Short-term prices likely to remain low

Both the Energy Information Administration (EIA) and International Energy Agency (IEA) released their most recent pricing outlooks for the energy markets today, giving a glimpse into what two of the most widely followed energy agencies see as the future of energy markets.

The EIA’s Short Term Energy Outlook (STEO) forecasts prices out through 2016, while the IEA’s World Energy Outlook (WEO) takes a longer-term look at energy markets out to 2040. Both agencies believe that oil prices will remain below the $100-mark, even 25 years from now.

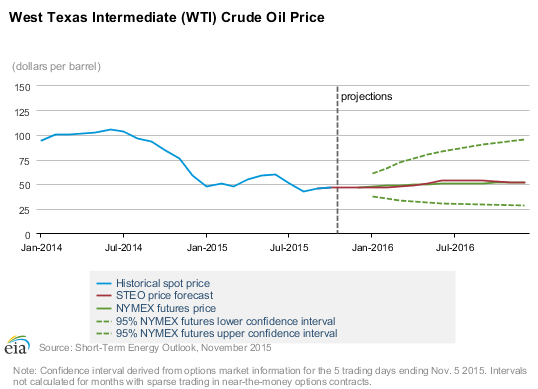

In its release today, the EIA left its forecast for Brent crude for the remainder of this year at $53.82 per barrel, while lowering its prediction for 2016 by $2 per barrel to $56.24 per barrel. The EIA’s expectations for U.S. crude oil benchmark WTI in 2015 is $49.88 with a slight increase in 2016 to $51.31 per barrel.

The EIA’s projections for 2016 have a wide lower and upper limit of $35 per barrel and $66 per barrel, respectively, in February 2016. The administration citing higher than normal levels of price volatility compared to last year. The number of days on which the value of WTI has changed more than 2% is nearly five-times higher this year than in 2014, according to data compiled by EnerCom Analytics. The limits continue to diverge through 2016 with the EIA modeling WTI price at $28-$95 per barrel by December of next year.

IEA also expects prices to be lower for longer

The IEA WEO released today put a strong emphasis on the importance of renewable energy sources moving toward 2040, and forecasted oil prices at lower levels than 2014 through 2040. According to the IEA’s factsheet, the agency sees oil prices reaching $80 per barrel in 2020 in their New Policies Scenario, the World Energy Outlook 2015’s central scenario.

Despite the expectation that prices will trend higher in the medium-term, the IEA said it could not rule out the possibility that oil prices could remain in the $50-$60 range well into the 2020s, edging higher toward $85 per barrel by 2040. The IEA admits, however, that the low oil price scenario “contains the seeds of its own demise,” saying that the longer oil prices stay low, the shorter the market will become in the long-run, thus increasing the risk of a correction and large price upswings in the future.

If prices do remain lower for longer, the IEA cautions that dependence on cheaply produced oil from OPEC could reach levels similar to those seen in the 1970s, risking a sharp market rebound if investment falls short on new production as demand continues to grow.

Based on the IEA’s New Policies Scenario, energy demand will grow by nearly one-third between 2013 and 2040, with all the net growth coming from non-OECD countries and OECD demand ending 3% lower. Oil production grows by 12% from 2014, to over 100 MMBOPD in 2040, led by non-OPEC countries through 2020, and then by OPEC later on.

Shale boom pauses, returns

Production from U.S. tight oil operations is expected to decline substantially in the short-term due to the drop in oil prices, the IEA said in its release today. But tighter markets will eventually raise prices, ultimately pushing U.S. production back up again in the mid-term, with production growing by as much as 1.5 MMBOPD by 2020 to over 5 MMBOPD.

Demand is expected to grow at an average of 900 MBOPD per year until 2020, but then subsequently slow, with global demand reaching 103.5 MMBOPD in 2040, up about 13 MMBOPD from 2014 levels. By 2040 OECD consumption has fallen by 11 MMBOEPD but this is almost exactly cancelled out by the twin pillars of demand growth: India and China (up 6 MMBOPD and 5 MMBOPD respectively). Elsewhere the Middle East sees oil demand climb by 3.5 MMBOPD, other non-OECD Asian countries by 2.7 MMBOPD, and Africa by 2.5 MMBOPD. The transport and petrochemicals sectors add 16.5 mb/d to 2040, offset only partially by slight reductions in the power sector and use in buildings.

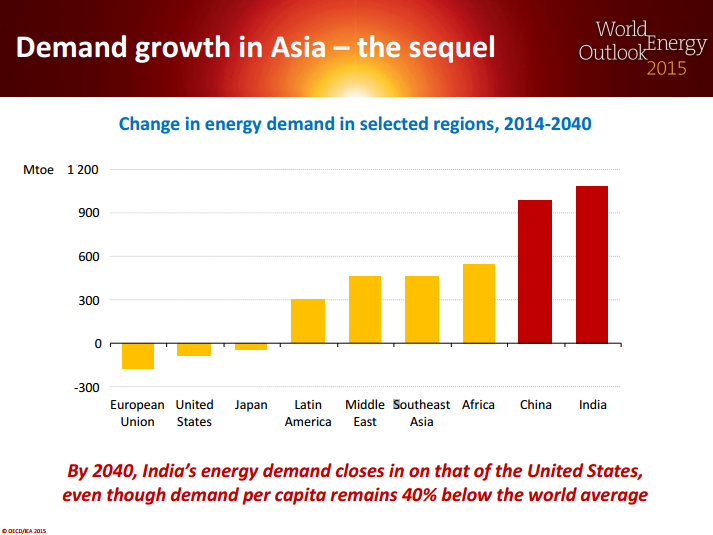

India set to become the new China

The IEA sees China’s demand for energy reaching a plateau near current levels as the country’s economy makes a shift towards a more service-industry driven model, reducing its need for further energy supplies. In China’s place, the IEA believes that India will take up the mantle of Asia’s largest center of energy demand growth.

The IEA’s expectations for increased demand growth out of India mirrored comments made by Stuart Bergman, deputy chief economist and director of economic and political intelligence center for Export Development Canada, made earlier in the year. “Emerging market economies like India can sustain far more exciting rates of growth than our traditional trade partners, as they converge with the developed world,” said Bergman.

The IEA sees Asia becoming the final destination for roughly 80% of regionally traded coal, 75% of oil and 60% of natural gas in 2040. China will become the world’s largest oil importer before 2020 and India the second-largest oil importer around 2035.

Middle East oil exports accelerate after 2020 and natural gas exports rebound after 2025. North American natural gas exports are around 85 billion cubic meters (Bcm) by 2025 and the region is self-sufficient in oil by the mid-2020s. Natural gas imports into the European Union grow by 30%, but sources of supply also diversify.

An increasing focus on renewables

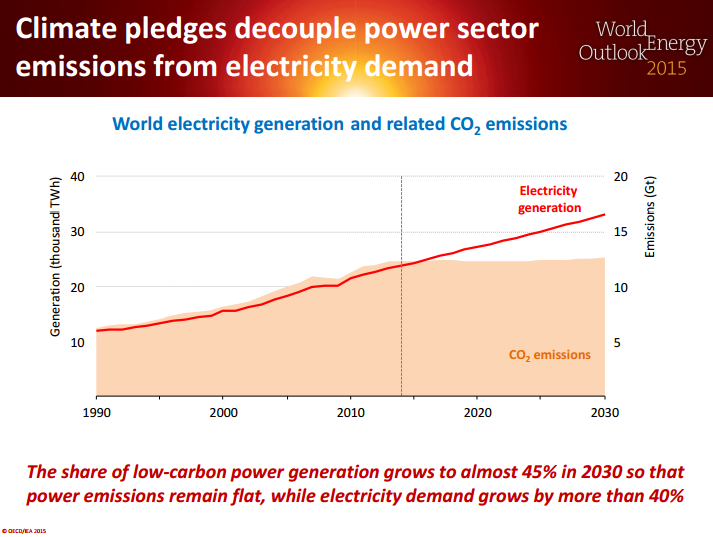

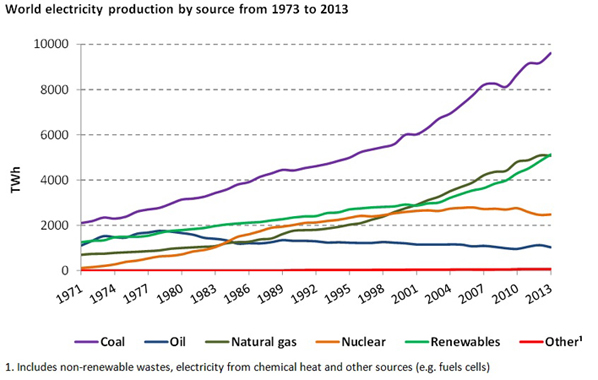

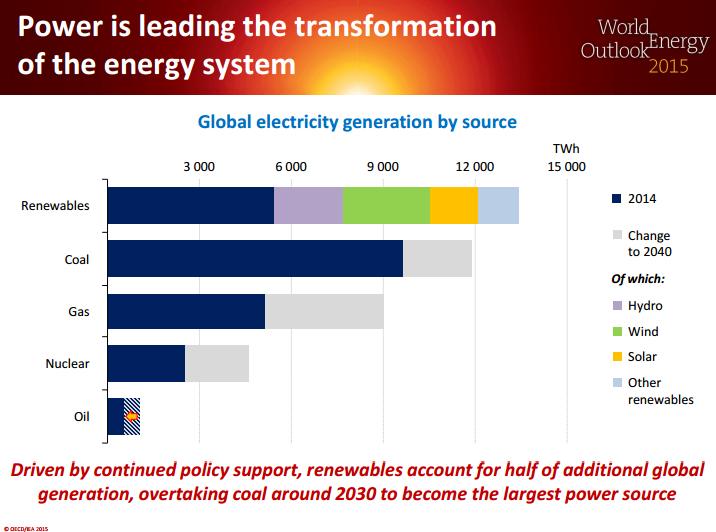

A major focus of the IEA’s 2015 outlook was the importance of renewable energy as many world powers look to commit to stronger climate goals ahead of the Paris COP21 climate summit later this month. “Renewables contributed almost half of the world’s new power generation capacity in 2014 and have already become the second-largest source of electricity (after coal),” the IEA said in its outlook.

The World Energy Outlook sees renewable energy sources overtaking coal as the largest source of electricity generation by the early 2030s. Based on the agencies forecasts, renewables-based generation will reach 50% in the EU by 2040, around 30% in China and Japan, and above 25% in the United States and India. Overall demand for electricity is expected to grow by more than 70% by 2040.

IEA: shift to renewables not enough to reach climate change targets

Despite the heavy focus on renewables, the IEA believes that further action is needed to reach global climate change targets. The net result of the greater use of renewables would be a decoupling of electricity generation from CO2 emissions, but long-term temperature increases would still reach 2.7 OC by 2100.

“As the largest source of global greenhouse-gas emissions, the energy sector must be at the heart of global action to tackle climate change,” said IEA Executive Director Dr. Fatih Birol.