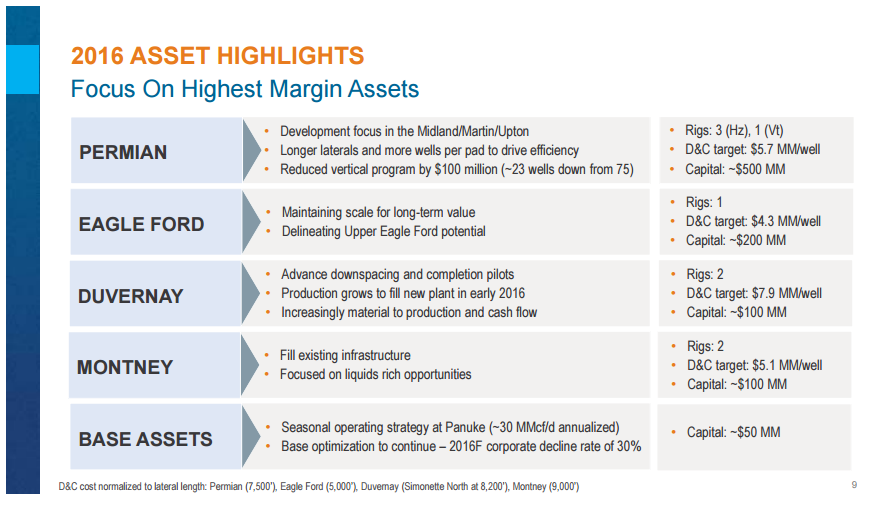

Encana remains focused on its core assets

Encana Corp. (ticker: ECA, Encana.com) continued to increase production and lower its debt amid the crash in crude oil prices. The company said that it produced 274.4 MBOEPD in the fourth quarter of the year from its four core assets: the Permian, Eagle Ford, Duvernay and Montney. This production represented a 35% increase from the same quarter in 2014, and was 4.4 MBOEPD above the company’s production target, Encana said in its press release.

Including the assets outside of the company’s core, Encana produced 406.8 MBOEPD in the fourth quarter, and averaged 405.9 MBOEPD, with liquids averaging 133.4 MBOPD, a 54% increase from 2014. Full-year natural gas production was 1,635 MMcf/d, the company reported.

The increased production helped to push the company’s cash flow for the quarter up 3% from Q3’15, despite lower oil prices. Encana reported cash flow of $383 million in the fourth quarter, compared to $377 million in Q3.

For the full year, Encana reported annual cash flow of $1.4 billion, and a 2015 operating loss of $61 million. The company’s net loss for the year came in at $5.2 billion, which was largely due to a $4.1 billion after-tax non-cash ceiling test impairment, and a non-operating foreign exchange loss of about $700 million.

The company’s 2016 capital budget is focused on production from Encana’s core assets, with 95% of its $0.9-$1.0 billion budget targeted at those four plays. ECA’s 2016 budget reflects a 55% decrease from its full-year 2015 budget. Encana does not expect the lower budget to affect production, with the company forecasting 340-360 MBOEPD of total production, with liquids averaging 120-130 MBOPD and natural gas in the 1,300-1,400 MMcf/d range.

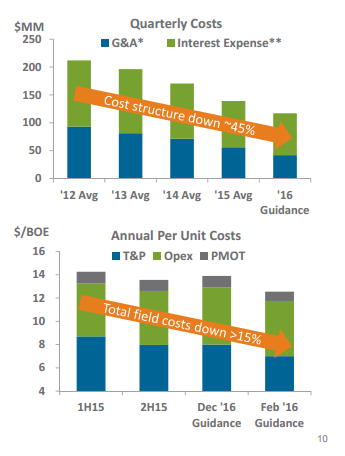

Shoring up the balance sheet and reducing costs

In its quarterly report, Encana said that the company reduced its debt by nearly 30% over the course of the year. Through the sale of non-core assets, and a C$1.44 billion (US$1.05 billion) equity offering, the company was able to pay down roughly $2 billion in debt.

The company has $4.5 billion of revolving unsecured credit facilities which do not mature until 2020. Encana’s only financial covenant is to maintain a debt-to-adjusted market cap ratio below 60%. As of December 31, 2015, Encana’s ratio was 28%, according to the company.

ECA reported total debt of approximately $5.1 billion, comprised of $5.4 billion of fixed and revolving debt, net $271 million cash and cash equivalents. Encana’s next debt maturity is in May 2019, when $500 million of senior unsecured debt will come due.

Doug Suttles, Encana president and CEO, said the company remains focused on improving its balance sheet, lowering cost structures and increasing financial flexibility. Encana reported that it exceeded its goal of $375 million in increased capital and operating efficiencies in 2015 by $25 million.

Encana plans to lower its cost structure by a further $550 million in 2016. ECA expects reductions of:

- $75-$125 million in transportation and processing costs

- $50 million in operating costs

- $25 million in production, mineral and other taxes

- $50 million in overhead costs

Encana’s expected overhead cost savings include an approximate 20% workforce reduction, bringing total workforce reduction since 2013 to over 50%. Additional capital efficiencies are expected to contribute a further $50 million of cash flow compared to previous 2016 guidance.

75% of liquids and natural gas production hedged through the end of the year

In addition to lower costs and a strong balance sheet, Encana reported that the majority of its oil and condensate, as well as its natural gas production is hedged through the end of 2016. Encana has hedged 75% of both liquids and natural gas production from March to December, it said in its release.

ECA’s oil and condensate hedges include 54 MBOPD of production from March to December, hedged at WTI fixed price contracts at an average price of $56.33 per barrel. The company also has 15 MBOPD of production during that time frame hedged under three-way options. The WTI three-way options are a combination of a sold call, purchased put and a sold put with average prices of $63.01, $55.00 and $47.14 per barrel, respectively.

On the natural gas side, Encana has 740 MMcf/d of production hedged using NYMEX fixed price contracts at an average price of $2.76 per Mcf, and 335 MMcf/d in costless collars with puts and sold calls averaging $2.22 per Mcf and $2.46 per Mcf, respectively. ECA reported that it also has approximately 255 MMcf/d of expected 2017 natural gas production hedged under three-way options. The three-way options are a combination of a sold call, purchased put and a sold put with average prices of $3.07, $2.75 and $2.26 per Mcf, respectively.