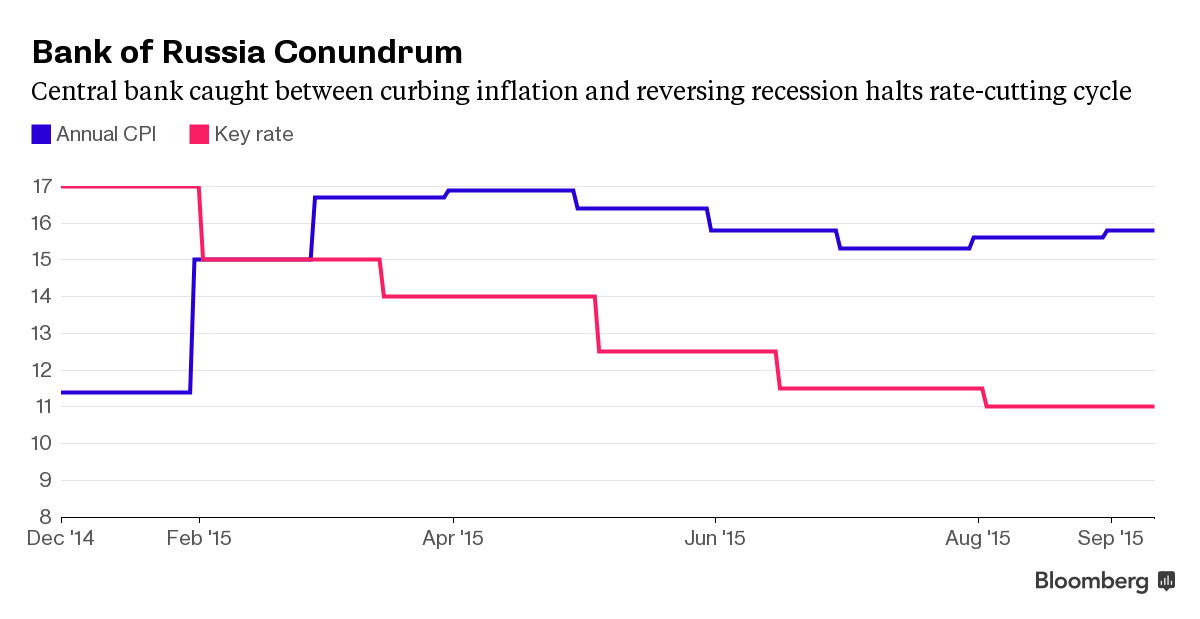

Capital outflows slowing, Russia pauses rate cuts

Capital outflows from Russia slowed 32% to $52.2 billion in the first eight months of the year, according to Russian Central Bank Governor Elvira Nabiullina, after policy makers kept the Russian benchmark rate unchanged at 11% following five cuts since December.

Barclays said the Russian central bank will likely hold off on cutting rates further until “inflation actually begins to decline,” while Goldman predicted another 100 basis points of reduction by the end of the year.

The central bank downgraded its forecast for gross domestic product in 2015, from a decline of 3.2 percent to between 3.9 percent and 4.4 percent, on the back of a deterioration in external conditions, reports Bloomberg. Inflation, estimated at 15.8 percent as of Sept. 7, is set to slow to about 7 percent next September, it said. Oil prices will be at about $50 for the next three years, according to the Russian central bank.

Oleg Kouzmin, an economist at Renaissance Capital in Moscow, said currency volatility will remain key in deciding future rate cuts. It “fully depends on the ruble” whether Nabiullina cuts by a half point by year-end or keeps rates on hold in the period, he said.