Residents of the northeast United States are likely to dismiss any notion of the upcoming winter season (it was 90 degrees in Boston today), but the chilly months that accompany football season are indeed approaching.

Winter for New Englanders also brings wide disparities in consumer power costs, plagued by a lack of infrastructure in the nearby Marcellus/Utica region. ICF International, an energy consulting firm, estimated last year that $313 billion of infrastructure investment is needed by 2035 to keep pace with growing domestic natural gas operations.

The remarkable need for midstream and downstream support is a two-fold result of the shale boom and New England’s shift to gas-fired electricity generation. In its recent ICF International report titled “New England Energy Market Outlook,” the firm mentions about half of all current power in the northeast United States is gas-fired, compared to only 15% in 2000. With the retirement and decommissioning of nuclear and coal-fired plants, ICF expects the natural gas utilization to continue to climb.

Infrastructure Shortage

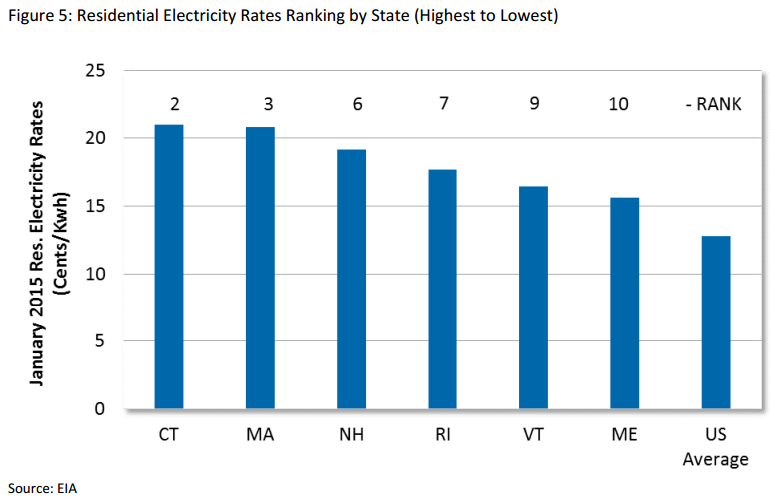

Natural gas infrastructure in the northeast is being constructed at a breakneck pace, yet still severely lags the buildout compared to other regions. The ICF report mentions all six New England states rank among the top ten U.S. states in terms of the highest residential electricity rates and are 45% higher than the U.S. average.

A key piece of the higher prices are due to the constrained takeaways – an element that becomes more pronounced in the winter season. ICF refers to non-firm supplies, dependent on pipelines and storage services, as “interruptible” sources that can be affected particularly by cold weather. A rather infamous example can be traced back to January 2014, when stalled operations and freezing pipelines briefly skyrocketed the spot price at a northeastern hub to $123.63/MMBtu. The phenomenon, referred to as the “polar vortex,” cost New England consumers an estimated $3.7 billion in wholesale electricity costs.

Production is not expected to slow down. ICF believes Appalachia output will reach 42.0 Bcf/d by 2035 – more than double the current output of 19.1 Bcf/d, based on data from the Energy Information Administration. In the meantime, potential unmet demand is expected to reach 1.7 Bcf/d in 2020 and rise to 3.2 Bcf/d in 2035.

The Case for New Pipelines

The Case for New Pipelines

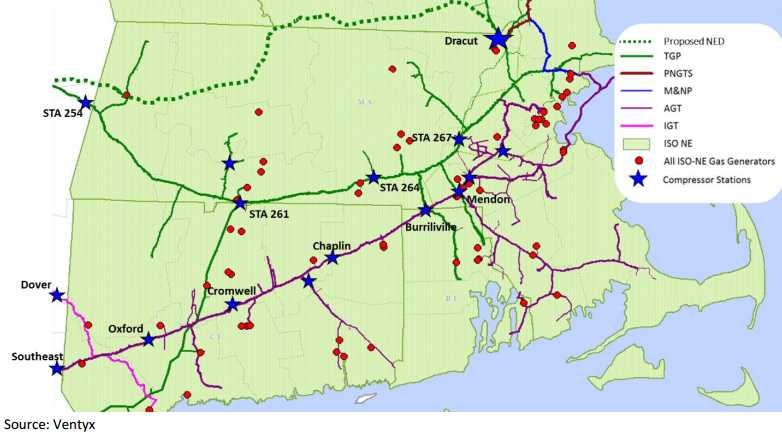

The ICF study, commissioned by Kinder Morgan (ticker: KMI), was designed to show the benefits realized by consumers if Kinder Morgan’s Northeast Energy Direct project is approved. The proposed pipeline would deliver 1.3 Bcf/d to northeast markets and could be in service by November 2018, saving a projected $2.1 billion annually in wholesale electricity costs from 2019 to 2028.

Kinder Morgan leading the charge on an energy project is nothing new. The Houston-based company is North America’s largest midstream provider and became the continent’s third largest energy company upon the $70 billion merger of its publicly traded units in August 2014. The combined footprint of the entity consists of approximately 84,000 pipeline miles and 165 terminals, and is responsible for moving roughly 33% of total U.S. gas demand. Approximately $48 billion has been invested in acquisitions or expansion projects since its inception in 1997, and another $9.4 billion of identified growth projects have already been identified over the next six years.