EnerCom traveled with CAMAC Energy to meet with investors in New York City during May 2014. Click here for the company’s latest presentation.

CAMAC Energy Inc. (ticker: CAK) is a Houston-based oil and gas company engaged in the exploration of offshore oil and gas leases in deep water Nigeria. The company is preparing to develop and exploit two separate wells in the Oyo Field and generate a total of 14 MBOPD. In the past year, CAK has acquired the remaining interests in blocks OML 120 and 121 and ratified a petroleum agreement with the government of Ghana for the Tano offshore block. The company also listed on the Johannesburg Stock Exchange (ticker: CME) and closed a $270 million equity investment with the Public Investment Corporation Limited of South Africa. On April 29, 2014, Arctic Securities initiated coverage on CAMAC Energy with a Buy rating.

CAMAC has secured a drillship and utilizes an FPSO to exploit its offshore Nigeria assets. Production from the Oyo-8 well is currently scheduled to commence in October and the incoming cash flow will be used to fund CAK’s other prospects in West Africa. The company plans to drill two additional Oyo wells in 2015.

“The results of these drilling efforts will make 2015 the most profitable year in the history of the company,” said Kase Lawal, Chairman and Chief Executive Officer of CAMAC Energy, in the company’s Q1’14 conference call with analysts and investors.

On the Road

Below are a series of questions management fielded from investors during the trip:

- How did CAMAC Energy acquire 100% working interest in the OML 120/121 fields offshore Nigeria?

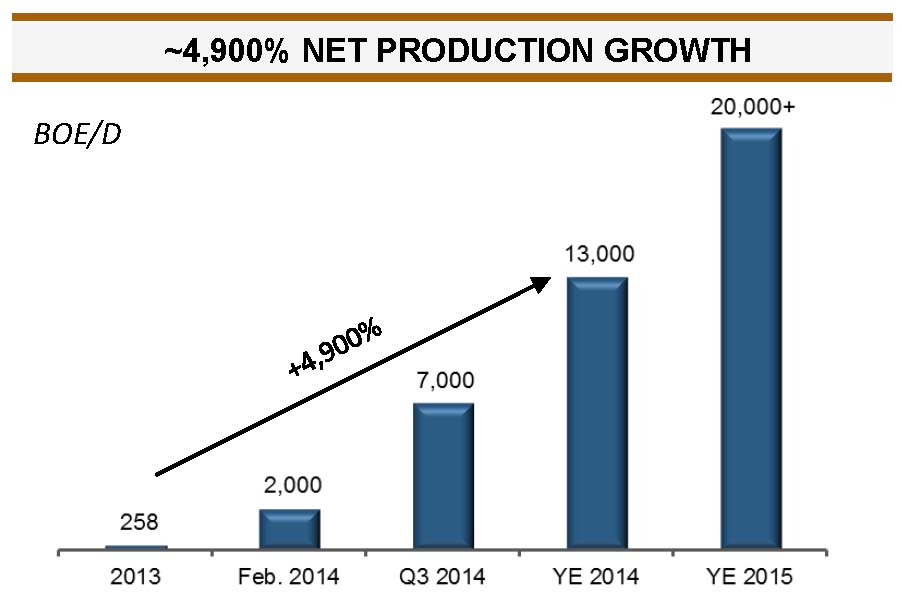

- The company is forecasting an increase in production from approximately 2,000 net BOPD to over 14,000 BOPD by the end of 2014. How many wells will this require CAMAC to drill?

- Does CAMAC have deep Miocene zone potential on its offshore Nigeria blocks to complement the existing Pliocene production and prospects?

- What are the major logistical and operational considerations CAMAC must deal with in terms of long lead time equipment, security and offtake capacity for offshore Nigeria?

- What will your hedging policy be when the company is producing 14,000 BOPD?

- Please explain the royalty structure associated with your offshore Nigeria blocks.

- What is the company’s plan to address its share count?

- How many Pliocene and Miocene prospects does CAMAC Energy have on its OML 120/121 blocks?

- How long is the drilling rig on contract and what is the company’s planned drilling program offshore Nigeria over the next 18months?

- Will CAMAC Energy consider industry partners for the development of its offshore Kenya blocks?

- When will onshore test drilling commence in Kenya?

- What are the project cash flow numbers for 2014 and 2015 given the planned drilling of three to four wells in OML 120/121?

- Please explain your exploration and G&G plan for your offshore Gambia assets.

- How long will it take between drilling a well and placing it on production in offshore Nigeria?

- What is the processing capacity of the FPSO CAMAC presently uses for OML 120/121 production and is the FPSO of sufficient capacity to handle your expected production growth?

- What is your farmout strategy for your various African exploration projects?

- Please explain the composition and experience of your technical staff.

- Do you anticipate any changes to the Nigerian Petroleum Laws, if/when enacted, may impact CAMAC Energy and its investors?

- What are your operating costs for your offshore Nigeria production and what impact will rising production have on your per barrel costs?

- Does CAMAC Energy realize any benefit from cost pool recovery for offshore Nigeria production?

CAK Valuation

With its long-awaited Oyo field results on the horizon, CAMAC is positioned to finally make the landmark switch from preparation to production. EnerCom’s E&P Weekly database, consisting of 87 companies, notes the street has responded in high hopes to the Oyo wells. CAK currently trades at a price/cash flow per share multiple of 15.8x and has $142 million in debt despite the long process to establish offshore operations along with minimal production. Its debt to market cap ratio is just 18% – well below the industry median of 37%.

[sam_ad id=”32″ codes=”true”]

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.