EnerCom Dallas presenter Razor Energy Corp. releases 2018 corporate budget and guidance

Alberta-based Razor Energy Corp. (ticker: RZE) announced Monday that the company has approved a corporate budget of $38.4 million for fiscal 2018. The budget will be deployed to continue production growth and to develop power generation and oilfield information technology, according to the company’s press release.

The 2018 budget will be split out as follows:

- Kaybob area drilling – 33%

- Natural gas power, oilfield IT, other – 22%

- Reactiviations, workovers and stimulations – 21%

- Land and other acquisitions – 15%

- End of life expenditures – 8%

Using that 2018 budget allocation, Razor anticipates that 2018 exit production will reach 5.4 MBOEPD, up 15% from year-end 2017.

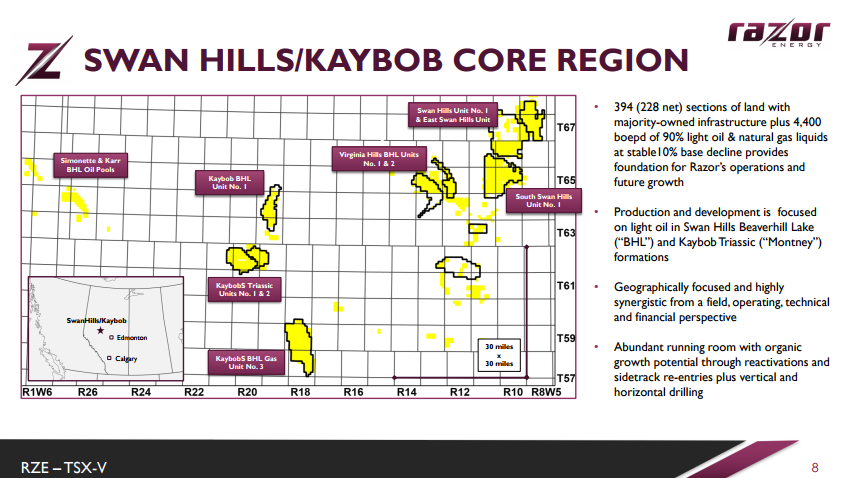

The increased production will be driven in part by a development drilling program including eight deviated wells targeting the oil-prone Montney formation in the company’s recently consolidated Kaybob South Triassic A Pool.

Razor bought higher working interest in two Montney wells

Over the course of December and January, the company paid $9.5 million of cash on hand to increase its working interest in the play from 52.9% and 43.3% in the Kaybob Triassic Unit #1 and Unit #2, respectively, to 93.5% and 100%.

The Kaybob asset is characterized by low-decline, light oil focused production and abundant infrastructure that directly complements Razor’s existing asset portfolio, according to the company. Razor reported that Kaybob directional wells have internal rates of return (IRRs) of 108% and payout in approximately one year at $60 WTI.

Reactiviations, workovers and stimulation include activities in both the Swan Hills and Kaybob areas. Also included are certain injection management activities of existing waterfloods which will complement current production levels while enhancing long-term recoveries of oil in place, the company said.

In light of current oil prices, Razor plans to grow production with a “reasonably aggressive yet flexible approach.” The budget will be continuously reviewed and adjusted in response to changes in light oil prices and project economics, RZE said in its release. The company is guiding to a 1.6x net debt to 2018 funds flow from operations.

Razor making investments into field efficiencies

A major part of the company’s 2018 capital budget will go to addressing operating costs through heightened field efficiencies and capital investment in the design, purchase, and installation of natural gas fired power generation units in Swan Hill, the company said.

In addition, an upgrade to the Swan Hills oilfield information system will allow for better operational awareness, preventative maintenance, personnel safety, and environmental protection through actionable and predictive analytics, the company said.

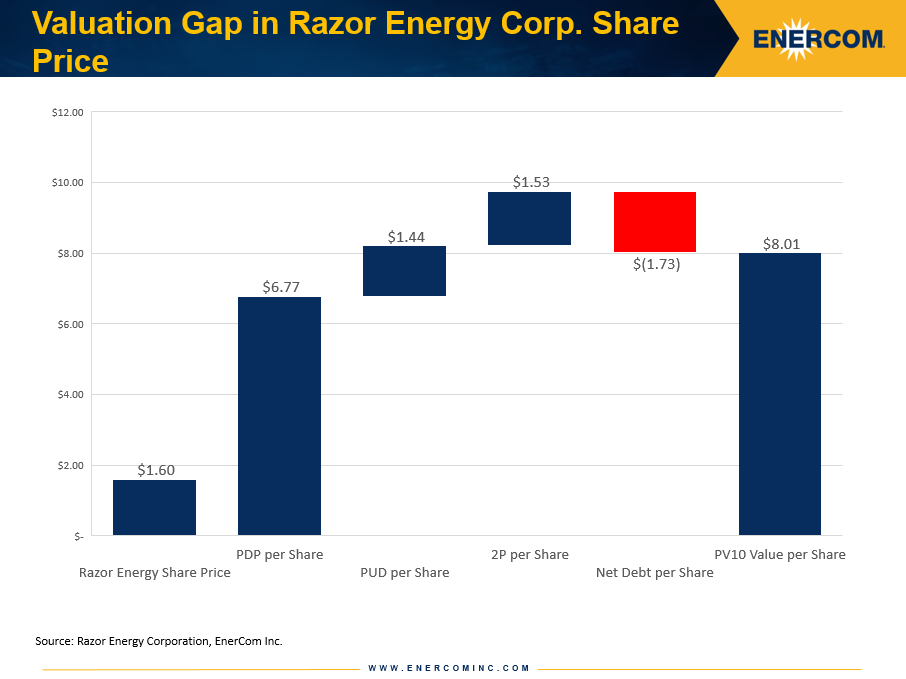

A serious valuation gap

Public companies typically trade at a multiple greater than the PV-10 value of their total proved reserves. Razor shares are trading 4.2x below the Proved Developed Producing (PDP) assets, which equate to $106.7 million or $6.77 per share. Stepping that analysis out further to encompass upside from PUD locations and 2P reserves less the company’s $27.3 million in net debt, the valuation gap grows even wider.

On a PV-10 basis, Razor Energy’s shares have an implied value of $8.01 per share, or 5.0x greater than where they trade today. This valuation target makes no assumptions of changes in Razor’s operations or greater market trends.

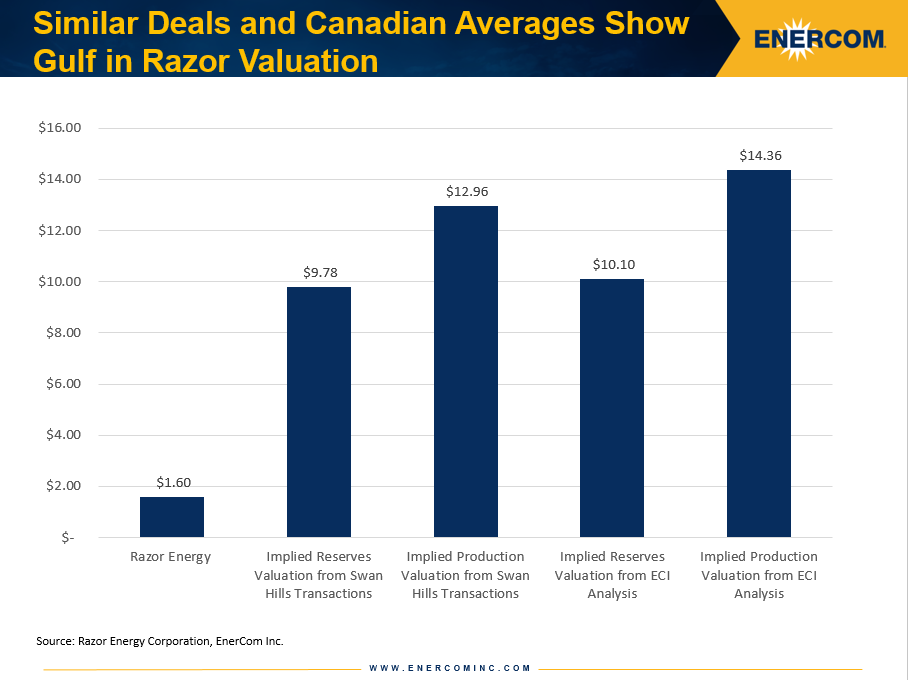

Swan Hills transactions

The majority of the company’s current production comes from Swan Hills region of Alberta, Canada, which has seen a number of transactions over the last several years. The most recent of those deals, which was announced in September 2017, was Pengrowth Energy’s purchase of ExxonMobil Canada Energy’s average 89% working interest in properties in the Carson Creek area. That deal went for $29,644 per flowing BOE or $4.84 per BOE of 2P reserves.

Of the five deals that took place in the region since July 2015, the average deal metrics is $49,857 per flowing BOE and $9.78 per BOE of 2P reserves. Applying those metrics to Razor’s assets, the company’s implied valuation is $12.96 per share on a flowing BOE basis and $9.78 per share per BOE of 2P reserves.

As of December 11, 2017, Razor was trading at a $6,168 per flowing BOE and $1.70 per BOE of 2P reserves, 88% and 83% below average metrics in the area, respectively.

Looking at Razor Energy’s Canadian peers in the EnerCom database, the valuation disconnect is even wider. By applying a multiple of the average dollar-per-BOE realized by Canadian companies to Razor’s production, the company’s implied share price is $14.36 while applying a similar analysis based on average dollar-per-BOE of 2P reserves implies a value of $10.10 per share. The company’s current stock price of $1.80 per share is 5.6x and 7.3x below the implied valuation from applying the average multiple achieved by Canadian companies on their 2P reserves and flowing production, respectively.

As Razor continues to develop its assets and improve operational efficiencies, these gaps will likely begin to close, bringing the company’s market valuation more in-line with its peers.

Razor Energy is presenting at the EnerCom Dallas oil and gas investment conference, February 21-22 at the Tower Club Downtown Dallas. Buyside money managers and analysts are encouraged to meet the RZE senior management team in person by registering to attend the conference and scheduling a one-on-one meeting. Details are available at the EnerCom Dallas conference website.