Two Wild Cards, Two Steps to Rebalance

(NOTE: Part One of this two-part analysis was published yesterday and can be accessed here.)

Wild Card No. 1: Iran

Iran is the loudest blender of the oil market margarita.

The EU used to be the first trading partner of Iran, but due to the sanctions regime, China, the UAE and Turkey are now Iran’s main trade partners, followed by the EU. Total EU imports from Iran decreased by 86% between 2012 and 2013, and total EU exports decreased by 26% during the same period.

Iran’s main imports are: non-electrical machinery (17% of total imports), iron and steel (14%), chemicals and related products (11%), transport vehicles (9%) and electrical machinery, tools and appliances (7%). They don’t produce iPhones, manufacture cars, or high tech products for export. 82% of the country’s exports are crude oil and natural gas. The proposed removal of sanctions will put the country into hyper-over drill mode to put more oil into the market, but the exact amount is widely speculative. The sanction removal is not a guarantee, considering some of the backlash it has received for potentially restricting the exact conditions to Congress.

The EIA published a report detailing the effects of lifting sanctions in late 2013: “The imposition of sanctions on associated insurance and transportation services by the European Union had a significant effect on Iran’s exports when implemented in July 2012, but Iran has been able to create arrangements that allow it to export limited quantities of oil to several countries. EIA does not anticipate those countries significantly increasing their oil imports from Iran, so without an easing of sanctions covering Iran’s ability to sell additional oil, the country is unlikely to significantly increase its production or exports in the short term.”

Two years later, the general unknowns associated with lifting sanctions and allowing Iran to reenter the oil market has thrown prices for another loop. Dr. Sara Vakhshouri, an expert on Iran and president of SVB Energy International, told Oil & Gas 360® that “This absence of knowledge and understanding seems to create more of psychological impact on the market and the prices, rather than an actual effect.”

How Many Barrels and When?

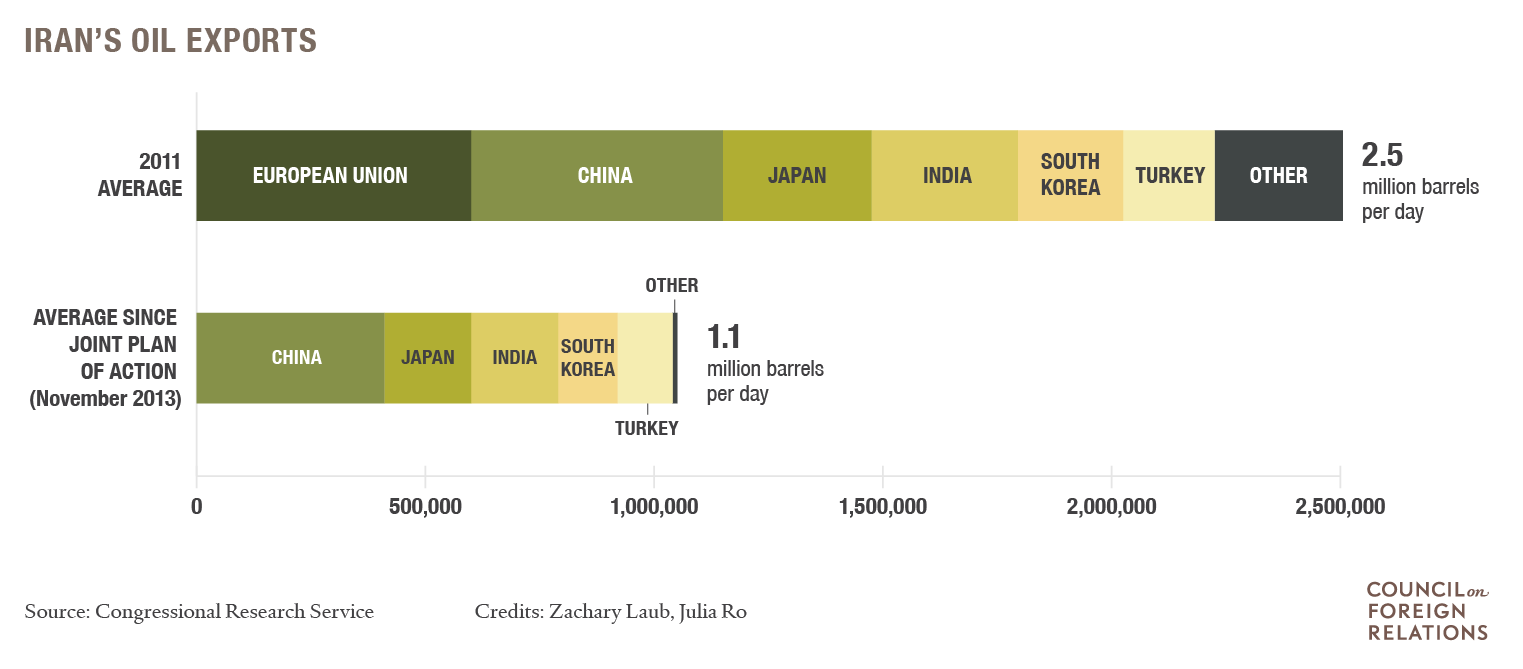

2.5 Million Barrels?

In the event that sanctions are lifted, Iran says it hopes to return to pre-sanction export levels of about 2.5 MMBOPD, which would be more than double its current exports of 1 MMBOPD. But some U.S.-based energy analytics firms are not convinced.

600,000 Barrels?

Wood Mackenzie believes Iran has the potential to be a key source of global supply, but not until after 2020. Wood Mackenzie believes an actual impact won’t be felt for about three years. A research note says, “On this basis, our analysis shows that Iran could gradually add 0.6 MMBOPD of crude oil production to global supply by the end of 2017 which is not expected to place significant downward pressure on prices.”

700,000 Barrels?

700,000 Barrels?

Raymond James issued a similar outlook in March, saying that, in theory, 0.7 MMBOPD is the most that could resurface. In the next 18 months, the firm believes only 0.5 MMBOPD will actually reach the market. Raymond James points out two critical factors in Iran oil development; technical issues and production already being in “over-the-hill” mode.

Iran’s oil minister, Bijan Zanganeh, said his country needs $200 billion to completely revitalize its dated oil and gas sector, while SVB Energy believes a minimum of $70 billion is required to reach the mid-term production goal.

Has Iran Already Hit Peak Oil?

Raymond James points out that 2011 production levels of 3.51 MMBOPD were already lower than volumes achieved in 2000.

“It doesn’t strike us as overly aggressive for Iran to get back to its all-time peak levels (around 4.0 MMbpd) by 2020 – provided that the political backdrop remains favorable, i.e., Iran complies with its nuclear obligations and does not attempt to renege,” the firm concludes, adding that “0.5 MMBOPD of additional supply eased in over the next 18 months would pale in comparison to the 1.7 MMBOPD of additional supply that U.S. producers added just last year.”

Dr. Iman Nasseri, a senior consultant with Facts Global Energy in the United Kingdom, believes such accusations are incorrect. Nasseri worked for Iran’s Institute of International Energy Studies, the research arm of the Ministry of Petroleum, prior to his current position.

“A lot of people have been saying Iran has lost its potential, and that it takes years to turn it back on, but they haven’t actually been to Iran,” Nasseri told Oil & Gas 360®. “We’ve been talking with the current administration, and they are telling us that they have been maintaining fields in the past two years and the fields are ready to increase production by about 500 MBOPD, and then they can ramp up to an additional 1 MMBOPD, which is basically pre-sanctions levels.”

4.2 Million Barrels by Mid-2016?

Nasseri believes Iran’s overall production (not exports) could climb to 4.2 MMBOPD as early as mid-2016, while the sanction removal will revitalize Iran’s entire industrial sector. The lack of foreign investment has clearly strained Iranian budgets – Verisk Maplecroft, an analytics provider, estimates public spending declined 30% since 2012. The World Bank says that according to unofficial sources, Iran’s unemployment rate has climbed to roughly 20%, refuting claims from the Iranian government that rates are half that amount.

“Some 750,000 youth are estimated to enter the labor market every year, with a large portion becoming unemployed, abandoning their job search and joining the ranks of the economically inactive population,” the World Bank report says. “The government estimates that the country must create some 8.5 million jobs over the next two years with stated of objective to reduce the unemployment rate to 7% by 2016.”

Wild Card No. 2: Mexico

Mexico desperately wants to boost its lagging crude oil output, so it has invited foreign investment to its oil and gas sector for the first time in almost eight decades.

But when the Latin American country hosted its first public mineral auction since 1938, only two of the 14 shallow water blocks were sold. An additional seven blocks received bids but did not meet the government’s requirements. The blocks that were sold require the buyer to provide a whopping 56% and 69% of their respective proceeds to the Mexican government. The buyer who won the two blocks via a consortium was Mexico’s first independent hydrocarbon company, Sierra Oil & Gas.

“People are assuming the first bidding round was a failure, but I think it’s a question of bettering the procedure,” said Ricardo Garcia-Moreno, Partner for Haynes & Boone. An expert on Mexico’s energy reform, Garcia-Moreno is a featured speaker at EnerCom’s The Oil & Gas Conference® 20 in mid-August.

“All of this is new and has occurred within the last two years, so it’s been very fast and there are some growing pains. They’re making great strides to get the blocks out, and I anticipate there will be much greater interest when the deepwater blocks are auctioned off,” Garcia-Moreno told Oil & Gas 360®.

Bloomberg reported that BP plc (ticker: BP) implored Mexico to improve their terms in order to attract investment, and Mexico’s oil regulator voted earlier this week to sweeten the rules for its second oil field auction. According to Reuters, recommendations include lowering a required corporate guarantee.

Mexico’s next auction consists of five shallow-water production-sharing contracts that cover blocks containing proven reserves.

The next blocks are scheduled for auction on Sept. 30, 2015. If its terms for buyers at future sales are attractive to outside E&Ps, then Mexico could become another bona fide wild card by decade’s end.

Operators to Oil and Gas Countries: Show Me the Money

ExxonMobil (ticker: XOM), did not renew an onshore concession in Abu Dhabi due to insufficient returns. “The Abu Dhabi Company for Onshore Oil Operations (Adco), which runs the fields, has been 100 per cent owned by Abu Dhabi National Oil Company since January, when the western majors lost their stakes in the operators. Exxon and its Japanese partner Inpex negotiated their per-barrel fee for Upper Zakum from $1 to $2.85. That is expected to serve as a benchmark for Adco, which has long paid one of the lowest fees in the world,” the National reported.

Iran may need to offer more attractive terms than its peers due to its pressing need to recover from economic woes, put its population to work and shore up its bank account. Israel, wanting to develop its gas resources, recently bowed to price increase demands from Noble Energy (ticker: NBL) and Delek because Prime Minister Benjamin Netanyahu said he is “determined to get the gas out.”

Steps toward a Rebalance: 2 Lightning Rods

Is the U.S., because of political posturing, restricting itself from taking full advantage of the domestic shale revolution that it started, the one that has changed the global energy landscape?

Two political lightning rods might be holding the U.S. energy boom back. The Keystone XL pipeline and the U.S.’s 40-year-old crude oil export ban.

Construction of the Keystone XL (by U.S. workers) would further integrate its relationship with Canada on the energy front. These are the same two countries that have permanently changed the global energy picture by moving their vast unconventional hydrocarbon resources out of the ground and getting them into the marketplace. Unconventional technology has changed the equation. In August 2006, OPEC accounted for 43% of U.S. crude oil imports while Canada was responsible for 17%.

Construction of the Keystone XL (by U.S. workers) would further integrate its relationship with Canada on the energy front. These are the same two countries that have permanently changed the global energy picture by moving their vast unconventional hydrocarbon resources out of the ground and getting them into the marketplace. Unconventional technology has changed the equation. In August 2006, OPEC accounted for 43% of U.S. crude oil imports while Canada was responsible for 17%.

Fast forward to May 2015: OPEC is down to 33% of U.S. imported oil, and Canada has more than doubled its share to 38%. The U.S. shale boom, has reduced its overall import volume by 35%, down to 9.8 MMBOPD in May 2015 from 15.2 MMBOPD in August 2006.

A long-awaited green light for TransCanada’s (ticker: TRP) Keystone XL (KXL) pipeline would create an estimated 42,000 jobs during the two-year construction period, drastically helping an industry that has suffered an estimated 150,000 layoffs since November. Corey Goulet, President of Keystone Projects for TransCanada, told OAG360 in March that the KXL would have a ripple effect on the communities that host it in the form of $50 million in various taxes.

“When we built the Gulf Coast portion of the project, you couldn’t find a local business owner who didn’t appreciate the infusion of capital to the local area,” Goulet said. “When we built the Gulf Coast project some of the car and truck dealerships saw a 25% increase in sales, and restaurants and grocery stores also saw increases.”

A study by the U.S. Department of State says alternatives to the Keystone, like crude by rail, carry an environmental impact that would be anywhere from 28% to 42% greater than that of the pipeline.

Relic of the ‘70s

Remember the Gremlin, the Pinto and the Vega? Removing the crude oil export ban, another “relic of the ‘70s,” would open the doors to global trade opportunities for the U.S.’s vast resources. To date, only four companies are allowed to export crude products and they are only allowed to do so once it meets the criteria for condensate. Proponents of the industry believe the ban must be pulled in order for the shale revolution to continue.

Remember the Gremlin, the Pinto and the Vega? Removing the crude oil export ban, another “relic of the ‘70s,” would open the doors to global trade opportunities for the U.S.’s vast resources. To date, only four companies are allowed to export crude products and they are only allowed to do so once it meets the criteria for condensate. Proponents of the industry believe the ban must be pulled in order for the shale revolution to continue.

“The U.S. is the only major oil-producing country in the world that bans the export of crude, putting U.S. producers at a competitive disadvantage” said John Hess, CEO of Hess Corporation, in a commentary for The Wall Street Journal. “At this moment the U.S. government is considering lifting sanctions on Iranian crude oil exports. Why not lift the self-imposed “sanctions” on U.S. crude exports that have been in place for the past four decades?”

The Brookings Institution and IHS have published studies that say ending the ban would also benefit consumers by dropping gasoline prices as much as $18 billion annually. Hess pointed out that oil and gas capital investments represent 7% of U.S. spending as a whole, and the economy is being weighed down considering investments in 2015 are roughly one-third lower than 2014.

Ryan Lance, CEO of ConocoPhillips (ticker: COP), implored Congress to drop the ban earlier this year. “Government should recognize the new reality of the renaissance that has transformed North America from energy scarcity to abundance, and enable the industry to keep it going,” he said. “We have just scratched the surface of its potential, and can help ensure that the renaissance continues as an engine of long-term economic growth by exporting our excess crude oil into the world market.”

One Million Jobs, $750 Billion in New E&P Investment and $1.3 Trillion in Taxes and Royalties to the Feds: What’s Not to Like?

Economic benefits cited by IHS and Brookings Institution include the addition of one million direct or supply-chain jobs. Other benefits realized by the year 2030 include $750 billion in new E&P investment and $1.3 trillion in taxes and royalties gained by the U.S government.

Voices on both sides of the Atlantic are calling for an end to the U.S. crude export ban. In a talk to the U.S. Chamber of Commerce, Doug Suttles, president and CEO of Encana (ticker: ECA), put it this way: “Lifting the crude export ban would help stabilize the global supply; … the export ban was put in place 40 years ago—1975. Gerald Ford was president. For some of us that have been around a while you might remember that we were listening to music on 8-track tape players.”

Some U.S. companies see the future of opening up broad scale energy exports from the U.S. and are taking action now. Cheniere Energy (ticker: LNG), the first mover in the U.S. LNG export marketplace, is adding a $550 million liquids storage and marine terminal down the coast from its Corpus Christi, Texas, LNG export facility that is presently under development. Cheniere’s Sabine Pass LNG facility in Louisiana is on track to deliver its first LNG cargoes to Asian and European customers in early 2016. “The [liquids] terminal will be able to export any type of domestic oil if the decades-old U.S. crude export ban is ever lifted,” Reuters reported. A Cheniere spokesperson timed shipping condensate exports at 2017.

On July 30, the Senate Energy and Natural Resources Committee voted 12-10 to approve Sen. Lisa Murkowski’s (R-Alaska) bill that would lift the ban. Additionally the Murkowski bill would open more areas to offshore drilling and give nearby states a share of the royalties, The Hill reported.

Next comes the House of Representatives’ energy bill, slated for a post-recess vote. If that bill passes both the House and Senate in the fall, the industry will be only one signature away from U.S. producers being handed the keys to begin exporting crude oil globally—the end of a 40 year hiatus.

“In light of the Iran deal, the policy and politics of keeping the US crude export ban in place will be difficult to defend,” the Washington-based Potomac Research Group said, according to Bloomberg. “How can the US government approve lifting a ban on Iranian crude exports, but not a ban on US crude exports?”

V, U, N or W?

Regardless of what shape it takes, this is the oil business. A recovery is in the making.

Important disclosures: The information provided herein is believed to be reliable; however, EnerCom, Inc. makes no representation or warranty as to its completeness or accuracy. EnerCom’s conclusions are based upon information gathered from sources deemed to be reliable. This note is not intended as an offer or solicitation for the purchase or sale of any security or financial instrument of any company mentioned in this note. This note was prepared for general circulation and does not provide investment recommendations specific to individual investors. All readers of the note must make their own investment decisions based upon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Investors should consider a company’s entire financial and operational structure in making any investment decisions. Past performance of any company discussed in this note should not be taken as an indication or guarantee of future results. EnerCom is a multi-disciplined management consulting services firm that regularly intends to seek business, or currently may be undertaking business, with companies covered on Oil & Gas 360®, and thereby seeks to receive compensation from these companies for its services. In addition, EnerCom, or its principals or employees, may have an economic interest in any of these companies. As a result, readers of EnerCom’s Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this note. The company or companies covered in this note did not review the note prior to publication. EnerCom, or its principals or employees, may have an economic interest in any of the companies covered in this report or on Oil & Gas 360®. As a result, readers of EnerCom’s reports or Oil & Gas 360® should be aware that the firm may have a conflict of interest that could affect the objectivity of this report.