Iran tapped spare capacity and increased production more than 800 MBOPD

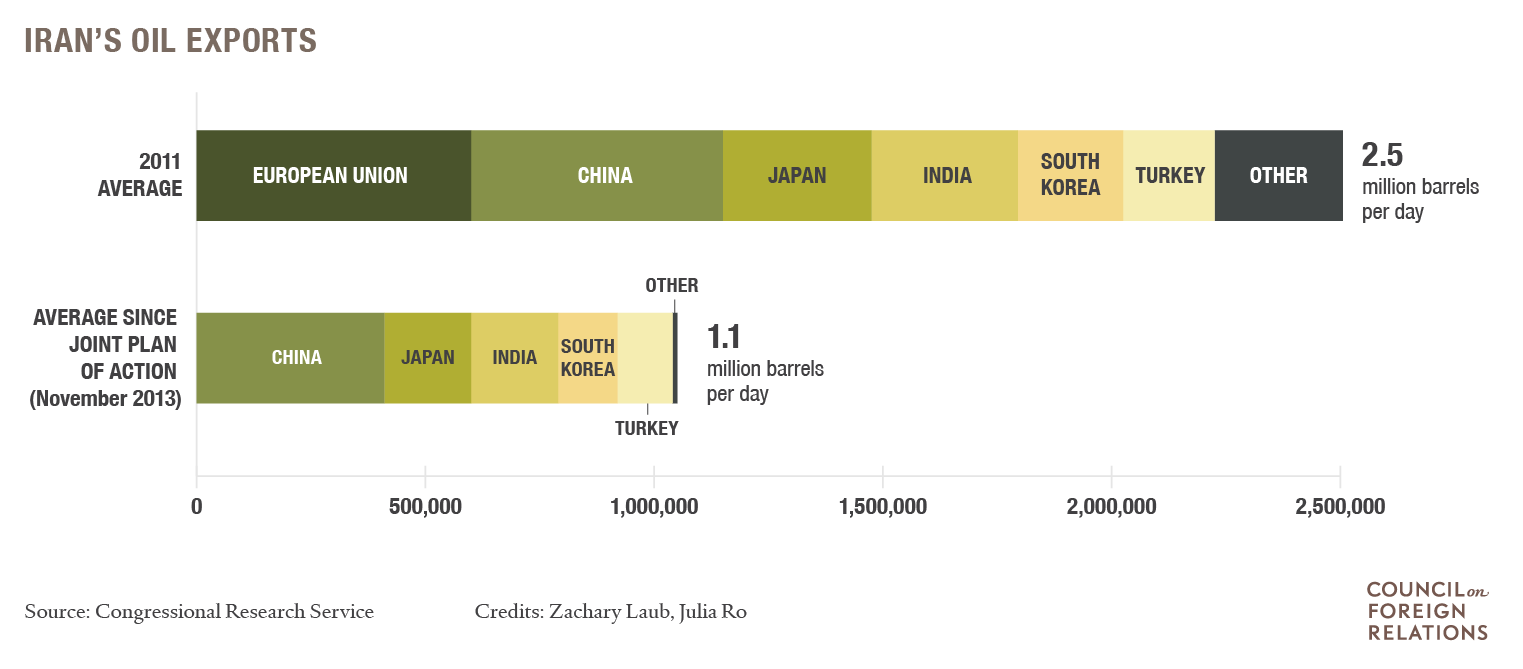

July 14 marks the one-year anniversary of the implementation of the Joint Comprehensive Plan of Action (JCPOA) negotiated by Iran and the P5+1, which included the U.N. Security Council and Germany. The JCPOA marked a historic deal between Iran and the political West, with the former agreeing to give up nuclear ambitions in the near-term in exchange for sanctions relief. And while the deal had both its proponents and detractors, no one was entirely sure what sanctions relief on Iran would mean for global oil markets or regional stability.

The addition of more oil from Iran sent a shock through oil markets with U.S. crude benchmark WTI shedding 7.5% of its value as concerns of the global glut worsening took hold. Experts varied widely on just how much oil Iran could bring back to markets out of the gate, however. SVB Energy International expected the Islamic Republic could add as much as 800 MBOPD to its production in a year, while others, like Wood Mackenzie, projected it would be year-end 2017 before Iran added even 600 MBOPD to its production.

A year down the line the numbers are in, and SVB was nearly on the money. From June 2015 to June 2016, Iran’s production increased 814 MBOPD according to secondary sources cited in OPEC’s monthly release. June 2016 production was 3.6 MMBOPD, compared to 2015 production of 2.8 MMBOPD. In the course of one year, Iran’s share of OPEC’s production rose to 11% from 9%.

While this jump in production exceeded the expectations of many, Iran still has 1.4 MMBOPD of production to add before it reaches its goal of 5 MMBOPD, and this may prove more difficult than the increases seen over the last year.

Much of Iran’s added production has come from mothballed fields that the country is bringing back online. In effect, Iran is just tapping its spare capacity, not adding new production.

The increases in Iran’s production has been “a most impressive performance that most would not have predicted a year ago,” Hossein Askari, the Iran Professor of International Business and International Affairs at The George Washington University, and who has served on the Executive Board of the International Monetary Fund, Special Advisor to the Minister of Finance of Saudi Arabia and as a consultant to the OECD, the World Bank, the IFC, the U.N., the Government of Saudi Arabia, and a number of multinational corporations, told Oil & Gas 360®.

But “most of this, if not all, has come from reactivating idle wells and increasing the flow from chocked wells.”

Investment to reach the 5 MMBOPD goal is still lagging

In order for Iran to reach its 5 MMBOPD goal, it will need to attract more investment from foreign countries, a process that has proved to be slow for the Islamic Republic.

“We’re not optimistic about Iran hitting that 5 MMBOPD goal soon,” Matthew Bey, an energy analyst with Stratfor, told Oil & Gas 360®. “We’re not seeing enough investment to get more than a couple hundred-thousand barrels per day of added production.”

For Iran to attract the significant foreign investment it requires, estimated at $280 billion last year, “foreign investors will first and foremost require assurances that their investment in Iran would not run them afoul of U.S. regulations and thus expose them to U.S. financial fines,” said Askari. “Less talked about but no less real, there is the danger that investors in Iran’s oil sector could be exposed to sanctions from Saudi Arabia and other members of the GCC. Reportedly, Saudi Arabia has already banned tankers that carry Iranian crude from entering its waters.

“Also foreign investors will be looking for attractive production sharing contracts in a world awash with crude. Let’s also not forget that in the past Iran has been its own worst enemy—its inflammatory rhetoric that affords little comfort to foreign investors,” Askari added.

New petroleum contracts are becoming a political powder keg in Iran

Beyond the fear of angering regional and global powers like Saudi Arabia and the U.S., uncertainty remains around what the Iranian Petroleum Contracts (IPCs) will offer investors and foreign partners once they are finalized. Because Iran’s constitution does not allow for the foreign ownership of Iranian oil, the country is not able to provide typical production-sharing style contracts to International Oil Companies (IOCs).

Iran’s reformers have been working to structure the IPCs in a way that still compensates upstream developers on a sliding-scale basis depending on the difficulty of the project and the IOC’s level of involvement, but the new contracts have become a domestic policy sticking point.

“The IPCs are being heavily debated in Iran,” said Bey. “The hardliners are lashing out while the reformers keep working, but we’re pessimistic that the IPCs will be ready by the summer.”

That timeline creates a new set of problems, he added. Iran’s presidential elections are quickly approaching, and if the IPCs are not finalized before then, it’s unclear what may become of them.

Hassan Rouhani, Iran’s sitting president, campaigned on a platform of economic growth brought about by returning Iran to the world stage. Rouhani delivered on ending international sanctions, but the economic benefits that were supposed to follow have been slow to materialize, a fact his opposition is likely to use against him as he campaigns for reelection.

“The economy will be a key battleground for the Iranian elections,” said Bey. “Rouhani promised the nuclear deal, which took some time, and he promised to lower inflation, which he has also done. But creating new jobs and increasing salaries takes time.” If Rouhani loses reelection, the IPCs could potentially be watered down by a new president, blunting the interest from foreign investors.

“It’s uncommon for an incumbent to lose in Iran, but the hardliners are assaulting him on economics and other policies,” said Bey.

The big picture: shifting ties and unrest in the Middle East

Beyond the domestic political climate and the oil market, the JCPOA has changed important relationships in the Middle East. Saudi Arabia, Iran’s regional rival, saw the deal as a real and substantial threat, and the involvement of the U.S. made the nuclear deal even more unnerving.

“The deal has ratcheted up tensions between Saudi Arabia and Iran. Saudi Arabia sees Iran’s acceptance of the deal as merely a tactic in its broader strategy to achieve regional hegemony, having ‘neutralized’ the U.S. threat for the time being,” Former U.S. Ambassador to Omen and CEO of Equilibrium International Consulting Gary Grappo told Oil & Gas 360®. “Importantly, however, neither side can afford – and will therefore avoid – a military confrontation.

“The Saudis went into the negotiations with great skepticism, fearing a lessoning of vigilance against their arch-enemy Iran and an American distancing from the Kingdom. The agreement also came with a lower U.S. profile in the Middle East in general, also alarming the Saudis. The U.S. has tried to patch up differences and the Saudis have largely gone along with the deal.

“Simultaneously, however, they are looking to others, e.g., the EU, China and Russia for economic and security ties. Ultimately, however, there is no one who can provide the kingdom with the kind of security assurance the U.S. can. This relationship will require much care and attention in the next administration.”

Hillary Clinton is a known commodity throughout most of the Middle East, including Saudi Arabia,” said Grappo. “She comes from a relatively pragmatic position on foreign policy and might be an easier person with whom to work than her predecessor was, assuming she’s elected.

“Trump is largely unknown. Some in the Middle East are showing greater interest in him, fearing if Clinton is elected, she may follow Obama’s policy. That would be an incorrect reading of her in my estimation. Moreover, Trump has indicated an interest in renegotiating for a ‘better deal’ with Iran on its nuclear program. That is highly unlikely, if not impossible, given neither Iran nor our negotiating partners, the P5+1, have an interest in reopening the agreement.”

Ambassador Grappo will be speaking at EnerCom’s The Oil & Gas Conference® 21 on August 17, at 12:50 p.m. EST. To learn more about the presenters coming to EnerCom’s conference this year, click here.

What will year two of the JCPOA look like?

Many were surprised at how quickly Iran brought production back online following the lifting of sanctions, but with an uncertain investment climate, year two of the JCPOA may look more stagnant.

“It will be a period of wait and see,” said Askari. “There are many uncertainties. Will the regime change its tune? Will the U.S. clarify sanction worries for investors? Will Iran-Saudi relations improve or worsen? What will happen if the Supreme Leader has to be replaced?”

Stratfor’s Bey believes that while Iran may sign some of the first IOCs by the end of 2016, there will likely be a lull in activity afterward. “They’re on the right track, but we need to see the final terms before investors really jump in,” he said, adding that Stratfor does not expect Iran to reach its 5 MMBOPD production target before 2022.

The addition of 800 MBOPD in the year that followed the lifting of international sanctions was surprising to most, but the future looks to be a story of slower growth. Most of the oil that came back to markets from July 2015 to July 2016 was from preexisting fields, but now Iran will need the help of IOCs to go further. With the state of both domestic and international politics in flux, it is unclear what the future investment climate in Iran could look like, but the Islamic Republic will need the help of international partners if it hopes to reach its 5 MMBOPD target.