CAMAC Energy Inc. (ticker: CAK) is a Houston-based oil and gas company engaged in the exploration of offshore oil and gas leases in deep water Nigeria. The company is preparing to develop and exploit two separate wells in the Oyo Field and generate a total of 14 MBOEPD. In the past year, CAK has acquired the remaining interests in blocks OML 120 and 121 and ratified a petroleum agreement with the government of Ghana for the Tano offshore block. The company also began listing on the Johannesburg Stock Exchange (ticker: CME) and closed a $270 million equity investment. On April 29, 2014, Arctic Securities initiated coverage on CAMAC Energy and with a Buy rating.

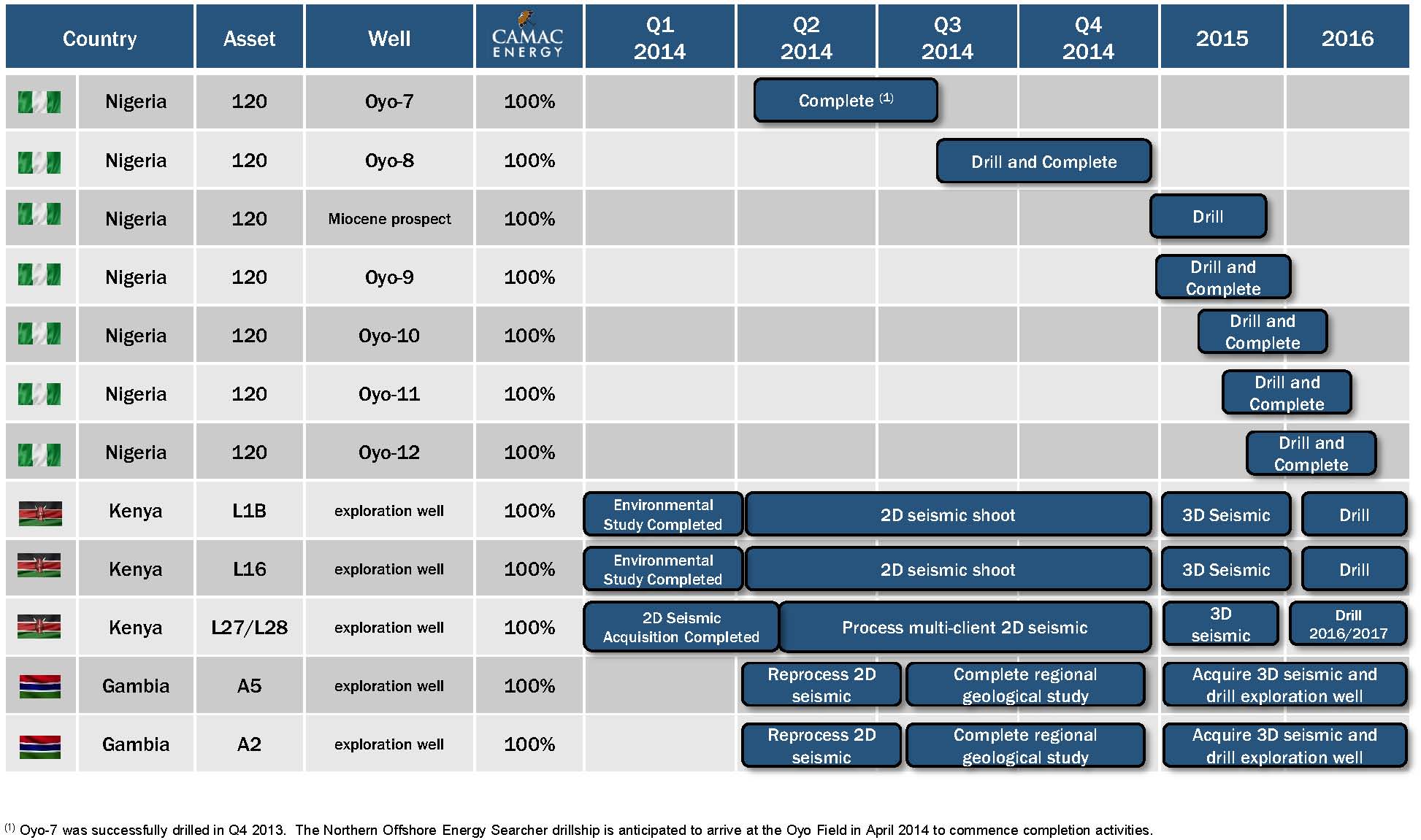

On the exploration front, CAK has prepared for 2014 Oyo Field production by securing the Northern Offshore Energy Searcher drillship for two years and obtaining the FPSO Armada Perdana for up to seven years through separate contracts. Completion operations are expected to begin in May 2014 with production commencing in October. CAK owns 100% of interest in the blocks and says it will use the cash flow from Oyo operations to fund ventures in its other properties.

In a conference call with investors and analysts on May 8, 2014, Kase Lawal, Chairman and Chief Executive Officer of CAMAC Energy, said, “The results of these drilling efforts will make 2015 the most profitable year in the history of the company.”

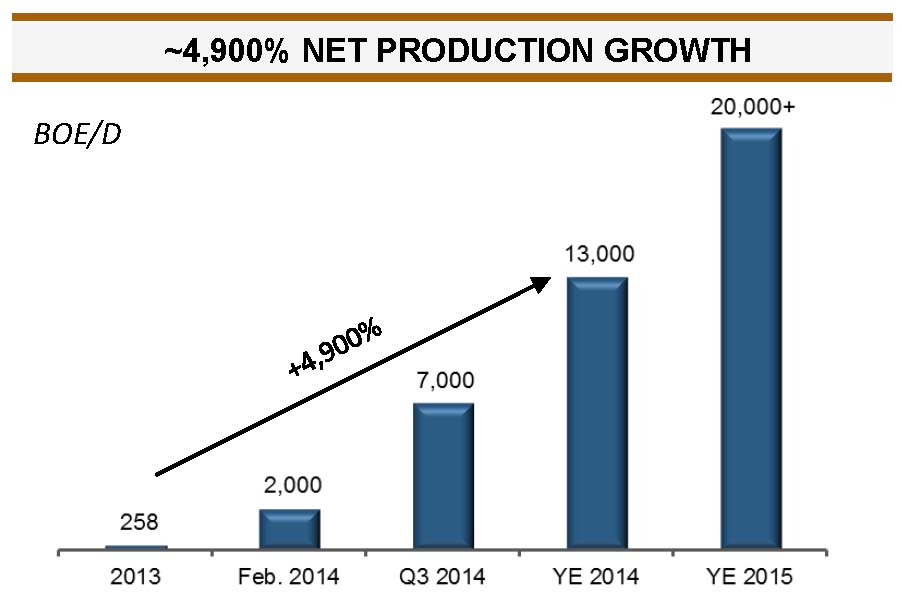

Q1’14 results include revenues of $19.9 million on net production of 1.7 MBOEPD. The company holds roughly $70 million in cash and anticipates spending $190 million in 2014 to advance operations. CAK management said the spending will likely be distributed evenly among the next three quarters.

Ghana, Kenya and Gambia

The Tano block is roughly 25 kilometers offshore Ghana and consists of about 370,000 acres. The area is believed to hold three discovered fields and CAK is enlisting the services of an independent consulting firm to explore production feasibility. The exploration results must be determined within nine months, per the terms of the government agreement. CAK’s subsidiary, the operator and 60% interest holder of the block, will establish potential results through geologic and 3D seismic data.

Exploration is also underway in Kenya. Testing on four blocks, with two onshore and two offshore, has resulted in planned exploration wells be drilled on the onshore properties as early as 2015. Five leads have targeted unrisked prospective resources of 900 MMBO in one of the onshore spots. Plans for the offshore blocks have yet to be determined but CAK is actively testing the region, which consists of more than nine million net acres.

Exploration is also occurring in Gambia and the first offshore exploration well is expected to be drilled in 2016.

Kick Starting the Oyo

CAK has full ownership of its Oyo Field blocks and anticipates drilling and completing a total of three wells by year-end 2015. Once operational, CAK estimates production will exceed 20 MBOEPD, up from less than 2 MBOEPD in Q1’14. Tests have concluded both the OML 120 and 121 hold the Miocene formation. In the conference call May 8, 2014, Earl McNiel, Senior Vice President and Chief Financial Officer of CAMAC Energy, said, “Revenue on a per barrel basis was $109 per barrel as we continue to garner our premium to Brent due to the high quality of crude oil from the Oyo field.”

Shell’s (ticker: RDS-B) nearby Miocene-producing Bonga field has produced 450 MMBO since being brought online in 2005. CAK has identified a total of six Oyo wells and the latter half are expected to be drilled in 2H’15.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. A member of EnerCom has a long-only position in Shell.